What's Happening?

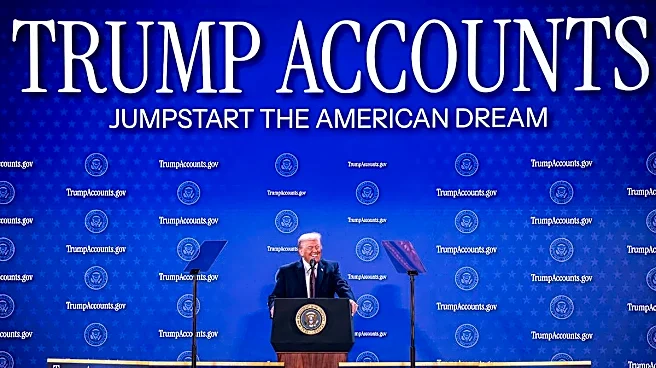

The Trump Administration has introduced a new financial initiative called Trump Accounts, set to launch on July 4. These accounts, also known as 530A accounts, are designed to help children under 18 build savings for the future. Under this program, children born

between January 1, 2025, and December 31, 2028, who open an account will receive a $1,000 contribution from the Treasury Department, which will be invested in the stock market. The accounts were created under the One Big Beautiful Bill Act and aim to function similarly to individual retirement accounts (IRAs) for adults. Contributions to these accounts must be invested in mutual funds or ETFs that track large indexes like the S&P 500. The accounts are administered by Bank of New York Mellon in partnership with Robinhood, and can be managed through the Trump Accounts app or website.

Why It's Important?

The introduction of Trump Accounts represents a significant effort by the government to encourage early financial literacy and savings among young Americans. By providing a $1,000 seed contribution, the program aims to give children a head start in accumulating retirement assets. This initiative could potentially influence the financial habits of a new generation, promoting long-term savings and investment from an early age. The involvement of major corporations like Dell Technologies, Bank of America, and JPMorgan Chase, which have pledged to match the government's contribution, underscores the program's potential impact on the financial sector. However, the accounts come with certain restrictions, such as contribution limits and penalties for early withdrawal, which may affect their attractiveness compared to other savings options.

What's Next?

As the Trump Accounts program rolls out, parents and guardians are encouraged to sign up for these accounts by completing IRS Form 4547. The program's success will likely depend on public reception and participation rates. Financial experts suggest that while the $1,000 government contribution is a significant benefit, families should carefully consider the tax implications and restrictions associated with these accounts. The program may also prompt discussions about the best ways to encourage savings and investment among young people, potentially influencing future policy decisions in the realm of financial education and youth savings initiatives.