The Reality of the June Numbers

India's retail inflation, measured by the Consumer Price Index (CPI), rose to around 4.4% in June 2026. This is an 18-month high and marks the first time in over a year that inflation has crossed the Reserve Bank of India's 4% target. The main drivers

behind this increase are no surprise to anyone who has been to the market or the petrol pump recently: food and fuel. Food inflation specifically climbed to over 5.3%, pushed up by essentials like vegetables and the impact of a weaker-than-expected monsoon. Meanwhile, transport costs also jumped significantly, reflecting higher global fuel prices. While the headline number is a cause for attention, it's not a signal for alarm. It reflects specific pressures, many of which are external or seasonal, rather than a runaway collapse in the economy.

Why Panic Budgeting Backfires

When financial anxiety hits, the first reaction is often to make deep, immediate cuts. This is 'panic budgeting'—deciding overnight to stop all discretionary spending, cancel all subscriptions, and live on the bare minimum. While it feels proactive, this approach is rarely sustainable. Extreme restrictions can lead to 'budget fatigue,' where you become so tired of deprivation that you eventually overspend, undoing all your hard work. Furthermore, unplanned cuts can sometimes cost you more in the long run. Forgoing a necessary vehicle service to save money today, for instance, could lead to a much larger repair bill tomorrow. The goal isn't to stop living; it's to spend more consciously.

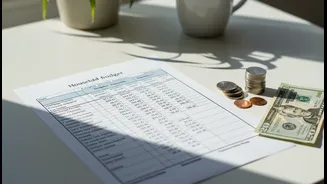

Your Guide to Tracking Essentials

The most powerful tool against inflation isn't cutting, it's tracking. Before you can make smart decisions, you need to know exactly where your money is going. Start by categorising your expenses. A popular method is the 50/30/20 rule: 50% of your income for 'Needs,' 30% for 'Wants,' and 20% for 'Savings & Debt Repayment'. Needs are the true essentials: rent or housing loan EMIs, utility bills, groceries, transport to work, and insurance premiums. Wants are everything else: dining out, entertainment, shopping for non-essentials, and hobbies. For one month, track every single rupee. You can use a dedicated app, a simple spreadsheet, or even a notebook. At the end of the month, you’ll have a clear, honest picture of your financial habits, free from guesswork.

Making Smart Adjustments, Not Sudden Cuts

Once you have your spending data, you can make informed adjustments. Look at your 'Wants' category. Are there any subscriptions you forgot you had? Can you reduce the frequency of ordering food in from three times a week to one? Instead of eliminating your entertainment budget, could you switch from expensive outings to more affordable options like hosting friends at home? The key is to make small, sustainable trims rather than eliminating entire categories of spending that bring you joy. Being a smart shopper also helps—taking advantage of sales for necessary items, buying non-perishables in bulk, and using discounts can stretch your rupee further without reducing your quality of life.

The Power of a One-Week Pause

If you're still feeling overwhelmed, try a 'no-spend challenge' for a short period, like one week. During this time, commit to spending money only on absolute essentials—the items on your 'Needs' list. This isn't a long-term strategy, but a short-term reset. It forces you to become hyper-aware of your impulses and distinguish between a genuine need and a fleeting want. You might discover that the daily coffee you thought was a 'need' feels more like a 'want' when you have to consciously justify the expense. This exercise builds financial mindfulness, which is a far more valuable asset than the few hundred rupees you might save in that week.