/images/ppid_59c68470-image-177908253499542926.webp)

What is the story about?

Muthoot Finance is seeing strong growth in higher-ticket gold loans even as smaller borrowers exit the system, Managing Director George Alexander Muthoot said. “Consumers are becoming more prosperous,” Muthoot said, adding that growth is now coming from loan buckets above ₹50,000.

Looking ahead, Muthoot Finance plans to open around 300 new branches this year, while subsidiary Belstar Microfinance could add another 200 branches.

He said rising gold prices have reduced the quantity of gold pledged per loan, impacting tonnage growth despite higher AUM expansion.

The company expects competition in the gold loan market to intensify, but Muthoot said the overall opportunity continues to expand as more households monetise idle jewellery. “The pie is increasing,” he said, noting that banks hold over ₹12 lakh crore in gold loans while NBFCs account for ₹3-3.5 lakh crore.

He also said restrictions on gold imports are unlikely to affect gold loan demand because large quantities of household jewellery remain outside the formal lending market.

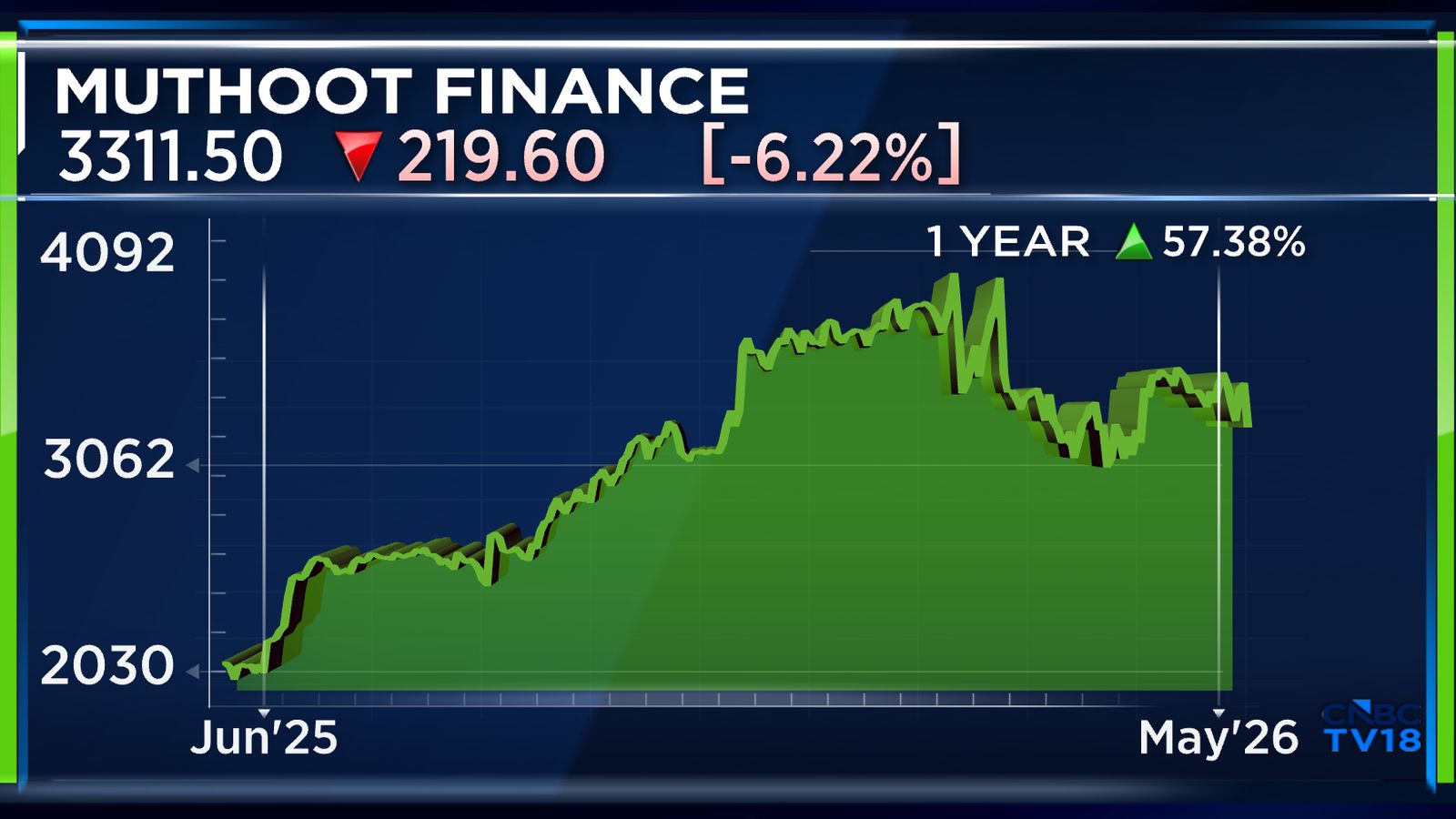

Muthoot Finance currently has a market capitalisation of ₹1,32,924.21 crore, while its shares have risen over 57% in the last year.

These are edited excerpts from the interview.Q: AUM grew 50% on a year-on-year basis. But if you look at the number of active customers, it fell about 2% sequentially, quarter on quarter. So if you look at quarter-on-quarter AUM growth, it is 12%, while active customers are down 2% sequentially. So why don't you start by addressing that?

A: The active customer base has not increased in proportion to the AUM growth, that's your question. So, we also did a little deep dive into how this is happening and why this is happening. We realised that customers below ₹10,000 loans, very small and ultra-small customers, amounting to about five lakh customers, have gone out of the system last year. Among customers between ₹10,000 to ₹30,000, again another six lakh customers went out of the system. But then we see growth in the other buckets, such as ₹50,000-₹1 lakh, etc.

So, for us, our income comes from the loan book and assets, AUM, and that is going up. This is because it's a very old book with old customers. Also, among old customers, there is always a churn. The loan is for only three to four months. So, there is churn in the portfolio every three months. That is why more customers go out and new customers come in.

The same thing applies to tonnage also. If you look at the tonnage, because today we don't need the 10 grams, which we had to give for a ₹1 lakh loan one year back. Today, we need only maybe five grams or six grams for the same loan. So, when a customer comes for the new loan, they give only six grams instead of 10 grams. That is why in the old book we see this.

Also Read | Torrent Power targets up to 1.4 GW renewable capacity addition in FY27 as gas prices rise

Q: So, 11 lakh customers with loans between ₹10,000 to ₹30,000 essentially went out, right?

A: Yes, they went out of the system.

Q: But you're growing in the higher-ticket segment, ₹50,000 plus.

A: Consumers are becoming more prosperous.

Q: Was funding a concern at all, or no?

A: It is always difficult because now, in the last two quarters, we have seen rates going up a little, but there is no concern. Probably it has become a little bit more costly, maybe 50-60 basis points costlier. That is why we also increased our lending rate by 1% in the last three-four months, because we expect the funding cost is going up. The incremental borrowing costs from banks, etc, are not coming down.

Q: You've increased lending rates by 100 basis points?

A: 75 to 100, yes.

Q: Because if you look at the gold price rise, that has been phenomenal. If you look at the fourth quarter, or maybe even a slightly longer period, compared to that, the AUM growth has been a little slower. That's what I was trying to get at. Don't you think higher rates are hurting?

A: Higher rates, yes, but that's only the yield. I will say the higher rates are because of the gold price, etc. Today, if you look at our portfolio, the average LTV is only 58%. So, people have not borrowed the full money which is eligible for them. They still have left money on the table. So, they can even borrow more if they want. They will borrow only what they require. Just because the gold price has gone up, people don't come and borrow more. As the gold price is going up very high, probably they look at selling it.

Q: Looking at various brokerage notes, some of them are highlighting competition. In fact, an Ambit note says that there are multiple trends indicating high competition. Now the problem is there is additional supply of gold loans coming from players who potentially have lower cost of funds. They're also offering lower yields as well. And basically, for your product, gold loans, there is no big product differentiation. So how will you manage growth? Or is it something that you're looking at, to maybe temper down your yields a little bit, because some competitors are coming with gold loans at 13%, 14%, 15%, 16%, 17% as well? So, a key point with regard to competition, because that's where the Street is a little bit jittery.

A: We have been facing competition from banks over the last several decades. All the banks lend at very low rates. Some do at ultra-low rates, probably for agricultural loans and similar priority loans, etc. So, it is nothing new to us.

Q: But the competition has become a little more intense. You have another gold finance company as well that's come in there with a little bit more funding. A lot of these banks that we speak to also want to eat part of the same pie.

A: It is not part of the same pie. The pie is increasing. Today the total gold loans of banks are more than ₹12 lakh crore. The banks have a portfolio of ₹12 lakh crore, and the non-banking financial companies (NBFCs) have a portfolio of only ₹3 to ₹3.5 lakh crore. So, the business is going up. The demand is going up. More and more people are now monetising their gold, so the base is increasing. It is not that somebody is taking away our share, or we are taking away someone else's share. There is space for everybody.

People look at trust also. Just because of the trust and the reach, etc, which we have, people definitely look at that also. That is why we have been able to survive. So just because we are putting down our rates, it's not that more people are going to come, or because our rates are not competitive with one or two players, it doesn't mean that all the customers will go there. If that was so, then only State Bank of India (SBI), with the lowest cost, would have got all the loans in the country. That is not the case.

Q: But in terms of branch openings, you've guided for some number, 200 to 300. There is some commentary that maybe others are a lot more aggressive with regard to branch openings.

A: We have been opening 200-150 branches every year. Probably now the advantage is we don't need to go and get prior approval. We can open the branch and maybe get it ratified later, or maybe tell them that the branch is there. This year, we are planning to open about 300 branches in Muthoot Finance, maybe another 200 branches in Belstar Microfinance also.

Also Read | JSW Steel CEO sees stable prices, better margins as domestic demand stays strong

Q: Your net interest margins improved and they stand at 13.38%, but you have flagged higher borrowing costs. So, is this peak margins? What would be sustainable NIMs? Or will you look to take another round of increase in yields?

A: It is not that the bank rates are going up. It is stable almost, but then we don't see it coming down. That is what I would like to say. The bank funding rates are not going to come down. We have about 13%, but then maybe 11% to 12% is what, going forward, we should be able to achieve.

Q: And this AUM growth guidance of 15% for next year, is that conservative?

A: It is not conservative. For the last 10 years, we have been doing the same thing. Only in quarter one, we will give 15%. Maybe in quarter two, etc, we start revising it as things progress. So, there is no problem. We see continuing with the same growth also, but just for guidance, we give that 15%.

Q: And the tonnage growth that you've assumed for the coming year?

A: Tonnage growth, I have always been saying, will be dependent on the gold price. If the gold price comes down, the tonnage will go up because new customers come with lesser amount of gold, because they can get the same loan with lesser quantity of gold. I can't insist that they give more gold, because if with 10 grams, he can get ₹1 lakh, why should he give more than 10 grams? So, because the churn is so short, it's a three-month loan or four-month loan, it will be in tandem with the gold price.

Q: These restrictions by the government on gold imports, do you think they will make a difference?

A: No, sir, because today there is about 25,000 to 30,000 tonne of gold jewellery with the public. Today, only 5,000 tonne have come into the gold loan market. There is still a lot of gold lying with people, and we find good opportunities there. This may affect the jewellers, but the jewellery, which is already with the people — it's only the mindset change. The moment people feel that they can monetise the gold, they will bring the gold for loans. Gold loans do not depend on import of gold.

Q: It's the start of a new fiscal. Belstar IPO — you've told us you all don't need the money as of now, but do you think sometime during this year we'll be hearing about the Belstar IPO?

A: Maybe. The board has not thought about it yet. Probably after a year or so, because we are trying to rethink the portfolio also, to do a little more secured lending in that. So, we would like to grow the gold loan portfolio also in that company. We are starting 100 branches there.

For the full interview, watch the accompanying videoQ: By the end of this fiscal?

A: The board has not thought about that, because today they don't need any additional funding.

Catch all the latest updates from the stock market here

Looking ahead, Muthoot Finance plans to open around 300 new branches this year, while subsidiary Belstar Microfinance could add another 200 branches.

He said rising gold prices have reduced the quantity of gold pledged per loan, impacting tonnage growth despite higher AUM expansion.

The company expects competition in the gold loan market to intensify, but Muthoot said the overall opportunity continues to expand as more households monetise idle jewellery. “The pie is increasing,” he said, noting that banks hold over ₹12 lakh crore in gold loans while NBFCs account for ₹3-3.5 lakh crore.

He also said restrictions on gold imports are unlikely to affect gold loan demand because large quantities of household jewellery remain outside the formal lending market.

Muthoot Finance currently has a market capitalisation of ₹1,32,924.21 crore, while its shares have risen over 57% in the last year.

These are edited excerpts from the interview.Q: AUM grew 50% on a year-on-year basis. But if you look at the number of active customers, it fell about 2% sequentially, quarter on quarter. So if you look at quarter-on-quarter AUM growth, it is 12%, while active customers are down 2% sequentially. So why don't you start by addressing that?

A: The active customer base has not increased in proportion to the AUM growth, that's your question. So, we also did a little deep dive into how this is happening and why this is happening. We realised that customers below ₹10,000 loans, very small and ultra-small customers, amounting to about five lakh customers, have gone out of the system last year. Among customers between ₹10,000 to ₹30,000, again another six lakh customers went out of the system. But then we see growth in the other buckets, such as ₹50,000-₹1 lakh, etc.

So, for us, our income comes from the loan book and assets, AUM, and that is going up. This is because it's a very old book with old customers. Also, among old customers, there is always a churn. The loan is for only three to four months. So, there is churn in the portfolio every three months. That is why more customers go out and new customers come in.

The same thing applies to tonnage also. If you look at the tonnage, because today we don't need the 10 grams, which we had to give for a ₹1 lakh loan one year back. Today, we need only maybe five grams or six grams for the same loan. So, when a customer comes for the new loan, they give only six grams instead of 10 grams. That is why in the old book we see this.

Also Read | Torrent Power targets up to 1.4 GW renewable capacity addition in FY27 as gas prices rise

Q: So, 11 lakh customers with loans between ₹10,000 to ₹30,000 essentially went out, right?

A: Yes, they went out of the system.

Q: But you're growing in the higher-ticket segment, ₹50,000 plus.

A: Consumers are becoming more prosperous.

Q: Was funding a concern at all, or no?

A: It is always difficult because now, in the last two quarters, we have seen rates going up a little, but there is no concern. Probably it has become a little bit more costly, maybe 50-60 basis points costlier. That is why we also increased our lending rate by 1% in the last three-four months, because we expect the funding cost is going up. The incremental borrowing costs from banks, etc, are not coming down.

Q: You've increased lending rates by 100 basis points?

A: 75 to 100, yes.

Q: Because if you look at the gold price rise, that has been phenomenal. If you look at the fourth quarter, or maybe even a slightly longer period, compared to that, the AUM growth has been a little slower. That's what I was trying to get at. Don't you think higher rates are hurting?

A: Higher rates, yes, but that's only the yield. I will say the higher rates are because of the gold price, etc. Today, if you look at our portfolio, the average LTV is only 58%. So, people have not borrowed the full money which is eligible for them. They still have left money on the table. So, they can even borrow more if they want. They will borrow only what they require. Just because the gold price has gone up, people don't come and borrow more. As the gold price is going up very high, probably they look at selling it.

Q: Looking at various brokerage notes, some of them are highlighting competition. In fact, an Ambit note says that there are multiple trends indicating high competition. Now the problem is there is additional supply of gold loans coming from players who potentially have lower cost of funds. They're also offering lower yields as well. And basically, for your product, gold loans, there is no big product differentiation. So how will you manage growth? Or is it something that you're looking at, to maybe temper down your yields a little bit, because some competitors are coming with gold loans at 13%, 14%, 15%, 16%, 17% as well? So, a key point with regard to competition, because that's where the Street is a little bit jittery.

A: We have been facing competition from banks over the last several decades. All the banks lend at very low rates. Some do at ultra-low rates, probably for agricultural loans and similar priority loans, etc. So, it is nothing new to us.

Q: But the competition has become a little more intense. You have another gold finance company as well that's come in there with a little bit more funding. A lot of these banks that we speak to also want to eat part of the same pie.

A: It is not part of the same pie. The pie is increasing. Today the total gold loans of banks are more than ₹12 lakh crore. The banks have a portfolio of ₹12 lakh crore, and the non-banking financial companies (NBFCs) have a portfolio of only ₹3 to ₹3.5 lakh crore. So, the business is going up. The demand is going up. More and more people are now monetising their gold, so the base is increasing. It is not that somebody is taking away our share, or we are taking away someone else's share. There is space for everybody.

People look at trust also. Just because of the trust and the reach, etc, which we have, people definitely look at that also. That is why we have been able to survive. So just because we are putting down our rates, it's not that more people are going to come, or because our rates are not competitive with one or two players, it doesn't mean that all the customers will go there. If that was so, then only State Bank of India (SBI), with the lowest cost, would have got all the loans in the country. That is not the case.

Q: But in terms of branch openings, you've guided for some number, 200 to 300. There is some commentary that maybe others are a lot more aggressive with regard to branch openings.

A: We have been opening 200-150 branches every year. Probably now the advantage is we don't need to go and get prior approval. We can open the branch and maybe get it ratified later, or maybe tell them that the branch is there. This year, we are planning to open about 300 branches in Muthoot Finance, maybe another 200 branches in Belstar Microfinance also.

Also Read | JSW Steel CEO sees stable prices, better margins as domestic demand stays strong

Q: Your net interest margins improved and they stand at 13.38%, but you have flagged higher borrowing costs. So, is this peak margins? What would be sustainable NIMs? Or will you look to take another round of increase in yields?

A: It is not that the bank rates are going up. It is stable almost, but then we don't see it coming down. That is what I would like to say. The bank funding rates are not going to come down. We have about 13%, but then maybe 11% to 12% is what, going forward, we should be able to achieve.

Q: And this AUM growth guidance of 15% for next year, is that conservative?

A: It is not conservative. For the last 10 years, we have been doing the same thing. Only in quarter one, we will give 15%. Maybe in quarter two, etc, we start revising it as things progress. So, there is no problem. We see continuing with the same growth also, but just for guidance, we give that 15%.

Q: And the tonnage growth that you've assumed for the coming year?

A: Tonnage growth, I have always been saying, will be dependent on the gold price. If the gold price comes down, the tonnage will go up because new customers come with lesser amount of gold, because they can get the same loan with lesser quantity of gold. I can't insist that they give more gold, because if with 10 grams, he can get ₹1 lakh, why should he give more than 10 grams? So, because the churn is so short, it's a three-month loan or four-month loan, it will be in tandem with the gold price.

Q: These restrictions by the government on gold imports, do you think they will make a difference?

A: No, sir, because today there is about 25,000 to 30,000 tonne of gold jewellery with the public. Today, only 5,000 tonne have come into the gold loan market. There is still a lot of gold lying with people, and we find good opportunities there. This may affect the jewellers, but the jewellery, which is already with the people — it's only the mindset change. The moment people feel that they can monetise the gold, they will bring the gold for loans. Gold loans do not depend on import of gold.

Q: It's the start of a new fiscal. Belstar IPO — you've told us you all don't need the money as of now, but do you think sometime during this year we'll be hearing about the Belstar IPO?

A: Maybe. The board has not thought about it yet. Probably after a year or so, because we are trying to rethink the portfolio also, to do a little more secured lending in that. So, we would like to grow the gold loan portfolio also in that company. We are starting 100 branches there.

For the full interview, watch the accompanying videoQ: By the end of this fiscal?

A: The board has not thought about that, because today they don't need any additional funding.

Catch all the latest updates from the stock market here

/images/ppid_a911dc6a-image-177908152831176407.webp)