First, What Are Fund Categories?

Think of fund categories as labels that tell you a fund's primary investment style. In 2017, the Securities and Exchange Board of India (SEBI) standardised these to make life easier for investors. The main buckets are Equity, Debt, and Hybrid funds. Equity funds buy

stocks and aim for long-term growth, but come with higher risk and volatility. Debt funds invest in fixed-income instruments like bonds, prioritising stability and regular income over high growth. Hybrid funds, as the name suggests, mix both equity and debt to balance risk and return. These broad groups are broken down further; for instance, equity funds are sub-divided into large-cap, mid-cap, and small-cap based on the size of the companies they invest in. This categorisation isn't just jargon; it's a clear indicator of a fund's risk level and return potential.

Then, What Is a Holding Period?

Your holding period, or investment horizon, is simply the length of time you plan to stay invested before you need your money back. It’s not a random number; it’s directly tied to your financial goals. Are you saving for a vacation next year? That’s a short-term horizon. Planning for your child’s college education in 10 years? That’s a medium-to-long-term horizon. Saving for retirement in 25 years? That's a classic long-term horizon. Defining this timeframe is one of the most important steps in creating an investment plan, as it dictates how much risk you can comfortably take. A longer horizon gives your investments more time to recover from market downturns, while a shorter one demands a focus on protecting your capital.

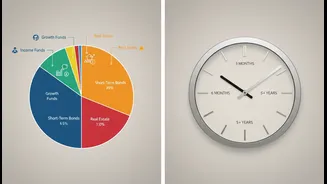

The Critical Link: Matching Risk to Time

This is where the two concepts merge. The core principle is simple: the risk profile of your chosen fund category must align with your investment holding period. High-risk categories require long holding periods, while low-risk categories are suitable for short ones. Equity funds, especially volatile ones like small-cap funds, need a long runway—ideally seven years or more—to ride out market cycles and allow the power of compounding to work. Investing in an equity fund for a goal that's only a year away is a gamble; a sudden market dip could force you to sell at a loss. Conversely, low-risk debt instruments like liquid funds are designed for short-term goals, from a few days to a year. Using them for a long-term goal like retirement means your money will likely fail to outpace inflation, eroding your wealth over time.

How Misalignment Hurts Your Portfolio

When your fund choice and time horizon are mismatched, you invite poor outcomes. Consider an investor who puts money for a home down payment needed in two years into a small-cap fund, lured by its recent high returns. A market correction could wipe out a significant portion of the capital, derailing the purchase. This is a classic mistake of chasing past performance without considering the associated risk and required time commitment. On the other end, imagine a young investor putting their retirement savings into an ultra-short-term debt fund. While the capital is safe, the returns will be minimal. Over 20 or 30 years, they will miss out on the substantial growth that equity markets historically provide over long periods, resulting in a much smaller retirement corpus. A mismatch works both ways, either by exposing you to inappropriate risk or by shackling your potential for growth.

The Tax Angle: Why Holding Periods Matter More

The tax you pay on your gains is also directly tied to your holding period. For equity funds, a holding period of more than 12 months classifies your profit as Long-Term Capital Gains (LTCG). As of 2026, LTCG up to ₹1.25 lakh is exempt, with gains beyond that taxed at a concessional rate of 12.5%. If you sell within 12 months, your profit is a Short-Term Capital Gain (STCG), taxed at a higher 20% rate. For debt funds purchased after April 1, 2023, the rules have changed; all gains are now added to your income and taxed at your applicable slab rate, removing the previous LTCG benefit. This tax structure explicitly encourages long-term investing in equities, rewarding patient investors with lower tax rates. Redeeming too early not only exposes you to market volatility but also results in a bigger tax bill.