The Modern Savings Dilemma

You get your salary, you have great plans for it. You promise yourself this is the month you’ll finally start that emergency fund. But then, a weekend trip comes up, a new gadget drops, or a series of small, seemingly innocent online purchases add up.

Before you know it, it's the end of the month, and your savings goal is pushed to the next one. This is a common struggle for millennials and Gen Z. In a world of instant gratification and frictionless spending, the discipline required for manual savings can feel like a chore. The constant decision-making of when and how much to save creates a mental burden that often leads to inaction.

Your UPI App: An Unlikely Savings Coach

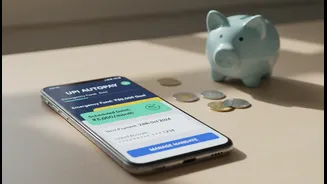

The Unified Payments Interface (UPI) has already transformed how India pays for things. But its power extends beyond simple peer-to-peer payments or scanning QR codes. A lesser-known but incredibly powerful feature is UPI AutoPay, a recurring payment system built by the National Payments Corporation of India (NPCI). Think of it as a modern, digital version of a standing instruction. You authorise a mandate once, and it automatically debits a fixed amount from your account at a set frequency—daily, weekly, or monthly. This is the key. By automating the process, you remove the need for willpower. It’s a “set it and forget it” strategy that outsmarts your own worst financial impulses.

How to Automate Your First Financial Safety Net

Building an emergency fund—typically three to six months' worth of living expenses—is the first step towards financial security. UPI AutoPay makes achieving this target significantly easier. The process involves a few simple, conceptual steps. First, you open an account with a fintech investment app that offers this feature. When you choose to invest, you select a specific instrument, like a Liquid Mutual Fund, which is a popular choice for emergency funds due to its low risk and easy accessibility. During setup, you select “UPI AutoPay” as your payment method. You’ll be prompted to approve a mandate in your UPI app (like Google Pay, PhonePe, or Paytm), where you define the amount and frequency, and confirm it with your PIN. That's it. The mandate is a one-time setup. Afterwards, the app will automatically pull the specified amount on the scheduled dates, building your savings without you having to lift a finger.

Where Does the Money Go?

An emergency fund needs to be parked in a place that is both safe and easily accessible. While a simple savings account is an option, it offers very low returns. Many young investors use UPI AutoPay to direct funds into Liquid Mutual Funds. These funds invest in very short-term debt instruments and aim to provide better returns than a savings account while maintaining high liquidity. Some platforms offer instant redemption facilities up to a certain limit, meaning you can get your money back in minutes if needed. Another popular option is a Sweep-in Fixed Deposit, where your bank automatically moves funds above a certain threshold into FDs, earning you higher interest. The key is that the investment product must be supported by the fintech platform you use to set up the UPI mandate.

Beyond the Emergency Fund

The beauty of this automated system is its versatility. Once you've successfully built your emergency fund, you don't have to stop. You can use the exact same UPI AutoPay mechanism for all your other financial goals. Want to save for a vacation, a new laptop, or a down payment on a bike? Create a new mandate. Ready to start your long-term wealth creation journey? Use UPI AutoPay to fund a Systematic Investment Plan (SIP) in an equity mutual fund. The principle remains the same: automate the habit of investing, pay yourself first, and let technology handle the discipline. Many platforms report that a huge percentage of new SIPs are now registered via UPI, thanks to its convenience.