The Rise of Set-and-Forget Savings

The Unified Payments Interface (UPI) has fundamentally changed how India transacts, with near-total adoption among Gen Z. Initially celebrated for simplifying peer-to-peer payments and QR code purchases, its capabilities have evolved. A key feature driving

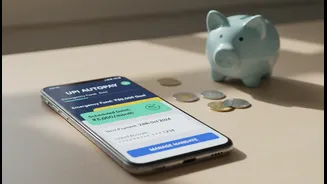

a new financial trend is UPI AutoPay. This function allows users to set up recurring e-mandates for everything from bills and subscriptions to investments. Instead of manually transferring money, a user can authorise an app to automatically debit a specific amount at regular intervals—daily, weekly, or monthly. This automation is proving to be a powerful tool, not just for expenses, but for systematically building savings without requiring constant effort or discipline.

Paying Yourself First, Automatically

Financial advisors have long preached the principle of “paying yourself first”—treating savings as a non-negotiable expense. Historically, this required discipline. However, UPI AutoPay removes the psychological barrier. By setting up an automated transfer to a savings account or a Systematic Investment Plan (SIP), young users are turning this classic advice into an effortless habit. This system works by removing willpower from the equation. The decision to save is made once, and technology handles the rest. While the convenience of UPI can sometimes lead to impulse spending, studies show that its tracking features and the ability to automate transfers also promote financial discipline when used mindfully. This automation creates a positive friction: money earmarked for savings is moved out of sight and out of mind, making it less likely to be spent.

What Transaction Data Reveals

While the headline's term "digital wallet audits" isn't standard industry parlance, analysis of transaction data from fintech platforms and payment gateways reveals a clear pattern. There is a surge in the use of UPI AutoPay for micro-investments and savings. Wealth-tech apps that allow users to invest small, recurring amounts in mutual funds, digital gold, or other assets have seen significant adoption, powered by the ease of setting up an AutoPay mandate. NPCI data shows that recurring payment volumes via UPI AutoPay have doubled in the last year alone, signaling a massive behavioral shift. These aren't just for OTT subscriptions; they are increasingly used for SIPs and other goal-based savings, turning routine digital interactions into wealth-building opportunities. This suggests that while overall digital transactions are increasing, a growing portion is being intentionally directed towards savings.

Fostering a New Culture of Financial Discipline

For a generation that grew up with smartphones and instant gratification, the ability to automate financial discipline is a game-changer. Gen Z, with a 99.5% adoption rate for UPI, is at the forefront of this shift. Fintech platforms are capitalizing on this by integrating behavioural nudges, like automated savings features, directly into their apps. These tools help young users transition from being just spenders to becoming savers and investors, often for the first time. The digital records from UPI transactions also enhance financial literacy by making it easier to track expenses and see where money is going. Several studies note that while UPI can increase spending frequency, its utility in tracking and managing money promotes better financial habits among those who use it intentionally for budgeting and saving.

A Tool to Use Wisely

Despite its benefits, the power of automation comes with a caveat. The same set-and-forget convenience that helps grow savings can also lead to unnoticed financial leaks from forgotten subscriptions or unnecessary recurring charges. The growth in the subscription economy means young users often have multiple auto-debits running simultaneously. Therefore, financial discipline isn't just about setting up automated savings; it's also about periodically reviewing all automated payments. Many UPI apps now provide a dashboard to view, pause, or cancel mandates, giving users control over their recurring financial commitments. Mindful usage remains key to ensuring that automation serves long-term financial goals rather than detracting from them.