/images/ppid_59c68470-image-178063507084265280.webp)

/images/ppid_59c68470-image-178047503738066024.webp)

/images/ppid_59c68470-image-178037753707183343.webp)

/images/ppid_59c68470-image-178037257637641588.webp)

What is the story about?

Neeraj Seth, Founder and CIO of 3R Investment Management, believes the next few months will be a critical test for global markets. While the artificial intelligence (AI) theme remains intact, elevated valuations, leverage build-up and aggressive growth expectations could pressure sentiment.

At the same time, he expects the US private credit market to move through a normal credit cycle, with defaults likely to rise over the next 12–24 months.

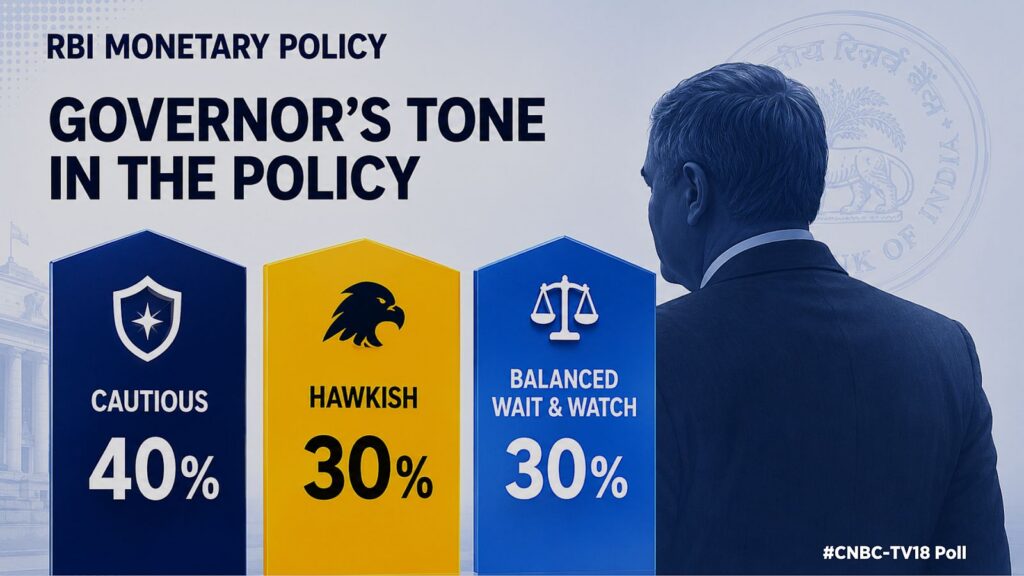

On the domestic front, Seth expects the Reserve Bank of India (RBI) to maintain a hawkish stance and avoid reacting too early by raising rates. He believes higher rates would have a limited impact on the rupee and that policymakers are more likely to focus on measures that ease hedging costs and reduce friction for corporates borrowing in dollars.

This is an edited transcript of the interview.Q: What are your expectations from the RBI this time? We are unlikely to see any tinkering with rates, but could there be measures to prevent further rupee depreciation and curb speculation?

A: I would expect a hawkish hold, which is the right approach. In my view, it is a bit early for the RBI to start reacting. More importantly, I do not think a rate hike would have any significant impact on the currency. The RBI is more likely to look at other measures rather than a rate hike at this point.

Q: What could those other measures be? Would it be relaxing external commercial borrowings (ECB) norms or tighter overseas direct investment (ODI) controls?

Q: What could those other measures be? Would it be relaxing external commercial borrowings (ECB) norms or tighter overseas direct investment (ODI) controls?

A: There could be further relaxation, although the RBI has already eased some ECB norms and those have not been a major constraint on corporates borrowing in dollars. It is more about risk premia, hedging costs and related factors. In my view, the RBI needs to think more about easing the overall environment from a hedging-cost perspective and reducing friction costs for corporates borrowing in dollars.

Q: Markets are also waiting to see whether withholding tax and capital gains tax on government securities are cut. Would that help attract capital? And shouldn't similar steps apply to corporate bonds as well?

A: This has certainly been discussed and has been in the news, although we have not seen anything yet. To be honest, I do not think it would significantly change the direction of capital flows. From a market sentiment perspective, however, it would be a positive and welcome outcome.

Also Read | RBI should avoid aggressive rate hikes as high crude threatens growth, says Axis AMC’s Devang Shah

If I take a step back, I think it is time for the Indian government and regulators to focus on making it easier for foreign institutional investors (FIIs) and foreign direct investment (FDI) capital to come into India over the longer term. This would be a small step, but in the right direction.

Q: The AI trade appears to be getting fragile. Markets such as Korea and Taiwan have seen some pressure. Are we getting closer to the end of the AI trade? Could India, which has been viewed as an anti-AI trade, relatively outperform?

A: Nobody exactly knows where these periods of euphoria end, but there are three things worth highlighting that could put pressure on the pace of the AI trade.

First, when you look at value creation, much of the benefit is still flowing to semiconductors and hardware. The rest of the ecosystem has not yet seen the same gains, and that needs to change.

Second, the pace of valuation expansion and the level of leverage build-up are concerning. I do think there is excessive leverage in parts of the system, which could create pressure. We are seeing sharp moves even at the index level, with markets such as the Kospi moving 5–10% in a single day.

Third, the revenue, sales and margin expectations being priced in by markets are very elevated. Over the last 48 hours, one small disappointment from Broadcom was enough to hit sentiment across the sector.

Overall, when I look at the AI trade alongside upcoming initial public offerings (IPOs) such as SpaceX, Anthropic and OpenAI, as well as Google's announced investment plans, I think market sentiment will be tested over the next couple of months.

Watch the full conversation hereQ: What is your view on the private credit market? Blackstone recently restricted withdrawals from a flagship fund after redemption requests reached 10%. What is your takeaway?

A: Private credit is obviously a very broad term. Some of these issues are specific to the US direct lending market and non-listed BDCs, where distribution has taken place through semi-liquid structures in the wealth channel.

There are two issues at play, and they are often mixed.

The first is fundamentals. I do think private credit in the US is going to go through a credit cycle, and defaults are likely to increase over the next 12–24 months. That is a normal part of the credit cycle.

Also Read | Global AI capex nears $700 billion as investor appetite for tech IPOs stays strong: Citi

The second is headline risk around redemptions. There is a structural issue here. Redemption requests may reach 10%, but many of these vehicles are designed to meet only 5% as per their legal documentation. When all requests are not fulfilled, it creates negative headlines.

In my view, there has been some mis-selling and mis-positioning of this asset class during distribution, and that headline risk is likely to continue.

Catch all the latest updates from the stock market here

At the same time, he expects the US private credit market to move through a normal credit cycle, with defaults likely to rise over the next 12–24 months.

On the domestic front, Seth expects the Reserve Bank of India (RBI) to maintain a hawkish stance and avoid reacting too early by raising rates. He believes higher rates would have a limited impact on the rupee and that policymakers are more likely to focus on measures that ease hedging costs and reduce friction for corporates borrowing in dollars.

This is an edited transcript of the interview.Q: What are your expectations from the RBI this time? We are unlikely to see any tinkering with rates, but could there be measures to prevent further rupee depreciation and curb speculation?

A: I would expect a hawkish hold, which is the right approach. In my view, it is a bit early for the RBI to start reacting. More importantly, I do not think a rate hike would have any significant impact on the currency. The RBI is more likely to look at other measures rather than a rate hike at this point.

Q: What could those other measures be? Would it be relaxing external commercial borrowings (ECB) norms or tighter overseas direct investment (ODI) controls?

A: There could be further relaxation, although the RBI has already eased some ECB norms and those have not been a major constraint on corporates borrowing in dollars. It is more about risk premia, hedging costs and related factors. In my view, the RBI needs to think more about easing the overall environment from a hedging-cost perspective and reducing friction costs for corporates borrowing in dollars.

Q: Markets are also waiting to see whether withholding tax and capital gains tax on government securities are cut. Would that help attract capital? And shouldn't similar steps apply to corporate bonds as well?

A: This has certainly been discussed and has been in the news, although we have not seen anything yet. To be honest, I do not think it would significantly change the direction of capital flows. From a market sentiment perspective, however, it would be a positive and welcome outcome.

Also Read | RBI should avoid aggressive rate hikes as high crude threatens growth, says Axis AMC’s Devang Shah

If I take a step back, I think it is time for the Indian government and regulators to focus on making it easier for foreign institutional investors (FIIs) and foreign direct investment (FDI) capital to come into India over the longer term. This would be a small step, but in the right direction.

Q: The AI trade appears to be getting fragile. Markets such as Korea and Taiwan have seen some pressure. Are we getting closer to the end of the AI trade? Could India, which has been viewed as an anti-AI trade, relatively outperform?

A: Nobody exactly knows where these periods of euphoria end, but there are three things worth highlighting that could put pressure on the pace of the AI trade.

First, when you look at value creation, much of the benefit is still flowing to semiconductors and hardware. The rest of the ecosystem has not yet seen the same gains, and that needs to change.

Second, the pace of valuation expansion and the level of leverage build-up are concerning. I do think there is excessive leverage in parts of the system, which could create pressure. We are seeing sharp moves even at the index level, with markets such as the Kospi moving 5–10% in a single day.

Third, the revenue, sales and margin expectations being priced in by markets are very elevated. Over the last 48 hours, one small disappointment from Broadcom was enough to hit sentiment across the sector.

Overall, when I look at the AI trade alongside upcoming initial public offerings (IPOs) such as SpaceX, Anthropic and OpenAI, as well as Google's announced investment plans, I think market sentiment will be tested over the next couple of months.

Watch the full conversation hereQ: What is your view on the private credit market? Blackstone recently restricted withdrawals from a flagship fund after redemption requests reached 10%. What is your takeaway?

A: Private credit is obviously a very broad term. Some of these issues are specific to the US direct lending market and non-listed BDCs, where distribution has taken place through semi-liquid structures in the wealth channel.

There are two issues at play, and they are often mixed.

The first is fundamentals. I do think private credit in the US is going to go through a credit cycle, and defaults are likely to increase over the next 12–24 months. That is a normal part of the credit cycle.

Also Read | Global AI capex nears $700 billion as investor appetite for tech IPOs stays strong: Citi

The second is headline risk around redemptions. There is a structural issue here. Redemption requests may reach 10%, but many of these vehicles are designed to meet only 5% as per their legal documentation. When all requests are not fulfilled, it creates negative headlines.

In my view, there has been some mis-selling and mis-positioning of this asset class during distribution, and that headline risk is likely to continue.

Catch all the latest updates from the stock market here

/images/ppid_59c68470-image-178046509890397752.webp)

/images/ppid_59c68470-image-178048511894527646.webp)

/images/ppid_59c68470-image-178046007184166996.webp)

/images/ppid_59c68470-image-178055003230120419.webp)

/images/ppid_59c68470-image-178058753215112585.webp)

/images/ppid_59c68470-image-178062755324162969.webp)

/images/ppid_59c68470-image-178056003580685947.webp)

/images/ppid_59c68470-image-178055010443480929.webp)