/images/ppid_59c68470-image-178046761237782932.webp)

/images/ppid_59c68470-image-178038012640950339.webp)

What is the story about?

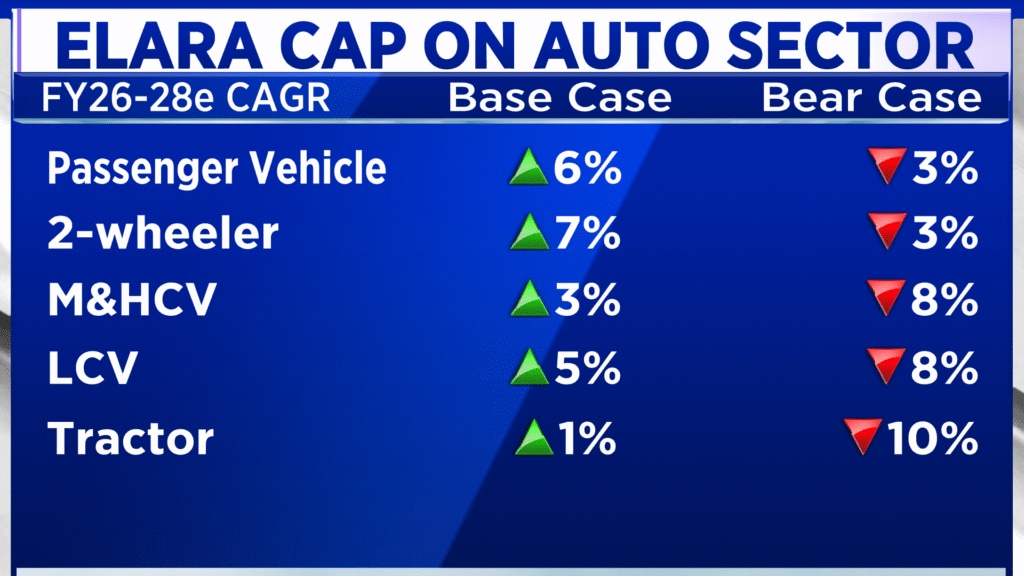

India’s auto sector may see some slowdown after the recent fuel price hikes, but this is unlikely to turn into a sharp downcycle like 2019-20 (FY20), according to Jay Kale, Executive Vice President-Research at Elara Capital.

He believes passenger vehicles (PVs) and two-wheelers remain relatively resilient, even as inflationary pressures begin to affect demand sentiment.

“The key question is whether this is a slowdown or is this the start of a down cycle?” Kale said. “In our view, this is more of a slowdown, not necessarily a start of a down cycle.”

Kale said the current situation is very different from the FY20 slowdown, when rising ownership costs, fuel price increases and the non-banking financial company (NBFC) crisis sharply hit vehicle demand. This time, despite recent price hikes, the overall cost of ownership is still lower than pre-goods and services tax (GST) levels, which gives the industry some cushion.

Elara Capital expects passenger vehicle industry growth of around 6–7% in 2026-27 (FY27), even though several automakers have guided for double-digit growth individually. According to Kale, demand trends were strong until the recent fuel price hikes, with May sales also supported by pre-buying ahead of vehicle price increases.

Also Read | Eicher Motors

Within the sector, Kale prefers passenger vehicles and two-wheelers over commercial vehicles (CVs). He said CV demand is more cyclical and vulnerable to rising diesel prices, which can hurt fleet operator profitability and slow replacement demand.

“PVs and two-wheelers are much more resilient. Historical cycles have shown that PV and two-wheeler cycles are not sharp. CVs are pretty sharp,” he said.

Also Read | TVS Motor Company

Kale added that even in a worst-case scenario, downside risks appear lower for passenger vehicle and two-wheeler stocks compared to CV makers. He believes the risk-reward remains more favourable in these segments.

Electric vehicles (EVs) are also seeing stronger momentum. Kale said EV demand has improved significantly in recent months, with some companies already facing capacity constraints. He added that earlier expectations for EV penetration by 2029-30 (FY30) now appear more realistic given the recent demand trend.

Watch the full conversation here

On stock preferences, Kale’s top picks include Maruti Suzuki, Mahindra and Mahindra , Gabriel India and Minda Corporation (M&M). He said companies expected to gain market share during a slowdown are likely to perform better.

Among auto ancillary companies, he prefers Uno Minda, Sona BLW Precision Forgings, Uno Minda and Sona BLW Precision Forgings.

Catch all the latest updates from the stock market here

He believes passenger vehicles (PVs) and two-wheelers remain relatively resilient, even as inflationary pressures begin to affect demand sentiment.

“The key question is whether this is a slowdown or is this the start of a down cycle?” Kale said. “In our view, this is more of a slowdown, not necessarily a start of a down cycle.”

Kale said the current situation is very different from the FY20 slowdown, when rising ownership costs, fuel price increases and the non-banking financial company (NBFC) crisis sharply hit vehicle demand. This time, despite recent price hikes, the overall cost of ownership is still lower than pre-goods and services tax (GST) levels, which gives the industry some cushion.

Elara Capital expects passenger vehicle industry growth of around 6–7% in 2026-27 (FY27), even though several automakers have guided for double-digit growth individually. According to Kale, demand trends were strong until the recent fuel price hikes, with May sales also supported by pre-buying ahead of vehicle price increases.

Also Read | Eicher Motors

Within the sector, Kale prefers passenger vehicles and two-wheelers over commercial vehicles (CVs). He said CV demand is more cyclical and vulnerable to rising diesel prices, which can hurt fleet operator profitability and slow replacement demand.

“PVs and two-wheelers are much more resilient. Historical cycles have shown that PV and two-wheeler cycles are not sharp. CVs are pretty sharp,” he said.

Also Read | TVS Motor Company

Kale added that even in a worst-case scenario, downside risks appear lower for passenger vehicle and two-wheeler stocks compared to CV makers. He believes the risk-reward remains more favourable in these segments.

Electric vehicles (EVs) are also seeing stronger momentum. Kale said EV demand has improved significantly in recent months, with some companies already facing capacity constraints. He added that earlier expectations for EV penetration by 2029-30 (FY30) now appear more realistic given the recent demand trend.

Watch the full conversation here

On stock preferences, Kale’s top picks include Maruti Suzuki, Mahindra and Mahindra , Gabriel India and Minda Corporation (M&M). He said companies expected to gain market share during a slowdown are likely to perform better.

Among auto ancillary companies, he prefers Uno Minda, Sona BLW Precision Forgings, Uno Minda and Sona BLW Precision Forgings.

Catch all the latest updates from the stock market here

/images/ppid_59c68470-image-178063003444852238.webp)

/images/ppid_59c68470-image-178063510221554304.webp)