A Market Reaching Escape Velocity

The numbers underpinning the electric vehicle transition are staggering, signalling a fundamental rewiring of the automotive industry. In India, the EV market is projected to see a nearly 12-fold increase in annual sales to 30.4 million units by 2032.

This explosive growth is driving a parallel surge in battery demand, which is expected to grow from 19 GWh in 2025 to a colossal 362 GWh by 2032. Globally, the story is the same. Automakers are expected to invest a collective USD 1.2 trillion by 2030 into developing and producing EVs, batteries, and securing raw materials. The battery market in India alone was valued at around USD 12.65 billion in 2025 and is forecast to grow to USD 23.20 billion by 2032. This isn't just growth; it's the creation of an entirely new industrial base, where the battery is the central, non-negotiable element.

More Than Just a Fuel Tank

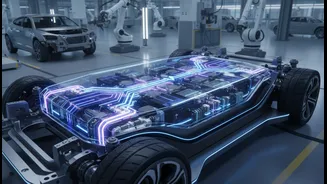

To view the battery as merely a replacement for the petrol tank is to miss the revolution entirely. It has become the vehicle's structural and digital backbone. Modern EV platforms are designed around the battery pack, which often forms the floor of the vehicle, influencing its rigidity, handling, and safety. But its role extends far beyond propulsion. The battery is the enabler of a vehicle's software-defined features, from over-the-air updates that enhance performance to advanced driver-assistance systems. Furthermore, the rise of Vehicle-to-Grid (V2G) technology transforms the car into a mobile energy asset. The V2G market, valued at around USD 7.8 billion in 2025, allows EV owners to sell power back to the grid during peak demand, stabilizing renewable energy sources and creating new revenue streams. This turns the car from a simple transportation device into an active participant in the energy infrastructure.

The Race to Control the Supply Chain

Recognising that batteries are the new center of gravity, automakers are in a frantic race to control their own destiny. Relying on third-party suppliers for the most critical and expensive component of an EV is a strategic vulnerability they are no longer willing to accept. This has triggered a wave of investment in vertical integration. In India, major players are establishing their own 'gigafactories'. Tata Group's Agratas is building a 40 GWh plant in Gujarat, aiming to supply its own brands like Tata Motors and JLR starting in 2026. Similarly, Ola Electric is investing heavily in its own cell production to reduce import dependency. This trend is global, creating regional manufacturing hubs like the 'Battery Belt' in the United States. By bringing battery design and production in-house, car companies can control costs, accelerate innovation, and secure supply in an increasingly competitive market.

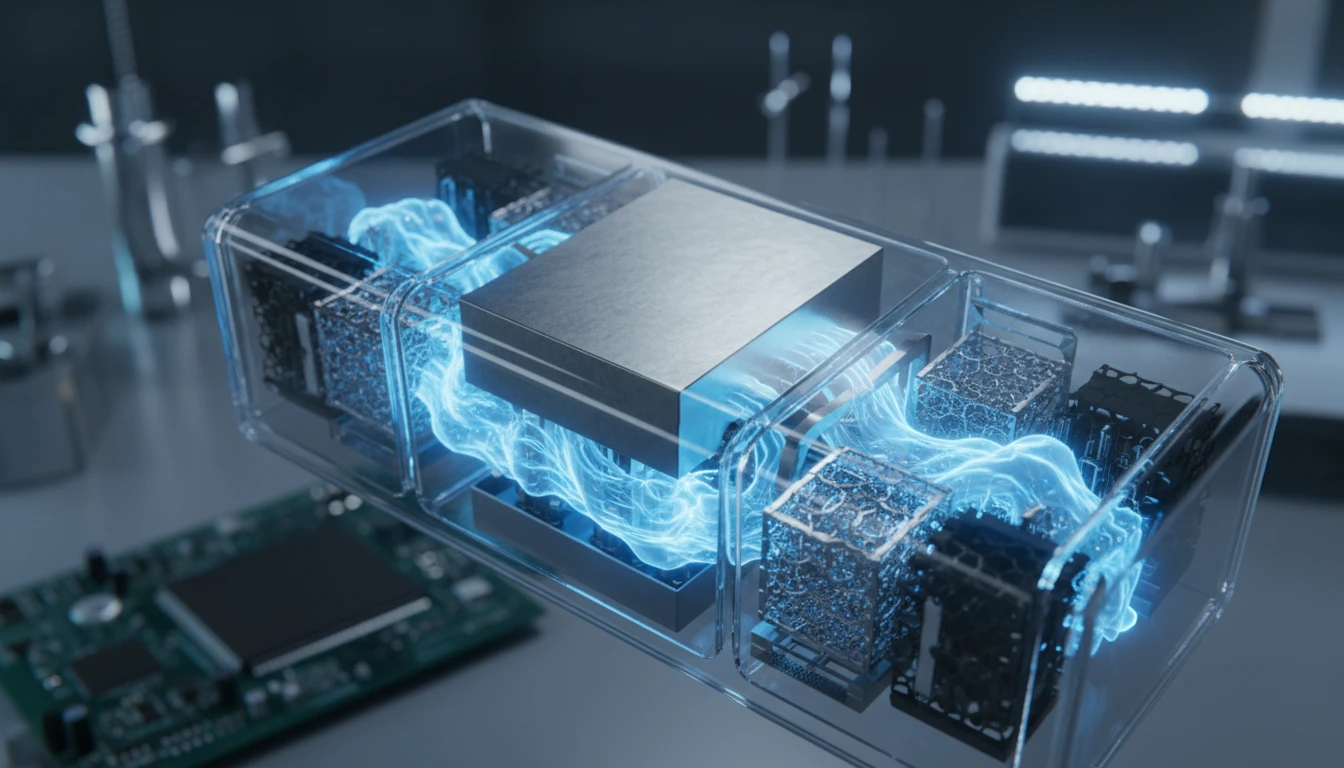

The Next Frontier: Chemistry and Innovation

The current dominance of lithium-ion technology is just the beginning of the story. The industry is on the cusp of the next great leap, with solid-state batteries being the most anticipated breakthrough. These batteries replace the flammable liquid electrolyte with a solid material, promising higher energy density (leading to longer range), faster charging, and improved safety. Automakers like Toyota and Nissan are targeting commercial deployment around 2028. Beyond solid-state, researchers are exploring a diverse range of chemistries like sodium-ion, which offers a cheaper and more abundant alternative for budget vehicles, and silicon anodes that dramatically boost energy storage. This isn't about finding a single 'silver bullet' but creating a portfolio of battery technologies tailored to different market segments, from affordable city cars to long-range luxury vehicles. The race to commercialize these next-gen batteries is a new front in the war for automotive supremacy.