/images/ppid_59c68470-image-177986517703646564.webp)

What is the story about?

Candace Browning, Head-Global Research at Bank of America, believes India has emerged as one of the near-term losers from the Iran conflict because of its dependence on imported energy, but a fall in oil prices could help India regain foreign investor interest.

"The losers of recent months could become the winners by the end of the year. We remain quite sanguine on the Indian market over the long term," she said.

Browning says global investors are largely looking through the geopolitical risks surrounding Iran, betting that the Strait of Hormuz disruption will remain temporary and oil prices will ease by the end of the year.

She says markets continue to stay focused on the ongoing artificial intelligence (AI) infrastructure investment cycle, which is still driving strong corporate earnings growth in the US.

This is an edited transcript of the interview.Q: Markets seem surprisingly resilient despite rising geopolitical uncertainty around the US-Iran situation. Do you think investors are underestimating the macro risk from a prolonged energy shock, or is the market betting this remains contained? What's your view?

This is an edited transcript of the interview.Q: Markets seem surprisingly resilient despite rising geopolitical uncertainty around the US-Iran situation. Do you think investors are underestimating the macro risk from a prolonged energy shock, or is the market betting this remains contained? What's your view?

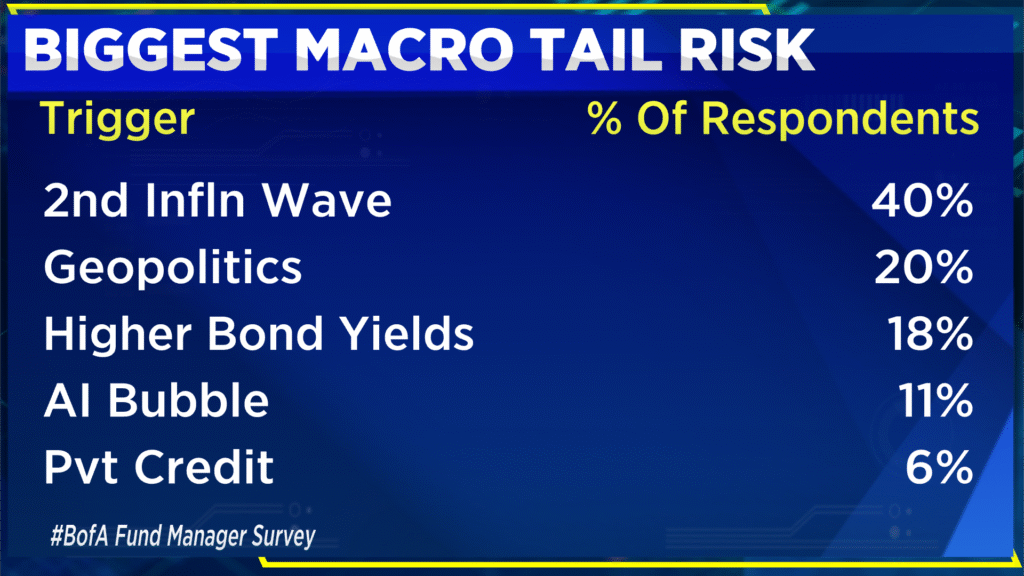

A: We just finished a global fund manager survey covering more than 200 institutions managing over $500 billion in assets. The results were quite interesting. About 54% of respondents expect the Strait of Hormuz to be fully open by the end of June. Investors are effectively looking through the problems around the Strait and believe oil prices will probably decline and end the year around $85.

Whether that is optimistic or too optimistic, we will find out. But this clearly shows investors are looking through the issue. Rather than focusing on the Iran war, markets are focusing on the continuing proliferation of capex around AI infrastructure. There has been a trade-off between those two themes.

Also Read | Foreign investor selling now a bigger drag on rupee: Jefferies

Q: One of the biggest debates globally right now is whether we are entering a stagflationary phase, which means high oil prices, sticky inflation and slowing growth. How seriously is BofA thinking about that risk, especially for the US and global economy?

A: It is definitely a risk. What has happened with the Iran situation is what I would call a stagflation shock. We now have a somewhat different outlook on interest rates compared with the beginning of the year.

We definitely think there is more of a tilt towards tightening monetary conditions rather than the looser conditions that existed earlier. However, it is still a little too early to call for rate hikes in the US. While we are concerned about slower growth and higher inflation, we do not think there will be Fed hikes this year.

We do expect around 50 basis points of hikes in Europe.

Q: From an asset allocation perspective, capital continues moving towards US equities, particularly AI trades. Will that continue, or are you beginning to see rotation into commodities, emerging markets and real assets?

Q: From an asset allocation perspective, capital continues moving towards US equities, particularly AI trades. Will that continue, or are you beginning to see rotation into commodities, emerging markets and real assets?

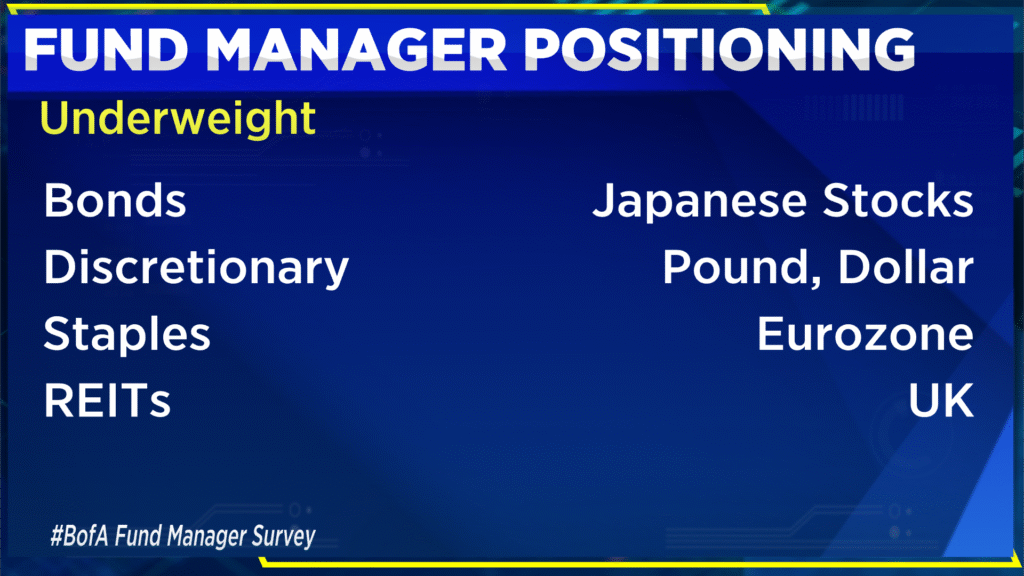

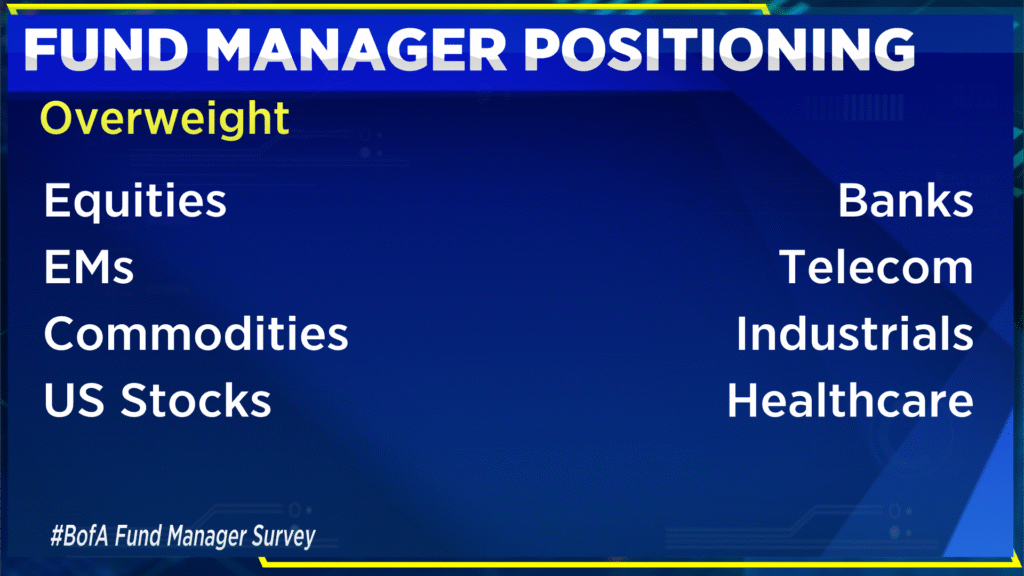

A: We remain quite bullish on the US, assuming the Iran situation gets resolved over the next couple of weeks. While we see long-term opportunities in frontier and emerging markets, we do not think those opportunities will be realised until the Iran situation is resolved.

India, for example, is highly dependent on imported energy. We continue to believe this energy problem will hurt some emerging and frontier markets. In contrast, while the US is seeing higher gas prices, it is still benefiting from the AI boom.

You can clearly see that in corporate earnings. The most recent quarter saw strong double-digit earnings growth, and earnings growth for companies in the S&P 500 continues to remain extremely robust.

Q: Almost every major market rally globally seems tied to AI. Are we still early in this cycle, or is it becoming excessive? What makes this AI cycle different from past tech booms?

A: If you look back at the early internet era, many companies then were completely unprofitable. A lot of these companies today are actually very profitable.

Also Read | West Asia easing and AI trade cooling could revive India interest: Allspring’s Paroda

You can look at current AI capex spending and say it is a lot of money that is not generating much revenue yet. But the reality is that this investment is likely to continue for another 12 to 18 months, and we feel strongly about that.

The jury is still out on the eventual revenue-generating capability of these technologies. So, it is too early to call this frothy or a bubble.

Q: What about India? Foreign investors have pulled out nearly $22 billion from Indian equities this year. Is this purely money rotating towards Taiwan and Korea to chase the AI premium, or is this a structural shift?

A: India has been particularly hurt because of its dependence on imported energy. Any policy changes related to improving energy security would really benefit India.

India has been one of the losers from the Iran war so far in terms of equity valuations. But if the war ends and oil prices decline, India still has strong structural advantages behind it.

The losers of recent months could become the winners by the end of the year. We remain quite sanguine on the Indian market over the long term. We believe these issues are relatively short-term.

Q: Will the war ending and oil prices cooling alone fix the foreign outflow problem in India, or what else is needed for FIIs to return?

A: It will not completely fix the problem, but it would have a very large impact.

Watch the full conversation here

India has a lot going for it in terms of demographics. Positive policy changes and continued deregulation would also be very beneficial.

Catch all the latest updates from the stock market here

"The losers of recent months could become the winners by the end of the year. We remain quite sanguine on the Indian market over the long term," she said.

Browning says global investors are largely looking through the geopolitical risks surrounding Iran, betting that the Strait of Hormuz disruption will remain temporary and oil prices will ease by the end of the year.

She says markets continue to stay focused on the ongoing artificial intelligence (AI) infrastructure investment cycle, which is still driving strong corporate earnings growth in the US.

This is an edited transcript of the interview.Q: Markets seem surprisingly resilient despite rising geopolitical uncertainty around the US-Iran situation. Do you think investors are underestimating the macro risk from a prolonged energy shock, or is the market betting this remains contained? What's your view?

A: We just finished a global fund manager survey covering more than 200 institutions managing over $500 billion in assets. The results were quite interesting. About 54% of respondents expect the Strait of Hormuz to be fully open by the end of June. Investors are effectively looking through the problems around the Strait and believe oil prices will probably decline and end the year around $85.

Whether that is optimistic or too optimistic, we will find out. But this clearly shows investors are looking through the issue. Rather than focusing on the Iran war, markets are focusing on the continuing proliferation of capex around AI infrastructure. There has been a trade-off between those two themes.

Also Read | Foreign investor selling now a bigger drag on rupee: Jefferies

Q: One of the biggest debates globally right now is whether we are entering a stagflationary phase, which means high oil prices, sticky inflation and slowing growth. How seriously is BofA thinking about that risk, especially for the US and global economy?

A: It is definitely a risk. What has happened with the Iran situation is what I would call a stagflation shock. We now have a somewhat different outlook on interest rates compared with the beginning of the year.

We definitely think there is more of a tilt towards tightening monetary conditions rather than the looser conditions that existed earlier. However, it is still a little too early to call for rate hikes in the US. While we are concerned about slower growth and higher inflation, we do not think there will be Fed hikes this year.

We do expect around 50 basis points of hikes in Europe.

Q: From an asset allocation perspective, capital continues moving towards US equities, particularly AI trades. Will that continue, or are you beginning to see rotation into commodities, emerging markets and real assets?

A: We remain quite bullish on the US, assuming the Iran situation gets resolved over the next couple of weeks. While we see long-term opportunities in frontier and emerging markets, we do not think those opportunities will be realised until the Iran situation is resolved.

India, for example, is highly dependent on imported energy. We continue to believe this energy problem will hurt some emerging and frontier markets. In contrast, while the US is seeing higher gas prices, it is still benefiting from the AI boom.

You can clearly see that in corporate earnings. The most recent quarter saw strong double-digit earnings growth, and earnings growth for companies in the S&P 500 continues to remain extremely robust.

Q: Almost every major market rally globally seems tied to AI. Are we still early in this cycle, or is it becoming excessive? What makes this AI cycle different from past tech booms?

A: If you look back at the early internet era, many companies then were completely unprofitable. A lot of these companies today are actually very profitable.

Also Read | West Asia easing and AI trade cooling could revive India interest: Allspring’s Paroda

You can look at current AI capex spending and say it is a lot of money that is not generating much revenue yet. But the reality is that this investment is likely to continue for another 12 to 18 months, and we feel strongly about that.

The jury is still out on the eventual revenue-generating capability of these technologies. So, it is too early to call this frothy or a bubble.

Q: What about India? Foreign investors have pulled out nearly $22 billion from Indian equities this year. Is this purely money rotating towards Taiwan and Korea to chase the AI premium, or is this a structural shift?

A: India has been particularly hurt because of its dependence on imported energy. Any policy changes related to improving energy security would really benefit India.

India has been one of the losers from the Iran war so far in terms of equity valuations. But if the war ends and oil prices decline, India still has strong structural advantages behind it.

The losers of recent months could become the winners by the end of the year. We remain quite sanguine on the Indian market over the long term. We believe these issues are relatively short-term.

Q: Will the war ending and oil prices cooling alone fix the foreign outflow problem in India, or what else is needed for FIIs to return?

A: It will not completely fix the problem, but it would have a very large impact.

Watch the full conversation here

India has a lot going for it in terms of demographics. Positive policy changes and continued deregulation would also be very beneficial.

Catch all the latest updates from the stock market here

/images/ppid_59c68470-image-177968502759745957.webp)

/images/ppid_59c68470-image-177970006987264248.webp)

/images/ppid_59c68470-image-17798175469957261.webp)

/images/ppid_59c68470-image-177985513348476779.webp)

/images/ppid_59c68470-image-177981253323736959.webp)

/images/ppid_59c68470-image-177981503530738288.webp)

/images/ppid_59c68470-image-177983753154937879.webp)

/images/ppid_59c68470-image-177963753630694206.webp)

/images/ppid_59c68470-image-177961511017179000.webp)