Understanding ITR Mismatches

An ITR mismatch occurs when the information you declare in your income tax return does not align with the data available with the Income Tax Department. This data is collected from various third-party sources, such as banks, employers, and financial institutions,

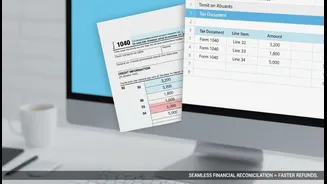

and is consolidated in your Annual Information Statement (AIS) and Form 26AS. Common reasons for mismatches include differences in reported income, incorrect claims for Tax Deducted at Source (TDS), or simple data entry errors. For instance, the interest income your bank reports might be different from what you declared, or your employer may have made an error while filing their TDS return. These discrepancies can lead to delayed refunds, demand notices, and potential penalties if left unaddressed.

The Old Way of Fixing Things

Previously, resolving ITR mismatches, especially those identified after an assessment order, was often a lengthy process. It required filing a formal rectification request under Section 154 of the Income-tax Act, 1961. This often involved manual intervention from jurisdictional Assessing Officers (AOs), leading to administrative delays and prolonged uncertainty for the taxpayer. The communication between different tax department wings, like the Centralized Processing Centre (CPC) in Bengaluru and the local AO, could be slow, leaving taxpayers waiting for their corrected refunds or demand notices to be nullified.

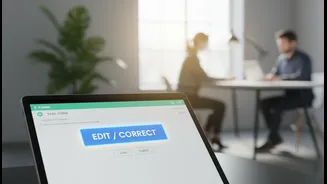

The New Route: On-Screen Functionality

The Central Board of Direct Taxes (CBDT) has introduced new 'on-screen' functionalities to streamline the correction process. This initiative, part of the e-Verification Scheme, allows taxpayers to reconcile certain mismatches directly on the income tax compliance portal. For discrepancies related to interest and dividend income, the portal provides a self-contained feature where you can review the mismatch and furnish your response directly online, without needing to upload any documents. This is a significant step towards a more transparent and less intrusive system, allowing taxpayers to provide feedback or accept the discrepancy.

Fixing Tax Credit Mismatches Online

For the most common issue—tax credit mismatches—the e-filing portal offers a dedicated rectification option. If you've received an intimation notice under Section 143(1) highlighting a mismatch in TDS, TCS, advance tax, or self-assessment tax, you can file a 'Tax Credit Mismatch Correction' request. The process is straightforward: log in to the portal, navigate to 'Services' and then 'Rectification', select the relevant assessment year, and choose this specific request type. The portal allows you to review and edit the details of the tax payments in question. This empowers you to correct challan details or update TDS entries that the system may have missed, ensuring you get the full credit you're entitled to.

What if the Mistake Is in Your Original ITR?

It's important to distinguish between a processing error by the department and a mistake in your own filing. The rectification process is primarily for correcting errors 'apparent from the record' after your return has been processed. If you realise you have under-reported income or made a wrong claim before the due date, you should file a Revised ITR under Section 139(5). If the deadline for a revised return has passed, you can use the Updated Return (ITR-U) under Section 139(8A). ITR-U allows you to voluntarily declare additional income and pay the due tax, often helping to avoid stricter penalties down the line, though it usually involves paying an additional tax.