The Rise of Micro-Savings

Forget the old piggy bank. The new way to save is digital, automated, and happens in such small increments you barely notice it. This is the world of micro-savings, a trend championed by India’s most digitally-native generation. Instead of putting aside

a large, intimidating sum at the end of the month, micro-saving involves automatically saving very small amounts—think ₹50 or ₹100—on a daily or weekly basis. The idea is rooted in behavioural psychology: small, frequent actions build habits more effectively than large, infrequent ones. For a generation that grew up with UPI and values financial freedom, this method removes the friction and mental effort traditionally associated with saving.

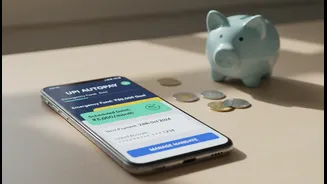

UPI AutoPay: The Engine Behind the Habit

The technology making this possible is UPI AutoPay. Launched by the National Payments Corporation of India (NPCI), this feature allows users to set up recurring payments for everything from subscriptions and bills to investments. Here’s how it works for savings: a user authorises a fintech app to debit a fixed, small amount from their bank account at a set frequency (daily, weekly, etc.). This authorisation, called an e-mandate, is approved once with a UPI PIN. After that, the deductions happen automatically in the background, making saving a 'set it and forget it' activity. This is different from a traditional SIP (Systematic Investment Plan) which is usually monthly and for a larger amount; this is about high-frequency, low-value saving.

Why This Approach Appeals to Gen Z

Gen Z’s entire financial life happens on their smartphone. They prefer digital-first solutions that are fast, transparent, and give them control. Automating micro-savings fits perfectly into this mindset. It feels less like a sacrifice and more like a smart, passive system working for them. Many are already using UPI for dozens of small transactions a month, so an additional small, automated debit feels natural. This generation is also highly risk-aware, not risk-averse; they value starting early, even with small amounts, to leverage the power of compounding. Seeing their savings pot grow, even by a little each day, provides a sense of accomplishment and financial control that resonates deeply.

Popular Apps and Methods

A new ecosystem of fintech apps has emerged to facilitate this trend. Some apps, like Jar and Gullak, use UPI AutoPay to pull small amounts daily and automatically invest them in digital gold. Others, like Bachatt, allow users to set up daily savings from as little as ₹51 into liquid mutual funds. Another popular method is the 'round-up' feature, where an app rounds up your daily digital transactions to the nearest ten and invests the spare change. Major payment platforms and neobanks like Jupiter and Fi Money also integrate savings tools, expense tracking, and automated rules to encourage better financial habits. These tools are designed to make saving intuitive rather than intimidating.

How to Set Up Your Own Micro-Savings

Getting started is simpler than you might think. First, choose a fintech app that offers micro-saving features, whether it's daily debits or round-ups. After downloading the app and completing the basic KYC process with your PAN and Aadhaar, you can link your UPI account. The app will then prompt you to create a savings rule. For instance, you could set a 'Daily Savings' of ₹100. The app will then redirect you to your primary UPI app (like GPay, PhonePe, or Paytm) to approve the e-mandate. You'll review the details—amount, frequency, and duration—and authorise it with your UPI PIN. This is a one-time setup. Once approved, the app will automatically handle the rest, sending you a notification 24 hours before each debit as per RBI guidelines.

What to Keep in Mind

While automated micro-saving is a powerful tool, it's important to stay aware. Regularly check your mandates in your UPI app's 'Mandate' or 'AutoPay' section to see what's active. You have full control to pause, modify, or cancel any mandate instantly. Also, be aware of the investment vehicle your money is going into—whether it's digital gold, liquid funds, or another asset—and understand its associated risks. Micro-saving is an excellent way to build an initial savings habit and emergency fund, but it should complement, not replace, larger, goal-oriented investments for long-term wealth creation.