The Rise of Frictionless Finance

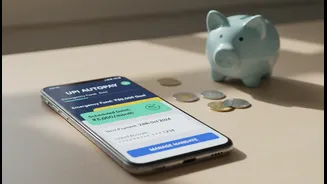

At the heart of this trend is UPI AutoPay, a feature of the Unified Payments Interface (UPI) that allows users to set up recurring payments with a few taps. Launched in 2020, its growth has been explosive. By early 2025, UPI AutoPay was already handling

over 53% of all recurring payment transactions in India, overtaking traditional card-based mandates. While designed for everything from OTT subscriptions to utility bills, its most transformative use has been in automating savings. For Gen Z, a generation with almost universal UPI adoption, it’s a natural fit. It isn’t a savings product itself, but rather the seamless, invisible engine that makes consistent saving and investing possible without the hassle of paperwork or branch visits.

Automating Good Habits

The secret to UPI AutoPay’s success as a savings tool lies in behavioural psychology. The principle is simple: make good habits easy and bad habits hard. For a generation accustomed to instant gratification and battling constant digital distractions, the discipline to manually set aside money each month can be a significant hurdle. AutoPay removes this friction entirely. By setting up an e-mandate—for a mutual fund Systematic Investment Plan (SIP), for instance—the saving happens automatically. This “set it and forget it” approach helps overcome procrastination and ensures that savings goals are met consistently. It transforms saving from a monthly chore requiring active willpower into a passive, background process, which is a game-changer for building long-term wealth.

Designed for the Digital Native

Previous generations had to rely on standing instructions that often involved filling out physical forms at a bank. Gen Z, born with smartphones in their hands, expects financial services to be as intuitive and seamless as their favorite apps. A survey found that 83% of this generation prefers digital-first financial services. UPI AutoPay meets this demand perfectly. An entire recurring mandate can be created, paused, or cancelled directly within a UPI app using a PIN, offering total control without ever speaking to a bank representative or signing a document. This is what “accessible” means to them: not just low cost, but low effort and high control, all managed from the palm of their hand. For this generation, convenience is the ultimate feature.

Lowering the Barrier to Investing

Perhaps the most significant impact of UPI AutoPay is how it has democratized disciplined investing. It has become the primary mechanism for funding SIPs in mutual funds. The process is incredibly simple: choose a fund on a fintech platform, and link your UPI ID to set up a monthly investment. Recognizing this trend, the transaction limit for mutual fund SIPs via AutoPay has been raised to ₹1 lakh, making it a powerful tool for serious and small-scale investors alike. This accessibility empowers young earners to start their investment journey early, even with small amounts, fostering a habit of wealth creation that was previously considered complex or reserved for those with more financial knowledge and resources.

The Old Guard vs. The New

When compared to older savings methods, the appeal of UPI AutoPay becomes even clearer. Traditional options like Recurring Deposits (RDs) often required a visit to the bank to set up. Even early digital methods for SIPs could be clunky. UPI AutoPay streamlines this entire workflow into a few seconds on an app. It offers a level of ease and flexibility that older systems can't match. While tools like Systematic Investment Plans are not new, the method of funding them has been revolutionized. It’s the difference between ordering a taxi by calling a landline versus tapping a button on an app—both achieve the same goal, but the experience is worlds apart, and for Gen Z, the experience is everything.