/images/ppid_59c68470-image-178358013578588524.webp)

/images/ppid_59c68470-image-178342753206362842.webp)

/images/ppid_59c68470-image-178331255431569511.webp)

/images/ppid_59c68470-image-178330259303631354.webp)

What is the story about?

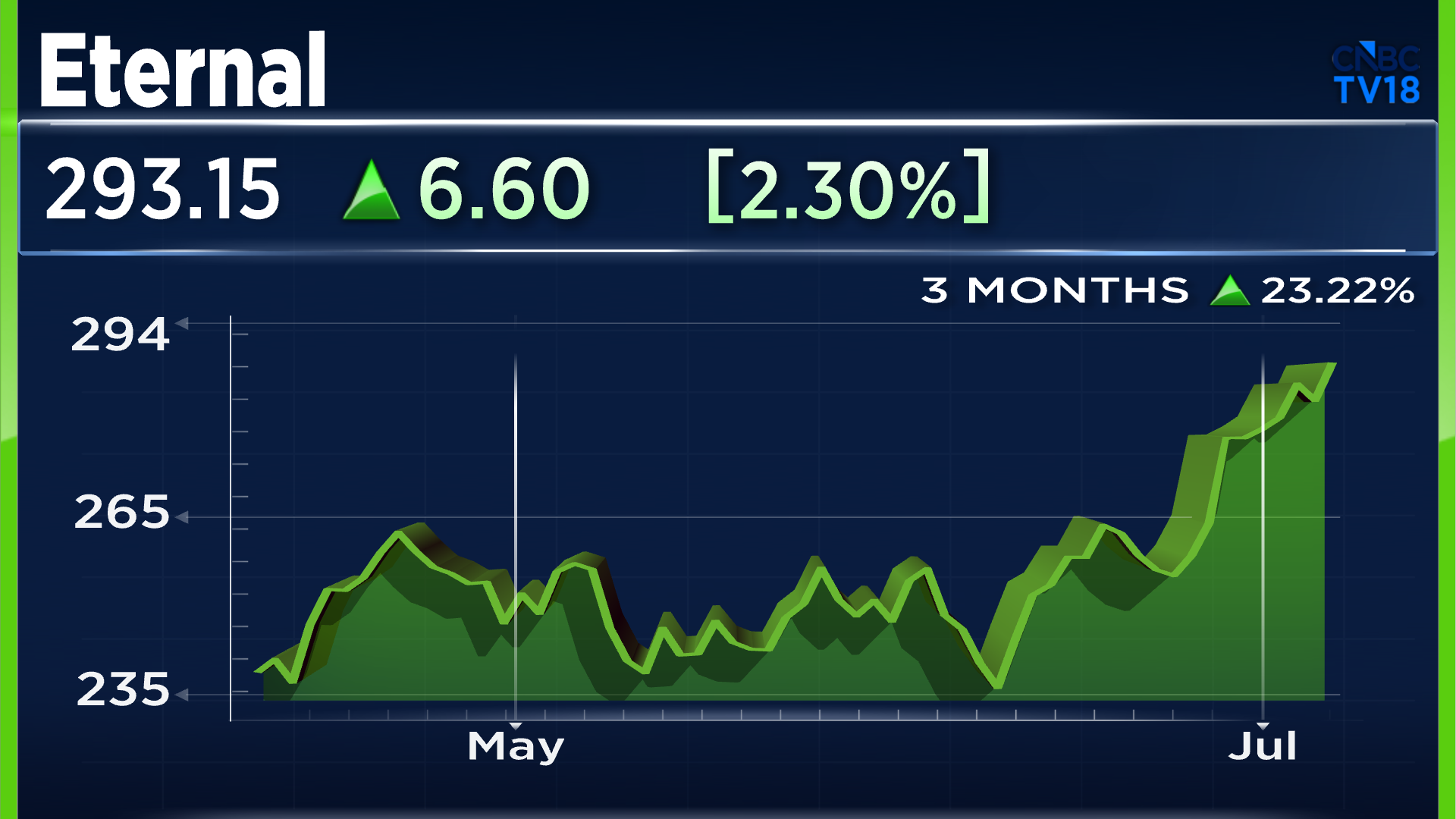

Shares of Eternal

Ltd. gained more than 3% on Thursday, July 9, amid expectations that the stock could see a higher weight in the MSCI Standard Index following an increase in foreign ownership headroom.

At the end of the June quarter (Q1FY27), foreign ownership headroom in Eternal had risen to over 25%, paving the way for a potential increase in the stock's MSCI weight during the index provider's August review.

Analysts estimate that a higher index weight could result in passive inflows of nearly $600 million.

The optimism follows changes to Eternal's foreign ownership structure. After the company was classified as an Indian-Owned and Controlled Company (IOCC), the foreign ownership limit had been reduced from 100% to 49.5%. As a result, MSCI halved the stock's weight during its May 2025 index review.

Separately, brokerage firm Motilal Oswal Financial Services reiterated its 'Buy' rating on Eternal with a target price of ₹380, implying an upside of around 34% from current levels.

The brokerage said it remains constructive on the company's long-term growth prospects, driven by the resilience of its food delivery business and the continued expansion of Blinkit.

According to Motilal Oswal, the food delivery segment has evolved into a stable duopoly alongside Swiggy, supported by balanced market shares, improving profitability and strong customer retention.

The brokerage expects the business to deliver around 20% gross order value (GOV) growth over FY27 and FY28 and has assigned a 35-times EV/EBITDA multiple to the segment.

While growth in the quick commerce business is expected to moderate to around 70% in FY27, the brokerage believes this reflects a normalisation from elevated levels rather than a slowdown.

It expects unit economics to improve steadily, aided by maturing dark stores and operating leverage, resulting in gradual margin expansion.

Motilal Oswal expects Eternal to report profit after tax (PAT) margins of 2.5% in FY27 and 3% in FY28.

The company has guided for $1 billion in adjusted EBITDA at the consolidated level by FY29. Motilal Oswal estimates that around $500 million will come from the quick commerce business, $425 million from food delivery, while the remaining contribution is expected from businesses such as Going Out, District and Hyperpure.

At the end of the June quarter (Q1FY27), foreign ownership headroom in Eternal had risen to over 25%, paving the way for a potential increase in the stock's MSCI weight during the index provider's August review.

Analysts estimate that a higher index weight could result in passive inflows of nearly $600 million.

The optimism follows changes to Eternal's foreign ownership structure. After the company was classified as an Indian-Owned and Controlled Company (IOCC), the foreign ownership limit had been reduced from 100% to 49.5%. As a result, MSCI halved the stock's weight during its May 2025 index review.

Separately, brokerage firm Motilal Oswal Financial Services reiterated its 'Buy' rating on Eternal with a target price of ₹380, implying an upside of around 34% from current levels.

The brokerage said it remains constructive on the company's long-term growth prospects, driven by the resilience of its food delivery business and the continued expansion of Blinkit.

According to Motilal Oswal, the food delivery segment has evolved into a stable duopoly alongside Swiggy, supported by balanced market shares, improving profitability and strong customer retention.

The brokerage expects the business to deliver around 20% gross order value (GOV) growth over FY27 and FY28 and has assigned a 35-times EV/EBITDA multiple to the segment.

While growth in the quick commerce business is expected to moderate to around 70% in FY27, the brokerage believes this reflects a normalisation from elevated levels rather than a slowdown.

It expects unit economics to improve steadily, aided by maturing dark stores and operating leverage, resulting in gradual margin expansion.

Motilal Oswal expects Eternal to report profit after tax (PAT) margins of 2.5% in FY27 and 3% in FY28.

The company has guided for $1 billion in adjusted EBITDA at the consolidated level by FY29. Motilal Oswal estimates that around $500 million will come from the quick commerce business, $425 million from food delivery, while the remaining contribution is expected from businesses such as Going Out, District and Hyperpure.

/images/ppid_59c68470-image-178342002617958809.webp)

/images/ppid_59c68470-image-178340002380090309.webp)

/images/ppid_59c68470-image-178358007768139754.webp)

/images/ppid_59c68470-image-178340256165152644.webp)

/images/ppid_59c68470-image-178343505282395864.webp)

/images/ppid_59c68470-image-178358010672792677.webp)

/images/ppid_59c68470-image-178358016705599588.webp)