Choose the Correct ITR Form

The first and most fundamental check is ensuring you've selected the right Income Tax Return (ITR) form. Filing the wrong one can lead to your return being classified as 'defective' by the tax department, causing unnecessary delays. The choice depends

on your income sources. For most salaried individuals with an income up to ₹50 lakh and simple interest income, ITR-1 (Sahaj) is the right choice. However, if you have any income from capital gains (like selling stocks or mutual funds), multiple house properties, or foreign assets, you'll likely need to file ITR-2. Those with income from a business or profession must use ITR-3 or ITR-4. Take a moment to review your income sources for the financial year before you begin.

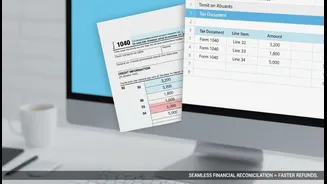

Reconcile with Form 26AS and AIS

Think of your Annual Information Statement (AIS) and Form 26AS as the tax department's report card on your finances. The biggest mistake taxpayers make is filing their return without cross-checking these documents. Your Form 26AS shows the tax deducted at source (TDS) and taxes you've paid. The AIS is much more comprehensive, listing transactions like savings account interest, dividend income, and securities transactions. Mismatches between the income you declare and what's shown in your AIS are a primary trigger for tax notices. Before filing, download both documents from the e-filing portal and ensure every reported income and TDS credit matches your records.

Report All Sources of Income

It’s easy to focus on your primary salary and forget about smaller income streams, but the tax department won't. A common oversight is failing to declare interest earned from savings bank accounts, fixed deposits, or recurring deposits. While TDS might not be deducted on all interest income, it is still taxable and must be reported. Other frequently missed items include rental income, freelance earnings, and gains from investments. The AIS now captures most of this information directly from banks and financial institutions, so failing to report it is a surefire way to get flagged for discrepancies.

Claim All Eligible Deductions

If you're opting for the old tax regime, don't leave money on the table. Many taxpayers stick to the popular Section 80C deductions (like PPF and life insurance) and overlook others they are eligible for. For instance, contributions to the National Pension System (NPS) offer an additional deduction of up to ₹50,000 under Section 80CCD(1B). Interest from a savings account is deductible up to ₹10,000 under Section 80TTA. You can also claim deductions for health insurance premiums (Section 80D), interest on education loans (Section 80E), and even rent paid if you don't receive HRA (Section 80GG). Keep all proofs of investment and expenditure handy.

Pre-Validate Your Bank Account

This is a crucial step, especially if you are expecting a tax refund. The Income Tax Department will only issue refunds to a pre-validated bank account that is linked to your PAN. An incorrect account number, a different name on the account, or a wrong IFSC code can cause your refund to fail or be significantly delayed. You can pre-validate one or more bank accounts through the official e-filing portal. Log in, go to the 'My Profile' section, and add or validate your bank details. It’s a simple check that ensures your refund reaches you without any glitches.

Don't Forget to E-Verify

Simply submitting your ITR is not the final step. Your return is considered invalid until it is verified. The deadline for verification is 30 days from the date of filing. Failing to do so is equivalent to not having filed at all and can lead to penalties and the rejection of refund claims. The easiest way to verify is electronically, a process known as e-verification. You can do this instantly using an Aadhaar OTP, your bank account through an Electronic Verification Code (EVC), or net banking. This final check closes the loop on your tax filing process.