What is the story about?

As the year draws to a close, Indian credit card users are taking stock of a period of significant change. Banks across the country revised fees, rewards

and benefits through 2025, even as regulators stepped up efforts to improve transparency and strengthen consumer protection.

Looking ahead, technological shifts—particularly the growing use of artificial intelligence—are set to reshape how millions of customers manage, monitor and use credit in 2026.

Key changes announced in 2025

Several leading banks revised credit card features mid-year.

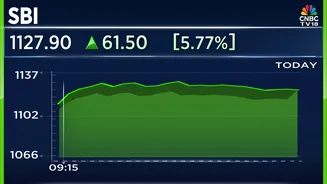

SBI Cards discontinued complimentary air accident insurance for premium and mid-tier cardholders and updated the order of payment settlement, impacting how payments are allocated across GST, EMIs, fees, and retail spends.

HDFC and ICICI Bank introduced new fees on online gaming, digital wallet loads, and high-value utility payments, alongside tightened reward structures and revised airport lounge access rules tied to spending thresholds or vouchers.

Kotak Mahindra Bank discontinued the Myntra Kotak Credit Card, transitioning users to the Kotak League Credit Card.

On the product front, the IndiGo and IDFC FIRST Bank co-branded credit card launched with benefits tailored for travel and everyday spending, supporting both RuPay and Mastercard networks. Regulators also played a crucial role: the RBI focused on enhancing transparency and reducing hidden charges, while the NPCI incentivized wider adoption of domestic RuPay cards.

What lies ahead in 2026?

Looking forward, banks plan further revisions.

ICICI Bank will enforce new reward caps and additional charges on online gaming, wallet loads, and high-value transport spends, while IDFC FIRST Bank is set to reduce rewards and lounge access benefits on popular cards like Mayura and Ashva.

SBI and HDFC will also tie lounge access eligibility to spend thresholds, marking a shift from automatic benefits.

Experts note that technology will play a growing role in personal credit management.

Tanish Sharrma, co-founder of BillCut, highlighted that AI-driven platforms are expected to optimise repayment schedules, reduce interest burdens, and provide personalised financial guidance at scale.

With India’s vast credit-eligible population, AI is projected to make credit management more proactive, shifting from static credit scores to dynamic, behavior-driven insights.