The Need for Speed in Your Wallet

For decades, moving money between banks was a sluggish affair, often taking several business days for a transfer to clear. That reality is fading fast. The rise of peer-to-peer (P2P) payment apps like Zelle, Venmo, and Cash App conditioned millions of Americans

to expect instant transactions. Now, the entire U.S. banking system is getting a supercharge with FedNow, the Federal Reserve's real-time payment network that launched in 2023. This system allows money to move between participating banks in seconds, 24/7/365. The goal is efficiency: no more waiting for checks to clear or ACH transfers to process. Whether you're paying rent, splitting a dinner bill, or getting paid for a freelance gig, the money arrives almost immediately. On the surface, it’s a massive upgrade for consumers and small businesses alike.

The Irreversible Problem

Here's the catch: the speed that makes these systems so appealing is also their biggest vulnerability. Unlike a credit card transaction, which has built-in consumer protections allowing you to dispute a charge, most instant payments are final. Think of it like handing someone physical cash. Once it leaves your hand, you have very little recourse to get it back if you realize you've been scammed. This finality is a feature, not a bug; it guarantees the recipient that the funds are good. But for fraudsters, it's a golden opportunity. Current regulations, like Regulation E, primarily protect consumers from *unauthorized* transactions—meaning, when a hacker breaks into your account and sends money without your permission. They offer far less protection if you were tricked into *authorizing* the payment yourself, which is how most modern payment scams work.

A Playground for Scammers

Scammers have flocked to fast payment platforms precisely because of their speed and finality. The playbook is varied but often involves social engineering. You might get a text message that looks like a fraud alert from your bank, asking you to 'reverse' a fake transaction by sending money to yourself via Zelle—which actually sends it to the scammer. Or you could be contacted by someone impersonating a family member in distress, begging for immediate funds. Another common scheme involves online marketplace deals where a 'seller' insists on a Zelle or Venmo payment for an item they never intend to ship. By the time the victim realizes they've been duped, the money has been transferred out of the scammer's account and is long gone. The speed of the system means there's no window to halt the transaction once it's been initiated.

What 'Smart Security' Actually Looks Like

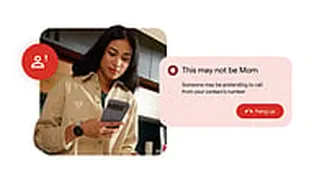

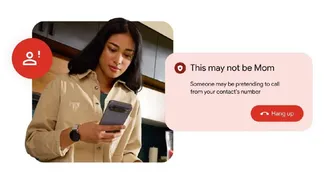

This is where the need for smarter security checks comes in. Banks and fintech companies can't just rely on passwords and two-factor authentication anymore. The next frontier is proactive, intelligent fraud detection. This involves using artificial intelligence and machine learning to analyze payment behavior in real time. For example, a smart system might flag a transaction if you're suddenly sending a large sum of money to a new recipient at 3 a.m., a pattern that deviates from your normal behavior. Some banks are implementing new warning screens that pop up before you confirm a payment to an unknown user, forcing you to acknowledge the risks. Others are creating delays or holding payments for review if a transaction is deemed high-risk, intentionally slowing things down to provide a cooling-off period and a chance for intervention.

Your Personal Security Checklist

While financial institutions are beefing up their defenses, your first line of defense is your own vigilance. The cardinal rule of fast payments is simple: only send money to people you know and trust. Treat it like digital cash. Never send money to someone you've only met online. Always verify requests for money, even if they appear to come from a friend or family member; call them at a known number to confirm. Be deeply skeptical of any message that creates a sense of urgency or fear, as this is a classic scammer tactic. Finally, enable every security feature your banking and payment apps offer, especially multifactor authentication, and set up alerts for any transaction that goes through your account.