What is the story about?

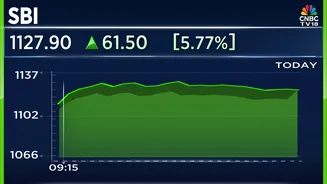

Shares of State Bank of India (SBI) emerged as the top gainer on the Nifty 50 index, rising 6% and posting its biggest single-day gain since June 2024 after its third quarter results.

SBI beat market estimates with a 24% growth in net profit at the end of the December quarter. The bank beat private peers like ICICI Bank and HDFC Bank in loan growth, and raised the guidance for the next financial year. Not surprisingly, a slew of increases in target prices have followed.

42 of the 49 analysts tracking the stock have a 'buy' rating, according to the latest Bloomberg data. At least five of them have raised their target prices.

Sequential loan growth was much better than peer PSU banks as well as large private sector banks, according to CLSA.

SBI’s core earnings are stronger than private banks for third consecutive quarter with stable net interest margin, higher than sector loan growth and strong fees, Nuvama highlighted.

Overall, a combination of strong growth, improved margins, and better asset quality kept return on assets (RoA) comfortably above 1% mark and return on equity (RoE) above 20%: Bernstein.

A substantial portion of re-rating has already played out, and the subsequent increase in SBI stock would be largely driven by earnings, and not bigger multiples, analysts at Nomura said.

The consensus on the street is that SBI shares may rise to ₹1189.38, more than 11% higher from Friday's closing price. The stock has gained over 44% in the last year.

Speaking to CNBC-TV18, Nitin Aggarwal of Motilal Oswal said that SBI may overshadow the growth of all three top private-sector banks.

The outlook for SBI in terms of growth, profits, and asset quality deserves further rerating, he added.

Track the latest market updates on the CNBC-TV18 daily live-blog.

SBI beat market estimates with a 24% growth in net profit at the end of the December quarter. The bank beat private peers like ICICI Bank and HDFC Bank in loan growth, and raised the guidance for the next financial year. Not surprisingly, a slew of increases in target prices have followed.

42 of the 49 analysts tracking the stock have a 'buy' rating, according to the latest Bloomberg data. At least five of them have raised their target prices.

| Brokerage | Rating | Target Price |

| Nomura | Buy | ₹1,235 |

| CLSA | Outperform | ₹1,275 |

| CITI | Buy | ₹1,265 |

| Bernstein | Market Perform | ₹1,100 |

| Jefferies | Buy | ₹1,300 |

| Nuvama | Buy | ₹1,250 |

| UBS | Neutral | ₹1,120 |

The following are some of the reasons cited by the analysts bullish on SBI's prospects going forward:

Sequential loan growth was much better than peer PSU banks as well as large private sector banks, according to CLSA.

Margins are expected to sustain at or above 3% and disciplined underwriting/credit protocols, alongside recoveries should support robust asset quality,

said CITI.

SBI’s core earnings are stronger than private banks for third consecutive quarter with stable net interest margin, higher than sector loan growth and strong fees, Nuvama highlighted.

Overall, a combination of strong growth, improved margins, and better asset quality kept return on assets (RoA) comfortably above 1% mark and return on equity (RoE) above 20%: Bernstein.

A substantial portion of re-rating has already played out, and the subsequent increase in SBI stock would be largely driven by earnings, and not bigger multiples, analysts at Nomura said.

The consensus on the street is that SBI shares may rise to ₹1189.38, more than 11% higher from Friday's closing price. The stock has gained over 44% in the last year.

Speaking to CNBC-TV18, Nitin Aggarwal of Motilal Oswal said that SBI may overshadow the growth of all three top private-sector banks.

The outlook for SBI in terms of growth, profits, and asset quality deserves further rerating, he added.

Track the latest market updates on the CNBC-TV18 daily live-blog.