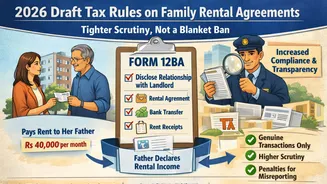

For years, salaried individuals have made rental agreements with parents or close relatives as part of legitimate tax planning. When properly documented,

such arrangements have enabled employees to claim House Rent Allowance (HRA) exemptions without breaching tax laws. But with the proposed Income Tax Draft Rules, 2026, many taxpayers are asking whether these family-based rental setups will continue to hold ground. The short answer: yes, but with a more transparent process. What Are The Draft Rules Change The Income Tax Draft Rules, 2026, introduce an additional compliance layer. Taxpayers claiming HRA will now have to disclose the ‘relationship with the landlord’ in Form No. 124. This step is designed to tighten reporting standards and reduce misuse, not to outlaw genuine rental agreements between family members. Under Draft Rule 205, there is no blanket ban on paying rent to parents, in-laws, or even a spouse. However, the arrangement must be authentic. That means a formal rental contract, rent transfers through banking channels, proper rent receipts, and the landlord declaring rental income in their return. The change essentially increases reporting obligations rather than restricting who can legally act as a landlord. How The Rule Works Consider Poorva Gupta, a 30-year-old sales professional based in Mumbai. She resides in a flat owned by her Father and pays Rs 40,000 per month as rent. She claims HRA exemption under Section 10(13A) read with Rule 2A. The agreement is backed by documentation, and payments are made via bank transfer. Her father includes the rental income in her tax filings. With Draft Rule 205 in place as part of the Central Board of Direct Taxes’ rollout, Poorva must disclose her relationship with the landlord in Form 12BA. The arrangement itself remains permissible. The added disclosure enables closer scrutiny of related-party transactions. Experts Clarify The Legal Position Tax professionals highlighted that the rule is about accountability, not prohibition. "Draft Rule 205 does not make paying rent to relatives illegal. Renting from parents, spouses, or other family members remains a perfectly legitimate tax-planning arrangement under the law, provided the transaction is genuine. The rule is simply designed to bring these transactions out of the shadows and ensure they are reported consistently by both the tenant and the landlord," says Rohit Jain, Managing Partner, Singhania & Co., according to a HT report. Legal experts echo a similar view. “Instead, it constitutes a calibrated transparency and disclosure measure intended to fortify the integrity of tax administration by mandating explicit declaration of the landlord-tenant relationship in Form 12BA. This enables employers and, more significantly, the Income-tax Department to identify and examine related-party rent arrangements with greater precision and vigilance,” says Tushar Kumar, Advocate, Supreme Court of India, as per the. He further explains, “It aligns with the settled legal principle that while tenancy between relatives is perfectly lawful and permissible, the same must withstand the test of genuineness, commercial substance, and actual payment, and must not be a mere colourable device for tax avoidance.” Higher Scrutiny, Higher Penalties For Misreporting The compliance bar is clearly being raised. If rent payments are artificial, circular, or not reflected in the landlord’s return, penalties may follow. Under Section 270A of the Income-tax Act, 1961, under-reporting can attract a penalty of 50 per cent of the tax payable, while misreporting may invite penalties of up to 200 per cent. “However, it must be stated with equal clarity and authority that in bona fide arrangements, where rent is genuinely paid, properly documented, aligned with market realities, and duly disclosed by the recipient in their tax returns, the exemption remains fully tenable in law and defensible upon scrutiny,” says Kumar. In essence, the Draft Tax Rules 2026 do not dismantle family rental arrangements. They reinforce documentation, transparency, and consistency, protecting genuine claims while deterring abuse.