1. Treat Digital Payments Like Cash

The single most important mindset shift is understanding that most peer-to-peer (P2P) payment apps are designed to work like digital cash. When you hand someone a $20 bill, you don’t get it back if you later realize you gave it to the wrong person. Instant

payment networks like Zelle are often built directly into banking systems, and once the money is sent, it's gone in seconds. Unlike credit card transactions, which have robust fraud protections and dispute processes, P2P transfers offer very limited recourse. If you send money to a scammer or to the wrong username by mistake, the bank is often not obligated to reverse the transaction. Adopting a “cash mentality” forces you to pause and appreciate the finality of hitting ‘Send’.

2. The Golden Rule: Only Pay People You Know

Payment apps themselves constantly remind users of this, yet it’s the most frequently broken rule. P2P services were created to simplify payments between friends, family, and trusted individuals—think splitting a dinner bill, paying a babysitter, or sending a birthday gift. They were not designed for commercial transactions with strangers you meet online. Scammers prey on this by posting fake concert tickets, phantom puppies, or non-existent apartment rentals on social media or marketplace sites, demanding payment via Zelle or Cash App. Once you send the money for that “must-have” item, the seller vanishes and your money is gone. If a deal with a stranger requires an instant, irreversible payment, consider it a major red flag.

3. Always Double-Check the Recipient

A simple typo can cost you dearly. Scammers know this and sometimes create usernames that are deceptively similar to legitimate ones. Before you confirm any payment, take five extra seconds to verify the recipient’s details. Are you sending it to the right username, phone number, or email address? If you’re paying someone for the first time, consider sending a $1 test transaction first. Ask them to confirm they received it before you send the full amount. This small step can prevent a costly mistake, whether you’re paying a new contractor or just trying to send your friend money for pizza. It feels like an unnecessary delay in an “instant” world, but it’s one of the most effective safeguards you can employ.

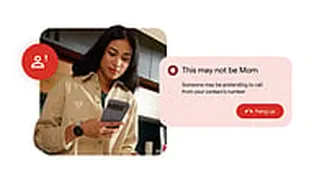

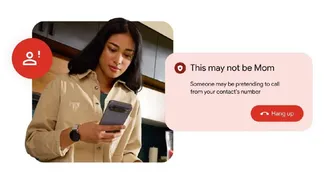

4. Recognize Common Scam Tactics

Fraudsters are creative, but their tactics often follow predictable patterns. Be wary of a “wrong number” scam where someone “accidentally” sends you money and then frantically asks you to send it back; they may have sent it from a stolen credit card, and when the original charge is reversed, you’re out the money you sent. Another classic is the fake alert: you receive a text message or email that looks like it’s from your bank or a payment app, warning you of a fraudulent transaction and asking you to click a link or call a number to stop it. This is a phishing attempt to steal your login credentials. Never click these links. Instead, log into your banking or payment app directly to check for any alerts.

5. Enable Every Security Feature Available

Your phone and your financial apps are packed with security tools—use them. Start with the basics: set up multi-factor authentication (MFA) on every financial app. This means that even if a scammer steals your password, they can’t log in without a second code sent to your phone or email. Enable transaction alerts, so you get an immediate notification via text or email every time money moves in or out of your account. Use biometric security like fingerprint or face ID to lock the apps themselves. These layers of protection create a digital fortress around your money, making it significantly harder for unauthorized users to gain access and drain your funds.