/images/ppid_59c68470-image-177821509956426337.webp)

/images/ppid_59c68470-image-177799270947840795.webp)

/images/ppid_59c68470-image-17780000316803521.webp)

What is the story about?

PR Seshadri, MD & CEO of South Indian Bank, expects loan growth of 15-16% in FY27 as asset quality continued to improve during the January-March 2026 quarter.

He said slippages and credit costs remained near historical lows, with the bank’s quarterly slippage ratio at 15 basis points. Recoveries were trending at around ₹400 crore against NPA slippages of nearly ₹150 crore, helping net NPA levels decline to nearly 29 basis points.

“We think that 15% to 16% growth should be reasonable,” he said, adding that the lender will continue to prioritise retail and MSME lending over corporate loans.

Seshadri said the bank was closely monitoring the West Asia conflict but had not made any specific provisions yet because the situation remained uncertain.

“We do think that the West Asia crisis will have an overall negative impact on portfolio performance,” he said, while noting that the bank does not have direct exposure to airlines and has limited exposure to government-owned petroleum refiners.

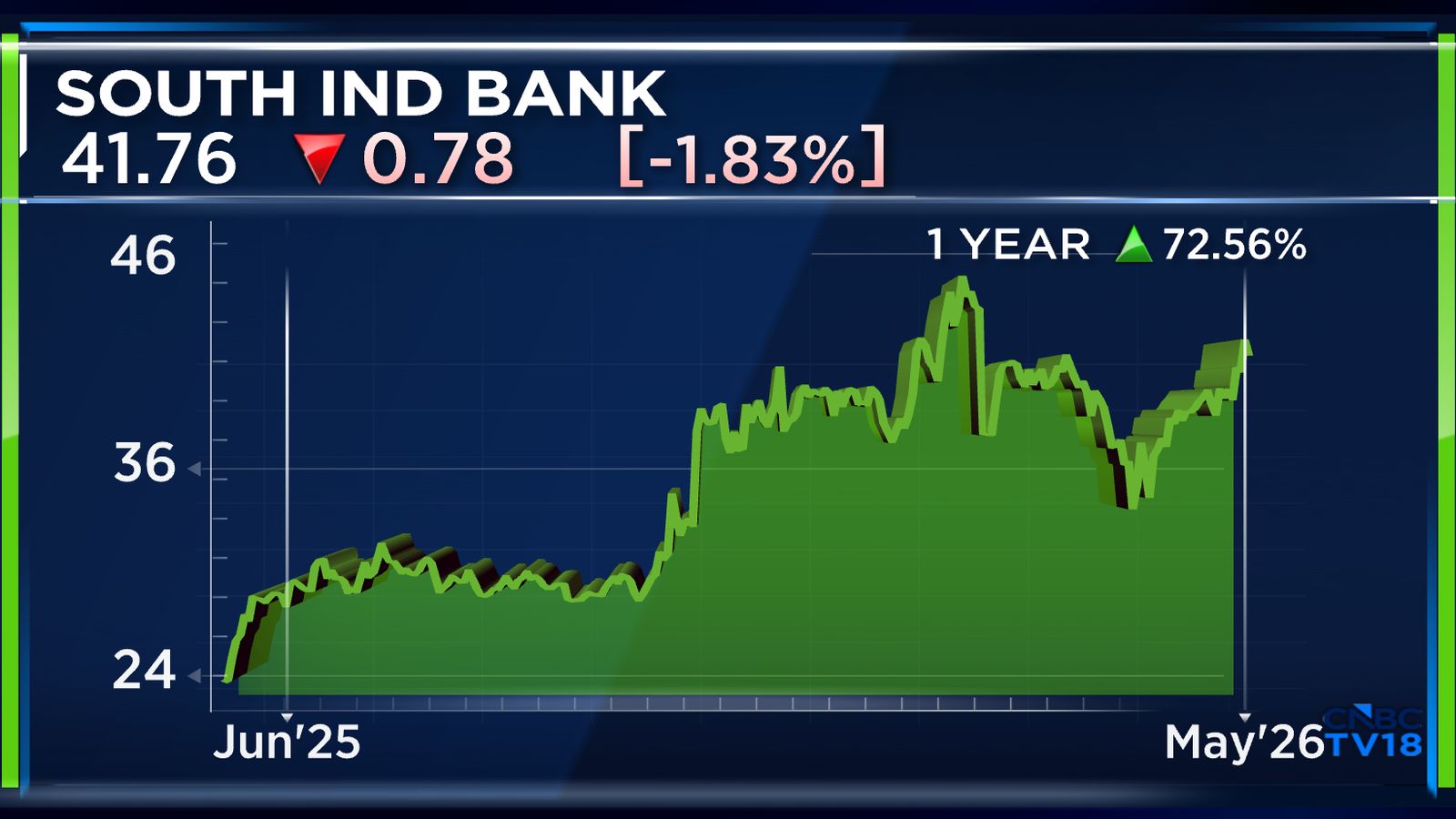

The bank currently has a market capitalisation of ₹10,933.68 crore, while its shares have gained more than 72% over the last year.

This is an edited transcript of the interview.Q: Let's start with the asset quality, which has come as a bigger surprise this quarter. You had record high profits, record high revenues, but asset quality is where the focus has been. What has aided this recovery? Were there one-offs? What’s happening with your legacy book? Since most of the slippages are still coming from there, when do you start to see that normalise? And any guidance you could give us with what's happening in West Asia, if you expect that to start showing up in the book, what kind of provisions you're making for it? A: We've been working on asset quality for the last five years, and the impact of that is now beginning to show through. Even in the last quarter, we had taken a large charge, and we took a significant technical write-off at the end of March as well, which helped the gross numbers to come down very considerably.

The slippages for us are at historical lows. So, for the quarter, our slippage was only 15 basis points. The prior quarter was at 16 basis points. So, on an annualised basis, we are losing approximately 60 basis points or thereabouts, and recoveries have been very strong. So, our recoveries are trending at approximately ₹400 crore against non-performing asset (NPA) slippage of approximately ₹150 crore. And that has helped us get to a point where our net NPA number is approximately 29 basis points. And this has happened over a period of time. It's not happened this quarter. It is a great deal of work that's gone into ensuring that the underwriting standards have been fixed, and we do our best in trying to get the kind of quality of customers that we actually want to onboard onto our books.

For the full interview, watch the accompanying videoQ: Any number you could give us for the credit cost guidance? And let me also just extend that to ask what your exposure towards West Asia is. And with the government now announcing this ECLGS 5.0, are there any of your customers that have reached out to you that could potentially utilise this line? Do you have exposure to any of the airlines as well? And to just complete that thread as well, NRI flows, that's been growing at 12 to 14% odd for you. Any sort of slowdown on account of what's happening there?A: Let me try and answer the last one first. NRI flows continue to be strong, and our expectation is, as long as the crisis continues, we think that flows will be strong because there will be a flow of capital to safe haven entities such as India. And consequently, we do expect that these flows will continue to be strong.

With respect to the other questions that you asked, our credit costs for the quarter were at three basis points, and that's an extraordinarily small number. We don't expect these to remain at these levels. We do believe that credit costs will increase as time goes by. We do think that the West Asia crisis will have an overall negative impact on portfolio performance. How much and what quantum it is, is something that only time will tell. We don't have any direct exposure with respect to airlines and other such entities that are immediately impacted. We do have some exposure to petroleum refiners and so on and so forth, but they're largely government-owned, and the expectation is that there won't be a very significant impact on them.

Also Read | RailTel expects ₹300 crore data centre revenue in FY27

But estimating first-order impact and thereafter second- and third-order impacts is very difficult, because petroleum and energy are intrinsic to so many industries. So, we are watching this very closely. As of this moment, we don't have very negative views, nor are we seeing very significant increases in our working capital utilisation levels, but it is something that we watch out for every day. I'm afraid I can't give you a better answer than that, but that is the situation as of this moment.

Q: What you can tell us is if there is any proactive provision that you have made, or are looking to make, in anticipation of any negative impact that you see from this West Asia crisis. Part one. And two is that you've seen a significant improvement in asset quality. Yes, there have been significant recoveries as well that you have seen this quarter, but a majority of your gross NPAs are still coming from your old legacy book. By what point does that become irrelevant? And do you anticipate this recovery trend to continue in FY27 as well?A: Our legacy book is currently approximately 12% of the total, and our view is that it has now reached a point where perhaps the distinction between the new book and the legacy book is no longer relevant because significant time has elapsed since the classification of these assets as well.

So, whilst historically, a majority of our losses have come from the legacy book, we think that going forward, the performance of the two should sort of normalise and become similar to each other.

The reason why we haven't made any provisions for the West Asia crisis is the fact that it is radically uncertain. It's very hard to figure out how long it's going to last. It's very hard to understand how it is going to impact us as well. Therefore, we're waiting and watching to see what we need to do.

Our provision coverage ratios are very high. Our net NPA number is only approximately ₹280 crore or thereabouts. So, we have a very well-provided.

Portfolio performance - if you were to look at our investor deck, we've given you numbers on SMA-1 as well as SMA-2. Those numbers are at historical lows. At this point in time therefore, to be able to predict possible downsides becomes a little difficult, which is the reason why we are watching the portfolio very closely and trying to understand if we need to do something, which we will do as the quarters roll by.

Also Read | Newgen targets return to double-digit growth in FY27: CEO Virender Jeet

Q: You also said that your credit costs were at historic lows as well, but your margins are still under slight pressure. But now, with the rate cut cycle almost coming to an end, there is significant competition as well in your sector. What steps are you taking to protect these margins that are at sub-3% currently? And of course, do you see them improving in the next year?A: We hit a bottom of 2.8% net interest margin (NIM), which happened at the end of Q2 and from there, we've now gone to 2.95% NIM. So, we grew by nine basis points last quarter. We grew six basis points the quarter prior to that. We think that trend will continue. We hope that in the medium term, we get back to about 3.25% or thereabouts as NIM, which was our norm before the Reserve Bank of India (RBI) rate-cutting cycle impacted us.

Q: We have your outlook on the margins, but let me just move on and quickly address your advances growth as well. It's been pretty strong at 15%, especially gold loans, which saw more than 45% growth. Vehicle and personal loans also saw 21% and 30% kind of growth. But what's been slower has been corporate. You've, of course, been talking about how you're deliberately not really growing too fast in that segment. Do you continue with that strategy? And what guidance could you give us for what FY27 could shape up to be?A: We continue to prioritise retail and MSME over corporate, not because of any other reason other than the fact that spreads on the corporate side have been very narrow. And given our focus on extremely high-quality corporate, the ability to eke out a profit is rather limited. Therefore, we need to sort of balance out the book with personal, agriculture and business loans, and that's what we are doing.

We are looking to bring corporate down to approximately a third of our total book. We continue to think that we should be able to grow at the rate at which the market grows. So, our assets grew at approximately 16% last year. The recorded number in our investor deck will be a little less because of the significant write-off that we did at the end of March. But going forward as well, we think that we should be able to grow as fast as the market. I do understand that the current outlook of the market is that the growth rate will be a little lower than the prior year, but we think that 15% to 16% growth should be reasonable, given the fact that we are a small institution.

Q: Your thoughts on succession planning, given your term is ending in September. Anything you could leave us with?A: It's a question more appropriately put to the board, but the process is on, and I'm sure that we will come out with information for the media very shortly.

Catch all the latest updates from the stock market here

He said slippages and credit costs remained near historical lows, with the bank’s quarterly slippage ratio at 15 basis points. Recoveries were trending at around ₹400 crore against NPA slippages of nearly ₹150 crore, helping net NPA levels decline to nearly 29 basis points.

“We think that 15% to 16% growth should be reasonable,” he said, adding that the lender will continue to prioritise retail and MSME lending over corporate loans.

Seshadri said the bank was closely monitoring the West Asia conflict but had not made any specific provisions yet because the situation remained uncertain.

“We do think that the West Asia crisis will have an overall negative impact on portfolio performance,” he said, while noting that the bank does not have direct exposure to airlines and has limited exposure to government-owned petroleum refiners.

The bank currently has a market capitalisation of ₹10,933.68 crore, while its shares have gained more than 72% over the last year.

This is an edited transcript of the interview.Q: Let's start with the asset quality, which has come as a bigger surprise this quarter. You had record high profits, record high revenues, but asset quality is where the focus has been. What has aided this recovery? Were there one-offs? What’s happening with your legacy book? Since most of the slippages are still coming from there, when do you start to see that normalise? And any guidance you could give us with what's happening in West Asia, if you expect that to start showing up in the book, what kind of provisions you're making for it? A: We've been working on asset quality for the last five years, and the impact of that is now beginning to show through. Even in the last quarter, we had taken a large charge, and we took a significant technical write-off at the end of March as well, which helped the gross numbers to come down very considerably.

The slippages for us are at historical lows. So, for the quarter, our slippage was only 15 basis points. The prior quarter was at 16 basis points. So, on an annualised basis, we are losing approximately 60 basis points or thereabouts, and recoveries have been very strong. So, our recoveries are trending at approximately ₹400 crore against non-performing asset (NPA) slippage of approximately ₹150 crore. And that has helped us get to a point where our net NPA number is approximately 29 basis points. And this has happened over a period of time. It's not happened this quarter. It is a great deal of work that's gone into ensuring that the underwriting standards have been fixed, and we do our best in trying to get the kind of quality of customers that we actually want to onboard onto our books.

For the full interview, watch the accompanying videoQ: Any number you could give us for the credit cost guidance? And let me also just extend that to ask what your exposure towards West Asia is. And with the government now announcing this ECLGS 5.0, are there any of your customers that have reached out to you that could potentially utilise this line? Do you have exposure to any of the airlines as well? And to just complete that thread as well, NRI flows, that's been growing at 12 to 14% odd for you. Any sort of slowdown on account of what's happening there?A: Let me try and answer the last one first. NRI flows continue to be strong, and our expectation is, as long as the crisis continues, we think that flows will be strong because there will be a flow of capital to safe haven entities such as India. And consequently, we do expect that these flows will continue to be strong.

With respect to the other questions that you asked, our credit costs for the quarter were at three basis points, and that's an extraordinarily small number. We don't expect these to remain at these levels. We do believe that credit costs will increase as time goes by. We do think that the West Asia crisis will have an overall negative impact on portfolio performance. How much and what quantum it is, is something that only time will tell. We don't have any direct exposure with respect to airlines and other such entities that are immediately impacted. We do have some exposure to petroleum refiners and so on and so forth, but they're largely government-owned, and the expectation is that there won't be a very significant impact on them.

Also Read | RailTel expects ₹300 crore data centre revenue in FY27

But estimating first-order impact and thereafter second- and third-order impacts is very difficult, because petroleum and energy are intrinsic to so many industries. So, we are watching this very closely. As of this moment, we don't have very negative views, nor are we seeing very significant increases in our working capital utilisation levels, but it is something that we watch out for every day. I'm afraid I can't give you a better answer than that, but that is the situation as of this moment.

Q: What you can tell us is if there is any proactive provision that you have made, or are looking to make, in anticipation of any negative impact that you see from this West Asia crisis. Part one. And two is that you've seen a significant improvement in asset quality. Yes, there have been significant recoveries as well that you have seen this quarter, but a majority of your gross NPAs are still coming from your old legacy book. By what point does that become irrelevant? And do you anticipate this recovery trend to continue in FY27 as well?A: Our legacy book is currently approximately 12% of the total, and our view is that it has now reached a point where perhaps the distinction between the new book and the legacy book is no longer relevant because significant time has elapsed since the classification of these assets as well.

So, whilst historically, a majority of our losses have come from the legacy book, we think that going forward, the performance of the two should sort of normalise and become similar to each other.

The reason why we haven't made any provisions for the West Asia crisis is the fact that it is radically uncertain. It's very hard to figure out how long it's going to last. It's very hard to understand how it is going to impact us as well. Therefore, we're waiting and watching to see what we need to do.

Our provision coverage ratios are very high. Our net NPA number is only approximately ₹280 crore or thereabouts. So, we have a very well-provided.

Portfolio performance - if you were to look at our investor deck, we've given you numbers on SMA-1 as well as SMA-2. Those numbers are at historical lows. At this point in time therefore, to be able to predict possible downsides becomes a little difficult, which is the reason why we are watching the portfolio very closely and trying to understand if we need to do something, which we will do as the quarters roll by.

Also Read | Newgen targets return to double-digit growth in FY27: CEO Virender Jeet

Q: You also said that your credit costs were at historic lows as well, but your margins are still under slight pressure. But now, with the rate cut cycle almost coming to an end, there is significant competition as well in your sector. What steps are you taking to protect these margins that are at sub-3% currently? And of course, do you see them improving in the next year?A: We hit a bottom of 2.8% net interest margin (NIM), which happened at the end of Q2 and from there, we've now gone to 2.95% NIM. So, we grew by nine basis points last quarter. We grew six basis points the quarter prior to that. We think that trend will continue. We hope that in the medium term, we get back to about 3.25% or thereabouts as NIM, which was our norm before the Reserve Bank of India (RBI) rate-cutting cycle impacted us.

Q: We have your outlook on the margins, but let me just move on and quickly address your advances growth as well. It's been pretty strong at 15%, especially gold loans, which saw more than 45% growth. Vehicle and personal loans also saw 21% and 30% kind of growth. But what's been slower has been corporate. You've, of course, been talking about how you're deliberately not really growing too fast in that segment. Do you continue with that strategy? And what guidance could you give us for what FY27 could shape up to be?A: We continue to prioritise retail and MSME over corporate, not because of any other reason other than the fact that spreads on the corporate side have been very narrow. And given our focus on extremely high-quality corporate, the ability to eke out a profit is rather limited. Therefore, we need to sort of balance out the book with personal, agriculture and business loans, and that's what we are doing.

We are looking to bring corporate down to approximately a third of our total book. We continue to think that we should be able to grow at the rate at which the market grows. So, our assets grew at approximately 16% last year. The recorded number in our investor deck will be a little less because of the significant write-off that we did at the end of March. But going forward as well, we think that we should be able to grow as fast as the market. I do understand that the current outlook of the market is that the growth rate will be a little lower than the prior year, but we think that 15% to 16% growth should be reasonable, given the fact that we are a small institution.

Q: Your thoughts on succession planning, given your term is ending in September. Anything you could leave us with?A: It's a question more appropriately put to the board, but the process is on, and I'm sure that we will come out with information for the media very shortly.

Catch all the latest updates from the stock market here

/images/ppid_59c68470-image-177821252934048334.webp)

/images/ppid_59c68470-image-177821502795332365.webp)

/images/ppid_59c68470-image-177812753082616344.webp)

/images/ppid_59c68470-image-17781475290998703.webp)

/images/ppid_59c68470-image-177821513442065866.webp)

/images/ppid_59c68470-image-177804007888288228.webp)