Q3 Earnings Triumph

The State Bank of India (SBI) has set a new benchmark with its third-quarter fiscal year 2025-26 (Q3FY26) financial report, posting its highest-ever quarterly

profit of ₹21,028 crore, a substantial 24.5 per cent increase year-on-year. This performance not only surpassed market expectations but also cemented SBI's status as a preferred investment among analysts. The bank's net interest income (NII) saw a healthy rise of 9 per cent year-on-year, reaching ₹45,190 crore. Although the reported net interest margin (NIM) expanded by 2 basis points to 2.99 per cent, a slight adjustment for interest on tax refunds indicated a marginal dip in core NIM quarter-on-quarter. The bank's management foresees expanded lending avenues, particularly in real estate investment trusts (REITs) and merger and acquisition financing, following recent Reserve Bank of India (RBI) regulatory changes. This outlook, coupled with an upward revision of its credit growth guidance to 13-15 per cent from 12-14 per cent and an exit NIM projection of around 3 per cent for FY26, underpins a positive future trajectory.

Analyst Optimism Soars

Following the impressive Q3FY26 results, a wave of optimism has swept through the brokerage community, leading to upward revisions in earnings estimates and price targets for the State Bank of India (SBI) stock. Emkay Global Financial Services, for instance, has enhanced its earnings projections for FY26-28 by 2-4 per cent and set a new target price of ₹1,225. Similarly, Motilal Oswal Financial Services has boosted its earnings estimates for FY27 by 3 per cent and for FY28 by 4.3 per cent, anticipating a return on assets (RoA) of 1.1 per cent and a return on equity (RoE) of 15.9 per cent for FY27. This firm has also raised its target price for SBI shares to ₹1,300. The consensus among analysts is overwhelmingly positive, with data from Bloomberg indicating that 42 out of 49 analysts tracking the stock recommend a 'buy' rating. JM Financial Institutional Securities echoed this sentiment, maintaining a 'buy' rating and increasing their target price to ₹1,250 from ₹1,140, citing strong growth, resilient margins, and robust asset quality as key strengths that justify premium valuations.

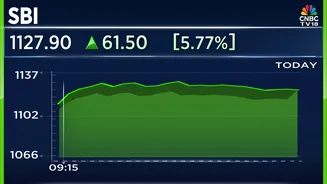

Stock Performance & Market Cap

The State Bank of India's stock experienced a significant surge following the release of its robust Q3FY26 financial results, reaching an all-time high. On the National Stock Exchange (NSE), SBI shares jumped 7.8 per cent to hit an intraday peak of ₹1,150. This marked the stock's most substantial single-day gain since June 2024, with approximately 40.8 million shares, valued at ₹4,633.17 crore, trading hands. The stock ultimately closed with a gain of 7.6 per cent, significantly outperforming the Nifty50 index's 0.68 per cent rise and the Nifty PSU Bank index's 3.34 per cent advance. Further underscoring its market strength, SBI's market capitalization surpassed the ₹10 trillion mark for the first time on a Monday, closing at an all-time high of ₹1,146 and valuing the institution at ₹10.6 trillion. This milestone positions SBI as the fifth most valuable company in India, trailing behind Reliance Industries, HDFC Bank, Bharti Airtel, and Tata Consultancy Services. Over the past year, SBI shares have appreciated by 55 per cent, considerably outperforming the Nifty50's 10 per cent gain.

Unmatched Asset Quality

SBI has demonstrated remarkable consistency in improving its asset quality, a key factor contributing to its strong financial performance and investor confidence. In the third quarter of FY26, the bank witnessed a reduction in both gross and net slippages by 3 basis points quarter-on-quarter. Furthermore, its gross non-performing assets (GNPA) ratio improved by 15 basis points to 1.57 per cent, and the net NPA (NNPA) ratio saw a 3 basis point improvement, settling at 0.39 per cent. Analysts have highlighted this as one of SBI's best asset quality prints in recent years. Complementing its lean asset profile, SBI maintains robust financial safeguards through substantial provisioning. The provision coverage ratio (PCR) stood firm at 75.5 per cent, indicating a strong buffer against potential loan losses. This combination of superior asset quality and fortified provisioning provides a solid foundation for the bank's sustained profitability and operational resilience, reinforcing its standing as a leading financial institution.