What's Happening?

The landscape of fraud detection in business transactions is undergoing a significant transformation with the integration of artificial intelligence (AI) tools. According to insights from Mary Kay Bowman, executive vice president and head of payments

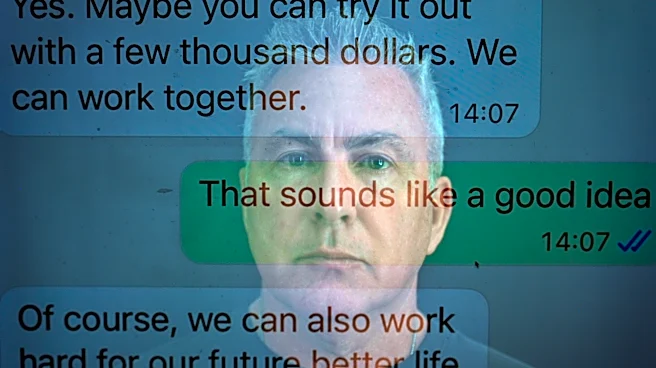

and financial services at BILL, traditional fraud patterns remain, but the tools used to detect them have evolved. AI now allows for real-time visibility into transactions, enabling earlier detection of fraudulent activities. A report from BILL highlights that 56% of businesses have experienced an increase in fraud attempts over the past year, with 42% noting that these attacks are becoming more sophisticated. This shift in technology means that fraudulent activities, which previously went unnoticed until the end of a financial period, can now be identified as they occur, provided the technology is effectively implemented.

Why It's Important?

The integration of AI in fraud detection is crucial for businesses, particularly small and midsized enterprises, which may lack the resources to monitor financial transactions closely. The ability to detect fraud in real-time can prevent significant financial losses and protect business integrity. As businesses increasingly rely on digital payment platforms, the need for robust fraud detection systems becomes more pressing. The report indicates that 92% of business leaders are concerned about fraud, underscoring the importance of reliable technology to safeguard financial operations. Companies that fail to adopt advanced fraud detection tools risk financial losses and damage to their reputation, while those that do can enhance trust with clients and stakeholders.

What's Next?

Businesses are likely to continue integrating AI-driven fraud detection systems to enhance their financial security. As fraud attempts become more sophisticated, companies will need to ensure that their technology partners provide systems that learn continuously and adapt to new threats. This ongoing evolution in fraud detection technology will require businesses to regularly evaluate their systems' effectiveness and ensure compliance with data security standards. Additionally, financial advisors and accountants will need to update their skills to understand and leverage these new tools effectively, ensuring they can provide informed advice to their clients.