/images/ppid_59c68470-image-177908510231472887.webp)

/images/ppid_a911dc6a-image-177925652958085792.webp)

What is the story about?

Rising global bond yields and persistent inflation pressures are forcing central banks, especially the US Federal Reserve, to rethink their easing stance, according to Ed Yardeni, President of Yardeni Research. Yardeni believes the bond market is effectively pushing the Fed toward a tightening bias, with the possibility of a rate hike as early as July if inflation concerns continue to build.

Despite short-term volatility driven by bond markets, geopolitics and higher yields, Yardeni remains constructive on equities. He expects the ongoing artificial intelligence (AI) led earnings boom, upcoming marquee initial public offerings (IPOs) and resilient corporate profits to keep the US and global bull market intact, while viewing any near-term correction as a buying opportunity rather than the start of a broader downturn.

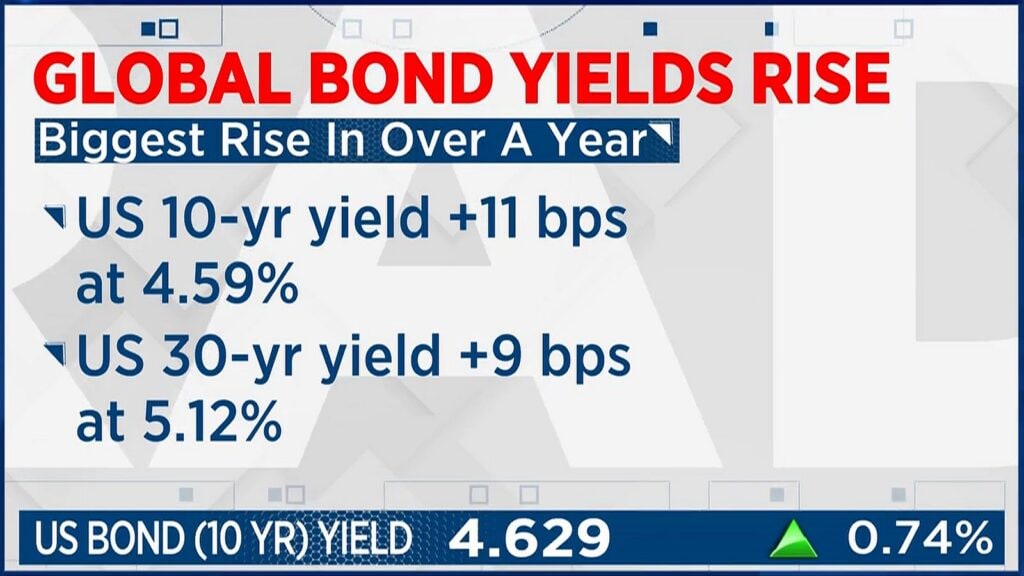

This is an edited transcript of the interview.Q: The interesting part is that the street was hoping for some de-escalation, given the spike seen in US bond yields. Do you think markets are now comfortable with bond yields staying above the 4.5% mark?

This is an edited transcript of the interview.Q: The interesting part is that the street was hoping for some de-escalation, given the spike seen in US bond yields. Do you think markets are now comfortable with bond yields staying above the 4.5% mark?

A: It is interesting that bond yields spiked on Friday, which was also the first day of Kevin Warsh as Fed Chair. The concern in the bond market is that the Fed Chair has been saying he wants lower rates, which makes no sense in the current economic environment.

I think it is becoming increasingly clear that the bond market is pushing the Fed to move from an easing bias, not just to a neutral bias, but to a tightening bias at the June meeting. That will probably be followed by a rate hike in July.

Also Read: Oil price pressure priced in, India offers selective opportunities: Raymond James strategist

Right now, the bond vigilantes are taking control of the global bond market and waiting for central bankers to take the inflation problem more seriously.

Q: Do you think Kevin Warsh will actually be allowed to do this?

A: No, there is no way he can be a lone dissenter. It is very unlikely that he will stand alone. He will have no choice but to go along with the consensus at the Federal Open Market Committee (FOMC).

I think the easing bias is long overdue to be replaced, not with a neutral bias, but with a tightening bias. Otherwise, it would be a terrible way to begin as Fed Chair by dissenting from almost every other vote.

Q: The moves in the UK and Japan yield are partly country-specific. Is there also a broader US read-through here?

A: This is definitely a global bond market sell-off. Bond yields are rising around the world, especially in developed economies with large fiscal deficits.

The longer the Strait of Hormuz remains closed, the more the bond market will conclude that interest rates will stay higher for longer.

I am relatively comfortable with US bond yields between 4.25% and 4.75%. There is a chance yields could touch 5%, where they briefly were in 2023, and I think that would be an extraordinary buying opportunity.

It is also interesting that oil prices have stayed around current levels. Brent is around $111, but it is extraordinary that prices are not even higher. Part of that is likely because China’s economy is not doing very well. The latest data suggests retail sales there remain extremely weak.

Q: Indian markets have underperformed recently. With yields spiking and the dollar index rising, do you think flows could move away from emerging markets?

Q: Indian markets have underperformed recently. With yields spiking and the dollar index rising, do you think flows could move away from emerging markets?

A: The reality is that emerging market exchange-traded funds (ETFs) like emerging markets ETF (EEM) and emerging markets ex China ETF (EMXC), excluding China, were very strong until last week, when South Korea and Taiwan saw sharp declines.

Emerging market indices have largely been pushed higher by the AI trade through South Korea and Taiwan. Both those markets probably need to pause for a while.

As an asset class, emerging markets may underperform temporarily. But honestly, it would actually be healthy if markets took a break here.

I think markets are entering more of a resting phase rather than a broader breakdown. We already saw a pullback earlier this year and could see another one into the summer. But once things settle, I still believe we remain in a bull market for equities in the US and globally.

Q: You have been accurate with your US market targets. What is your outlook now for the S&P 500 and also for Korea’s Kospi, where valuations remain below 10 times earnings?

A: We have had what I call an earnings-led melt-up, which is healthier and more sustainable than a valuation-led melt-up.

However, some people are starting to question the quality of those earnings because some AI companies own stakes in other AI companies, and rising valuations feed on themselves. That is a concern.

Last week, I raised my year-end target for the S&P 500 to 8,250. Maybe I called the top, but I do not think so. I believe earnings remain strong enough to justify further upside.

The market touched 7,500 on May 14th and then fell just 1.2% on May 15th, yet suddenly everyone started talking about bond crashes and calamities. I think this is another short-term buying opportunity, especially in the US stock market.

Watch the full conversation hereQ: How do you see the current tug-of-war between the bond market, the White House and geopolitical uncertainty playing out?

A: Kevin Warsh is a very smart individual and understands markets. I think he understands that the bond market is telling him the Fed needs to pivot toward a hawkish stance.

If the Fed does that responsibly, there is actually a better chance that bond yields stop rising further.

Nobody wants a repeat of what happened in 2021-2022, when the Fed was three to six months too late in tightening policy.

I would not be surprised if the Fed raises rates by 25 basis points at the June meeting itself, simply to send a message that it understands inflation risks and wants to take control rather than leaving all the heavy lifting to the bond market.

Q: Do your 8,250 S&P targets include the impact of major upcoming IPOs like Anthropic and OpenAI?

A: Yes, absolutely. We are going to see some very exciting IPOs — including SpaceX for sure. That will further juice up the market and bring investors back from the sidelines.

The future remains exciting despite all the short-term anxieties.

Catch all the latest updates from the stock market here

Despite short-term volatility driven by bond markets, geopolitics and higher yields, Yardeni remains constructive on equities. He expects the ongoing artificial intelligence (AI) led earnings boom, upcoming marquee initial public offerings (IPOs) and resilient corporate profits to keep the US and global bull market intact, while viewing any near-term correction as a buying opportunity rather than the start of a broader downturn.

This is an edited transcript of the interview.Q: The interesting part is that the street was hoping for some de-escalation, given the spike seen in US bond yields. Do you think markets are now comfortable with bond yields staying above the 4.5% mark?

A: It is interesting that bond yields spiked on Friday, which was also the first day of Kevin Warsh as Fed Chair. The concern in the bond market is that the Fed Chair has been saying he wants lower rates, which makes no sense in the current economic environment.

I think it is becoming increasingly clear that the bond market is pushing the Fed to move from an easing bias, not just to a neutral bias, but to a tightening bias at the June meeting. That will probably be followed by a rate hike in July.

Also Read: Oil price pressure priced in, India offers selective opportunities: Raymond James strategist

Right now, the bond vigilantes are taking control of the global bond market and waiting for central bankers to take the inflation problem more seriously.

Q: Do you think Kevin Warsh will actually be allowed to do this?

A: No, there is no way he can be a lone dissenter. It is very unlikely that he will stand alone. He will have no choice but to go along with the consensus at the Federal Open Market Committee (FOMC).

I think the easing bias is long overdue to be replaced, not with a neutral bias, but with a tightening bias. Otherwise, it would be a terrible way to begin as Fed Chair by dissenting from almost every other vote.

Q: The moves in the UK and Japan yield are partly country-specific. Is there also a broader US read-through here?

A: This is definitely a global bond market sell-off. Bond yields are rising around the world, especially in developed economies with large fiscal deficits.

The longer the Strait of Hormuz remains closed, the more the bond market will conclude that interest rates will stay higher for longer.

I am relatively comfortable with US bond yields between 4.25% and 4.75%. There is a chance yields could touch 5%, where they briefly were in 2023, and I think that would be an extraordinary buying opportunity.

It is also interesting that oil prices have stayed around current levels. Brent is around $111, but it is extraordinary that prices are not even higher. Part of that is likely because China’s economy is not doing very well. The latest data suggests retail sales there remain extremely weak.

Q: Indian markets have underperformed recently. With yields spiking and the dollar index rising, do you think flows could move away from emerging markets?

A: The reality is that emerging market exchange-traded funds (ETFs) like emerging markets ETF (EEM) and emerging markets ex China ETF (EMXC), excluding China, were very strong until last week, when South Korea and Taiwan saw sharp declines.

Emerging market indices have largely been pushed higher by the AI trade through South Korea and Taiwan. Both those markets probably need to pause for a while.

As an asset class, emerging markets may underperform temporarily. But honestly, it would actually be healthy if markets took a break here.

I think markets are entering more of a resting phase rather than a broader breakdown. We already saw a pullback earlier this year and could see another one into the summer. But once things settle, I still believe we remain in a bull market for equities in the US and globally.

Q: You have been accurate with your US market targets. What is your outlook now for the S&P 500 and also for Korea’s Kospi, where valuations remain below 10 times earnings?

A: We have had what I call an earnings-led melt-up, which is healthier and more sustainable than a valuation-led melt-up.

However, some people are starting to question the quality of those earnings because some AI companies own stakes in other AI companies, and rising valuations feed on themselves. That is a concern.

Last week, I raised my year-end target for the S&P 500 to 8,250. Maybe I called the top, but I do not think so. I believe earnings remain strong enough to justify further upside.

The market touched 7,500 on May 14th and then fell just 1.2% on May 15th, yet suddenly everyone started talking about bond crashes and calamities. I think this is another short-term buying opportunity, especially in the US stock market.

Watch the full conversation hereQ: How do you see the current tug-of-war between the bond market, the White House and geopolitical uncertainty playing out?

A: Kevin Warsh is a very smart individual and understands markets. I think he understands that the bond market is telling him the Fed needs to pivot toward a hawkish stance.

If the Fed does that responsibly, there is actually a better chance that bond yields stop rising further.

Nobody wants a repeat of what happened in 2021-2022, when the Fed was three to six months too late in tightening policy.

I would not be surprised if the Fed raises rates by 25 basis points at the June meeting itself, simply to send a message that it understands inflation risks and wants to take control rather than leaving all the heavy lifting to the bond market.

Q: Do your 8,250 S&P targets include the impact of major upcoming IPOs like Anthropic and OpenAI?

A: Yes, absolutely. We are going to see some very exciting IPOs — including SpaceX for sure. That will further juice up the market and bring investors back from the sidelines.

The future remains exciting despite all the short-term anxieties.

Catch all the latest updates from the stock market here

/images/imfZ6nBC-image-177925728082881439.webp)

/images/ppid_59c68470-image-177925752366888315.webp)

/images/ppid_59c68470-image-177925755298533154.webp)