The 'Set It and Forget It' Savings Method

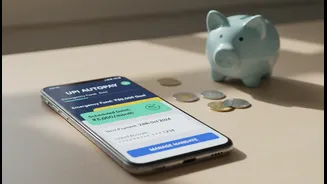

At its core, the 'hack' is surprisingly simple. It involves using the Unified Payments Interface (UPI) AutoPay feature, which was designed by the National Payments Corporation of India (NPCI) for recurring payments like bills and subscriptions. Young

users are creatively repurposing this tool. Instead of paying a merchant, they set up mandates to automatically transfer small, regular amounts from their primary bank account to a secondary savings account, a digital gold provider, or a mutual fund SIP. The process is straightforward: set a mandate once with your UPI PIN for a certain amount and frequency—daily, weekly, or monthly—and the system takes care of the rest. This transforms the act of saving from a conscious, often-postponed decision into an invisible, automated background process.

A Generation Hardwired for Digital

Gen Z grew up with smartphones and instant digital solutions, so it's no surprise they gravitate towards an app-based, automated approach to finance. This generation is accustomed to managing their lives through a few taps on a screen, and UPI fits perfectly into that lifestyle. They are less likely to use physical bank forms or set up traditional standing instructions, which can feel cumbersome. UPI AutoPay offers an instant, paperless, and fully controllable alternative right within the apps they use daily like Google Pay, PhonePe, or Paytm. This digital-native preference, combined with a growing awareness of financial wellness, makes the automated nature of this 'hack' particularly appealing. They can start small, building wealth consistently without the friction of legacy banking systems.

The Psychology of 'Paying Yourself First'

This method's effectiveness is deeply rooted in behavioural psychology. The core principle is 'pay yourself first', but with a modern twist. By automating savings, it removes the need for willpower and discipline, which are exhaustible resources. Psychologically, it's hard for our brains to prioritize a distant future reward over immediate gratification. Automation circumvents this 'temporal discounting' bias. When money is moved to savings before it can be spent, it's less likely to be used for impulse buys. The process becomes frictionless, turning a good intention into a consistent habit. Over time, watching these small, automated savings grow can even provide a dopamine hit, positively reinforcing the behaviour and making it easier to stick with.

The Perks of Automated Discipline

The primary benefit of this strategy is consistency. Automating payments ensures that saving happens regularly, whether it's ₹50 a day or ₹500 a week, helping to build a substantial corpus over time through the power of compounding. It enforces a discipline that many find difficult to maintain manually. It also helps in better cash flow management by earmarking funds for savings before they enter the general spending pool. For many, linking UPI AutoPay to a Systematic Investment Plan (SIP) in mutual funds has become a popular route, with AMFI reporting that UPI now accounts for a significant portion of new SIP registrations. This shows how the hack is not just about saving, but also about investing for long-term growth.

Potential Pitfalls to Watch For

While powerful, this 'hack' is not without risks. The main danger is losing track of active mandates. It's easy to set up a mandate and forget about it, leading to 'subscription creep' where small amounts are debited for services no longer used. Another risk is insufficient funds; if an auto-debit is triggered when your primary account balance is low, it could lead to payment failures or, in some cases, penalties. Although UPI AutoPay mandates can be paused or cancelled easily within the app, it requires active monitoring from the user. It’s also crucial to remember that for transactions above ₹15,000 (or up to ₹1 lakh for specific categories like insurance and mutual funds), manual PIN authentication is required, which adds a layer of security.