The Modern Money Challenge

Generation Z in India is navigating a complex financial world. As digital natives, you're comfortable with instant everything, from payments to social validation. This digital fluency is a superpower, but it also creates pressure. The ease of UPI can

make it just as easy to spend as it is to transact, turning your bank balance into a moving target. While studies show that Gen Z are surprisingly disciplined savers, often putting away 20-30% of their income, the desire for financial independence is often at odds with the temptation of instant gratification and the anxiety of starting from scratch.

First, Your Financial Safety Net

Before you can think about long-term wealth, you need a short-term buffer. This is your emergency fund. Think of it as a financial seatbelt against life's unexpected bumps—a sudden job loss, an urgent medical bill, or a necessary home repair. Financial advisors typically recommend saving three to six months' worth of essential living expenses. Without this fund, you might be forced to take on high-interest debt or compromise long-term goals just to handle a crisis. An emergency fund provides peace of mind and the freedom to make decisions without being ruled by fear.

The Psychology of ‘Pay Yourself First’

The hardest part of saving is often just starting. Manually transferring money requires discipline and memory, two things that are easily depleted. This is where automation becomes a game-changer. The principle is called "pay yourself first," and it means treating your savings like a non-negotiable bill. By automating the process, you remove willpower from the equation. The money is moved to your savings before you even have a chance to miss it or spend it, making the habit painless and consistent. This simple shift in process makes a huge psychological difference, turning saving from a monthly chore into a background process that works for you.

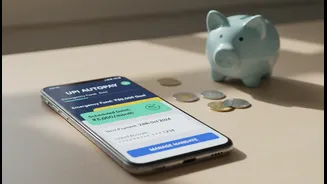

How UPI Auto-Debit Works

UPI AutoPay (or Autopay) is a feature from the National Payments Corporation of India (NPCI) that lets you automate recurring payments. You set up a one-time instruction, called a 'mandate,' through your UPI app. You decide the amount, frequency (daily, weekly, monthly), and duration. Once you approve it with your UPI PIN, the system automatically debits your account on the scheduled date without any further action from you for amounts up to ₹15,000. For amounts between ₹15,000 and ₹1,00,000 for specific categories like mutual fund SIPs, it also runs automatically after the initial setup. You receive a notification before each debit, and you can pause or cancel the mandate anytime through your app, giving you full control.

A Simple Habit for Financial Resilience

For Gen Z, this technology perfectly aligns with a digital-first mindset. You no longer need to rely on old-school standing instructions or remember to manually move money. You can use UPI Autopay to set up a small, recurring transfer to a separate savings account or even a liquid mutual fund, which many fintech apps now offer. By starting with a small, manageable amount—even just a few hundred rupees a week—you begin building the habit. This consistency is more powerful than the amount. As your income grows, you can easily adjust the mandate. The system turns the abstract goal of building a six-month safety net into a series of small, achievable, and automated steps.