What is an Emergency Fund and Why Bother?

Think of an emergency fund as your personal financial firefighter. It's a pool of money set aside specifically for unexpected life events: a sudden medical expense, urgent home repairs, or a period of job loss. It’s not for planned purchases or discretionary

spending. Financial experts generally recommend having enough saved to cover three to six months' worth of essential living expenses. For a young person starting their career, this cushion provides peace of mind and prevents you from derailing your long-term financial goals or falling into high-interest debt when a crisis hits. An emergency fund gives you the stability to handle setbacks without stress.

The Old Way vs. The 'Set It and Forget It' Method

Traditionally, saving required active discipline. You’d have to remember to manually transfer money from your primary account to a savings account each month. It’s a process that relies heavily on willpower, and it’s easy to forget or decide to skip a month. This is where automation changes everything. The modern approach leverages technology you already use daily. By setting up an automated transfer, you treat your savings contribution like any other recurring bill. It happens in the background without you needing to do anything, removing the friction and the element of choice that often derails good intentions.

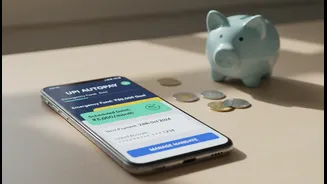

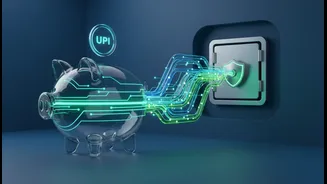

Enter UPI AutoPay: Your Personal Savings Assistant

Launched by the National Payments Corporation of India (NPCI), UPI AutoPay is a feature that allows you to authorize recurring payments from your bank account. You create a one-time 'mandate' for a specific merchant or platform, setting the amount, frequency (daily, weekly, monthly), and duration. Once you approve this mandate with your UPI PIN, the payments are debited automatically on the scheduled dates. While commonly used for bills and subscriptions, this tool is perfectly suited for building savings through Systematic Investment Plans (SIPs) in mutual funds. It’s the ultimate “set it and forget it” system for disciplined investing.

How to Automate Your Emergency Fund Savings

Setting up your automated emergency fund is a straightforward process. First, choose a suitable investment platform, such as a mutual fund app. For an emergency fund, the goal is capital safety and liquidity, not high returns. Therefore, select a low-risk investment option like a liquid fund or an overnight fund, which primarily invests in short-term securities. When you set up your SIP, choose UPI AutoPay as the payment method. You'll be prompted to create a mandate where you define the SIP amount and frequency. Review the details carefully, authorize it once with your UPI PIN, and you're done. Your bank will now automatically transfer the amount on the scheduled date each month. You’ll receive a pre-debit notification a couple of days before the transaction to ensure you have sufficient balance.

Why This Method Is Ideal for Young Earners

For young people, starting with a small, manageable amount is key. A SIP via UPI AutoPay allows you to begin investing with as little as a few hundred rupees. This consistency helps build a significant corpus over time without feeling like a major financial burden. The process is entirely digital, fitting seamlessly into a tech-savvy lifestyle. By automating the process, you effectively 'pay yourself first,' ensuring your savings goals are prioritized before other discretionary spending. It transforms saving from a chore into a disciplined, background habit, making financial resilience achievable for everyone.

Smart Practices and What to Watch For

While automation is powerful, it’s not a substitute for awareness. It's wise to start with a small amount and gradually increase it as your income grows. Always ensure you have enough funds in your bank account on the debit date to avoid the mandate failing. It's also good practice to regularly review your active mandates through your UPI app. This helps you keep track of your automated payments and cancel any that are no longer needed. Remember, an emergency fund should be kept separate from your long-term, higher-risk investments like stocks. The priority here is quick accessibility and capital preservation.