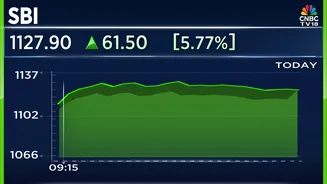

Record Profit Surge

The State Bank of India (SBI) recently announced a groundbreaking financial quarter, achieving its highest-ever quarterly profit. This remarkable achievement

has sent ripples through the market, causing its shares to surge by an impressive 7% and reach a new all-time high. The bank's net interest income (NII) demonstrated solid growth, climbing 9 percent year-on-year to ₹45,190 crore during the third quarter. This figure represents a healthy increase from the ₹41,445 crore earned in the same period of the previous year, underscoring the bank's core lending business's sustained strength. The positive financial results have not only boosted investor confidence but also prompted several financial analysts to revise their target prices upwards, signaling a strong belief in the bank's future performance.

Asset Quality & Guidance

Beyond the impressive profit figures, SBI also showcased significant improvements in its asset quality during the third quarter of FY26. The gross Non-Performing Asset (NPA) ratio saw a reduction, falling to 1.57 percent from 1.73 percent in the preceding quarter. Similarly, the net NPA ratio experienced a decline, moving from 0.42 percent to 0.39 percent. These improvements in asset quality indicate better credit management and a healthier loan book. Furthermore, the bank's provisions for the quarter stood at ₹4,506 crore, which was lower than the ₹5,400 crore set aside in the prior quarter and considerably less than the ₹911 crore from the same quarter a year ago, suggesting easing credit costs. The bank's management also demonstrated confidence in its future growth prospects by raising the loan growth guidance for FY26 to a range of 13–15 percent, up from the earlier projection of 12–14 percent.

Brokerage Upgrades & Targets

In response to SBI's outstanding quarterly performance, leading international brokerages have largely maintained their positive ratings and significantly increased their target prices for the bank's stock. Nomura, for instance, reiterated its ‘Buy’ call and boosted its target price to ₹1,235 per share, implying a potential upside of nearly 16 percent. The firm lauded SBI's strong all-around performance, noting better margin delivery and loan growth compared to its peers, driven by robust Net Interest Margins (NIMs), controlled operating expenses, and higher other income. CLSA also maintained an ‘Outperform’ rating with an elevated target price of ₹1,275, suggesting an upside of close to 20 percent. CLSA highlighted stronger-than-expected Q3 results, with core profit before provisioning and taxation (PPoP) and profit before tax (PBT) exceeding estimates. They also pointed out accelerated loan growth and improved NIMs due to a lower cost of deposits. Citi maintained its ‘Buy’ recommendation, raising the target to ₹1,265, citing core earnings that surpassed expectations and broad-based growth across various credit segments, leading to an optimistic loan growth outlook. Jefferies set a high target of ₹1,300, indicating a potential 22 percent upside, driven by increased other income and reduced credit costs. Nuvama also joined the chorus with a ‘Buy’ rating and a target of ₹1,250, acknowledging strong core earnings and improved loan and NII growth.