What is the story about?

The recent weakness in the Indian rupee is being driven more by capital outflows than by a widening current account deficit, marking a shift from past episodes of currency pressure, according to D Subbarao, former Governor of the Reserve Bank of India (RBI). He said the underlying concern is not the rupee’s movement itself, but the broader trend of foreign and domestic capital pulling back from India.

Subbarao pointed to pressures on the capital account, particularly foreign portfolio investment (FPI) and foreign direct investment (FDI). On FPIs, he stated that a sharp rise in domestic retail participation—numbers that have tripled over the past decade—is displacing foreign investors. At the same time, elevated market valuations are encouraging foreign investors to book profits, while global capital is increasingly being diverted towards the artificial intelligence boom, creating a fear of missing out that is accelerating exits from markets like India.

On FDI, Subbarao cited recent comments by the Chief Economic Advisor to note that while gross inflows remain healthy, net inflows are turning negative as foreign companies repatriate retained earnings at attractive valuations. He argued that this raises deeper questions about investment confidence. “Why are foreign investors not continuing here? Why is domestic investment not taking place?” he asked, adding that this is a bigger concern than the rupee’s depreciation, which he believes is broadly tracking fundamentals.

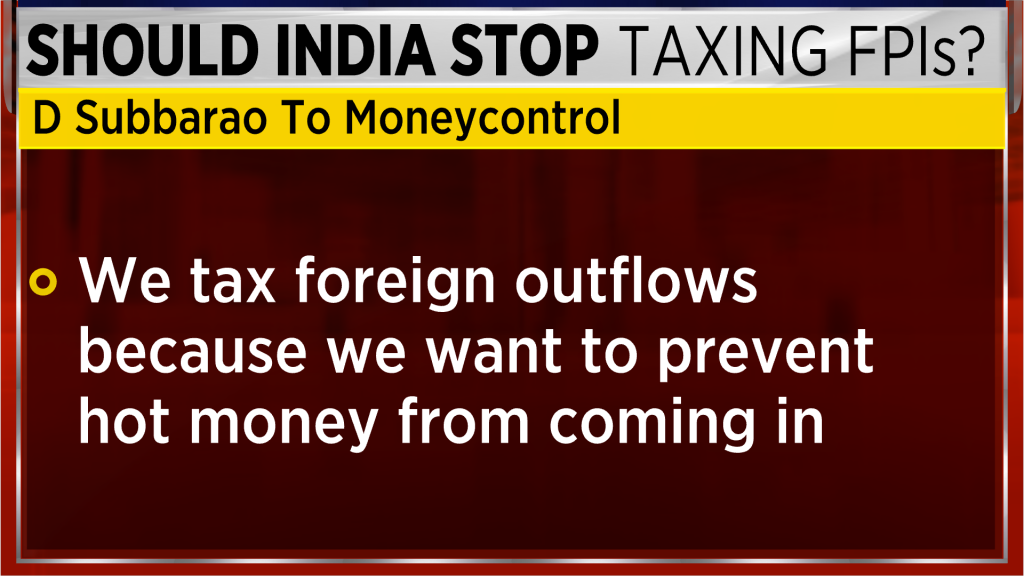

Subbarao also weighed in on India’s tax regime for foreign investors, clarifying that taxes on capital outflows are meant to discourage volatile “hot money” rather than raise revenue. He called for improvements in capital gains tax administration, arguing that uncertainty, not tax rates, is the real deterrent. He suggested fixing the tax regime for five years, publishing a comprehensive set of FAQs, and appointing a senior official to address investor concerns. He further distinguished between capital gains tax and withholding tax, arguing that while administration needs improvement for the former, the latter should be reduced, as high withholding taxes deter long-term, stabilising foreign capital.

Separately, Subbarao described India’s inflation-targeting framework and the Monetary Policy Committee (MPC) as a “plausible case,” saying they have strengthened the RBI’s independence. Reflecting on his tenure, he recalled facing pressure from finance ministers to stimulate growth during a period of policy paralysis. “The situation at that time was such, there was policy paralysis; the government could not do anything to push growth up, so they wanted the Reserve Bank to do something, be the cheerleader, inspire some confidence in the market,” he said, calling such pressure “understandable from a political perspective” but inappropriate from a technocratic standpoint.

He believes the current system offers greater insulation. “I believe it makes the RBI more independent because it's easier for the government to put pressure on one individual, the governor, rather than a committee,” Subbarao said, adding that the explicit inflation band creates a “more shared concern” between the government and the RBI when targets are breached. He dismissed early fears of political interference in MPC appointments, stating that “over the last 10 years, members of the MPC have been very credible, outstanding economists and analysts who've been there and MPC has established a record.”

However, Subbarao flagged two unresolved challenges. The first is supply-side inflation, a recurring issue in India. “If that happens, as is often the case, can RBI's monetary policy do the job of reining in inflation, and what does it do to the credibility of the inflation targeting framework? That question remains open,” he said. The second relates to the exchange rate. “The pass-through from exchange rate to inflation is high and getting higher. So, if the MPC is tasked with the responsibility of just inflation and not the exchange rate, can there be a conflict?” he asked, calling it a potential risk even though it has not yet materialised.

Overall, Subbarao said the framework has benefited from improved macroeconomic conditions. “The circumstances which we had some of us had reservations about, like the administered interest rate regime, a high fiscal deficit, which could undermine the inflation targeting framework, but they are less of a worry today. So, I think the circumstances for making the inflation targeting framework a success have also changed for the better,” he concluded.

Catch all the latest updates from the stock market here

Subbarao pointed to pressures on the capital account, particularly foreign portfolio investment (FPI) and foreign direct investment (FDI). On FPIs, he stated that a sharp rise in domestic retail participation—numbers that have tripled over the past decade—is displacing foreign investors. At the same time, elevated market valuations are encouraging foreign investors to book profits, while global capital is increasingly being diverted towards the artificial intelligence boom, creating a fear of missing out that is accelerating exits from markets like India.

On FDI, Subbarao cited recent comments by the Chief Economic Advisor to note that while gross inflows remain healthy, net inflows are turning negative as foreign companies repatriate retained earnings at attractive valuations. He argued that this raises deeper questions about investment confidence. “Why are foreign investors not continuing here? Why is domestic investment not taking place?” he asked, adding that this is a bigger concern than the rupee’s depreciation, which he believes is broadly tracking fundamentals.

Subbarao also weighed in on India’s tax regime for foreign investors, clarifying that taxes on capital outflows are meant to discourage volatile “hot money” rather than raise revenue. He called for improvements in capital gains tax administration, arguing that uncertainty, not tax rates, is the real deterrent. He suggested fixing the tax regime for five years, publishing a comprehensive set of FAQs, and appointing a senior official to address investor concerns. He further distinguished between capital gains tax and withholding tax, arguing that while administration needs improvement for the former, the latter should be reduced, as high withholding taxes deter long-term, stabilising foreign capital.

Also

Read: RBI may have spent $30 billion to shore up rupee in just four months

Separately, Subbarao described India’s inflation-targeting framework and the Monetary Policy Committee (MPC) as a “plausible case,” saying they have strengthened the RBI’s independence. Reflecting on his tenure, he recalled facing pressure from finance ministers to stimulate growth during a period of policy paralysis. “The situation at that time was such, there was policy paralysis; the government could not do anything to push growth up, so they wanted the Reserve Bank to do something, be the cheerleader, inspire some confidence in the market,” he said, calling such pressure “understandable from a political perspective” but inappropriate from a technocratic standpoint.

He believes the current system offers greater insulation. “I believe it makes the RBI more independent because it's easier for the government to put pressure on one individual, the governor, rather than a committee,” Subbarao said, adding that the explicit inflation band creates a “more shared concern” between the government and the RBI when targets are breached. He dismissed early fears of political interference in MPC appointments, stating that “over the last 10 years, members of the MPC have been very credible, outstanding economists and analysts who've been there and MPC has established a record.”

However, Subbarao flagged two unresolved challenges. The first is supply-side inflation, a recurring issue in India. “If that happens, as is often the case, can RBI's monetary policy do the job of reining in inflation, and what does it do to the credibility of the inflation targeting framework? That question remains open,” he said. The second relates to the exchange rate. “The pass-through from exchange rate to inflation is high and getting higher. So, if the MPC is tasked with the responsibility of just inflation and not the exchange rate, can there be a conflict?” he asked, calling it a potential risk even though it has not yet materialised.

Overall, Subbarao said the framework has benefited from improved macroeconomic conditions. “The circumstances which we had some of us had reservations about, like the administered interest rate regime, a high fiscal deficit, which could undermine the inflation targeting framework, but they are less of a worry today. So, I think the circumstances for making the inflation targeting framework a success have also changed for the better,” he concluded.

Catch all the latest updates from the stock market here