A Mindset Shift to Investing

For many young Indians, the traditional approach of simply saving money in a bank account is no longer enough. This generation, born between 1997 and 2012, grew up in a digital-first world and witnessed economic uncertainty during events like the COVID-19

pandemic. As a result, they view money not just as a means of security, but as a tool for freedom and achieving financial independence early. Instead of letting cash sit idle in low-interest savings accounts where it loses value to inflation, they are actively seeking ways to make their money work for them. This has led to a remarkable surge in investment awareness, with a significant portion of new investors in India now coming from the under-30 demographic.

The Magic of UPI AutoPay

At the heart of this transformation is the Unified Payments Interface (UPI), particularly its AutoPay feature. Launched by the National Payments Corporation of India (NPCI), UPI AutoPay allows users to set up recurring payments for everything from subscriptions to loan EMIs and, most importantly, investments. It functions like a modern-day standing instruction but is far more seamless. Users can authorise a mandate directly from their UPI-enabled app in seconds, eliminating paperwork and the long processing times associated with traditional bank mandates. This convenience is a game-changer for building consistent financial habits.

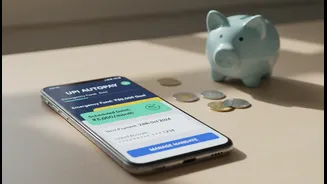

Powering SIPs with Automation

The most popular application of this technology for Gen Z investors is funding Systematic Investment Plans (SIPs). A SIP allows you to invest a fixed amount of money into mutual funds at regular intervals, such as monthly. By linking a SIP to UPI AutoPay, the investment process becomes completely automated. On the scheduled date, the pre-approved amount is debited from the user's bank account and invested in their chosen mutual fund. This 'set it and forget it' approach instills discipline and leverages the power of rupee cost averaging, which helps mitigate the risks of market volatility by averaging out the purchase price of fund units over time.

The Rise of Fintech Investment Apps

This automated investment revolution is facilitated by a host of user-friendly fintech apps. Platforms like Groww, Zerodha Coin, Paytm Money, and others have democratised investing by offering zero-commission direct mutual fund plans and intuitive mobile interfaces. These apps allow users to complete their KYC digitally, choose from thousands of funds, and set up a UPI AutoPay mandate in just a few taps. The entire financial journey, from learning about funds to tracking portfolio growth, happens on a smartphone screen, making it incredibly accessible for a generation that lives online.

The Behavioral Edge of Automation

One of the biggest advantages of automating investments is that it removes emotion from the equation. Markets are often volatile, and fear or greed can lead investors to make poor decisions, like selling during a downturn or buying impulsively at a peak. Automated SIPs through UPI AutoPay enforce discipline, ensuring that you continue investing consistently regardless of market sentiment. This long-term, steady approach is one of the most reliable strategies for wealth creation. It turns investing from a series of stressful decisions into a simple, background habit, much like paying a monthly bill.

Smart Automation: Risks and Best Practices

While technology makes investing effortless, it doesn’t eliminate the need for diligence. It's crucial to research the mutual funds you invest in and understand their associated risks. Automation is a tool for execution, not a substitute for financial literacy. Users should also be mindful of the UPI AutoPay limits; for mutual funds and insurance, the limit is typically ₹1 lakh per transaction. It is also wise to periodically review your automated investments to ensure they still align with your financial goals. While robo-advisors and automated platforms are excellent for getting started, they may not be suitable for complex financial situations.