/images/ppid_59c68470-image-178098261121930712.webp)

What is the story about?

While India has lagged some global markets, Conrad Saldanha, MD & Portfolio Manager at Neuberger Berman, believes the biggest headwind remains the powerful earnings growth being generated by artificial intelligence (AI) linked sectors in the US, Korea and Taiwan.

With AI spending still robust and hyperscaler capex yet to face meaningful scrutiny, he expects the earnings trajectory in those markets to remain strong for the next few quarters, continuing to attract global and retail flows.

Despite foreign investors reducing exposure to some Indian large-cap names, Saldanha sees selective opportunities in sectors benefiting from the AI infrastructure buildout, particularly power and related infrastructure. He is also constructive on long-term themes in infrastructure and speciality pharma, where innovation, strong demand and global revenue opportunities could support future growth.

This is an edited transcript of the interview.Q: The global sentiment, one day up, one day down on the AI stocks, though the macro trend is largely in their favour. Do you think that is one of the biggest factors because of which India is underperforming right now, and if yes, at what point does that come undone?

A: I think it's been going on for a while. When you look at earnings, they have been outstanding. Think of the US more broadly and the spillover impacts of that. You are seeing 25% growth for the US in terms of earnings. That's among the strongest it's been for a long period of time, so that's the first factor.

Second, when you look at markets like Korea and Taiwan, which are much more geared to the hardware, AI components and inputs, earnings growth has been extraordinary. In Korea, certain stocks could be seeing 150%-plus earnings growth. Memory names in particular, like Samsung or Hynix, are talking about 300% type earnings growth and still trading at six times earnings.

Now, I know these are cyclical stocks, so you have to worry about when you run into peak earnings. But AI spending is still strong. Until you see hyperscaler capex start to be questioned, that is when I think the slowdown happens, and multiples start to correct.

Short-term rates potentially going up could also cause some multiple compression. Arguably, there is evidence that it's overbought. It's probably in the 95th percentile in terms of buying interest and ownership in these stocks.

Also Read | InterGlobe Aviation

But the earnings trajectory is still very strong and is likely to continue for a few quarters. That is the headwind for India in essence. You have seen those flows, plus retail flows, gravitating toward AI, not just in the US, but also in Korea and Taiwan.

Q: What has been keeping you busy in India? Because there are pockets where stocks are doing very well, unaffected by the negative sentiment and external factors. These are largely, though not entirely, non-foreign institutional investor (FII) stocks.

A: I think you are right. Foreigners are pulling out, and maybe they were too long a handful of names, the mega-caps. So, you have seen the brunt of the selling pressure there.

Partly because emerging markets, to a certain degree, saw outflows until more recently, with the AI trend picking up and inflows finally coming back in.

By and large, the space that has done well, including some of what we own, is power. It's energy in a sense, but specifically power plays that feed into AI.

You don't have many direct AI infrastructure plays in India. We own NetWeb. It's been a phenomenal performer. Multiples can be questioned, and there is a scarcity value in the Indian context.

But broadly, infrastructure plays like power has done well, and I continue to see that as a global phenomenon.

I have met a few North Asian and US companies, and the roadmap continues to be very strong in terms of demand. Even transformer companies from Korea to China continue to see massive backlogs. Lead times remain extended.

All of those points point to good pricing, strong demand and healthy order books.

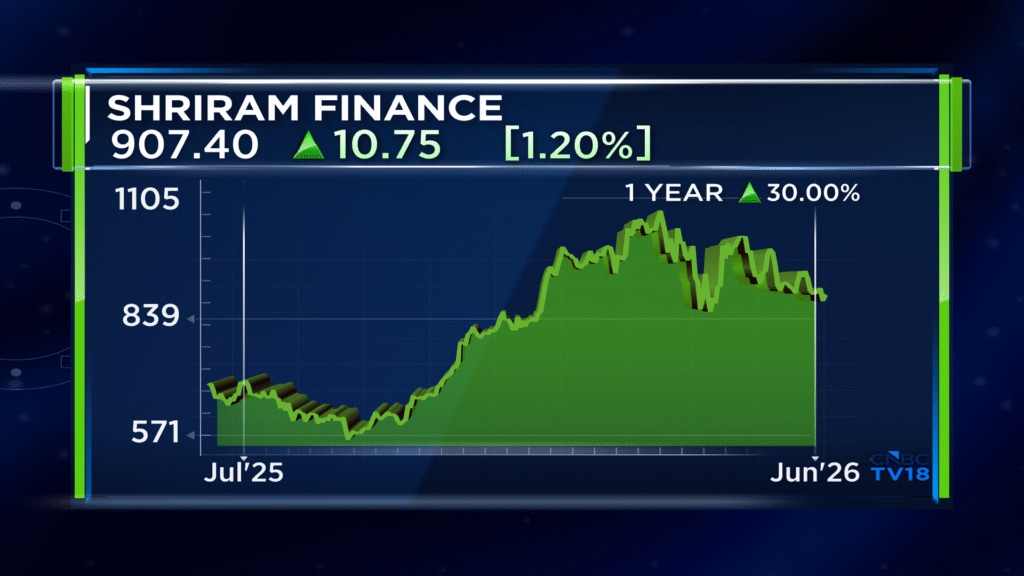

Q: What about India as an investment theme? You had trimmed your exposure to India from around 14-15% to roughly 10%. What are you doing right now? Is there a reason to increase allocation, or are you still cautious? Also, have there been any recent changes in stocks like Shriram Finance or GMR?

A: Not a whole bunch of changes. We are pretty static. We want to see the earnings inflexion. Last time, I mentioned we were starting to warm up to GMR Airports. I think that is a good business. What you are seeing with the infusion of capital from the Japanese is helping not only capital levels but also the cost of capital through credit rating improvements.

Now the question is whether oil prices and near-term concerns around vehicle financing make investors a little more cautious.

On Glenmark Pharmaceuticals, it's interesting because the management team is actually in New York this week. It's a good business. Obviously, you've seen pressure from developments in West Asia, some flight cancellations and potentially some charges being reduced to help alleviate industry pressure.

But it's a great business model and a strong infrastructure asset. It has massive operating leverage, and they run the three principal airports extremely well.

To me, that's a nice Indian consumer proxy backed by hard assets. It's a name we like over the long term. The question is valuation and entry price. You have to pick your points carefully, but it's a good business.

Beyond that, there hasn't been much change.

I would say I am looking again at the pharma space. I have spent a lot of time with Chinese companies and also met Indian companies.

Anthem Biosciences has done some innovative things. I am focusing much more on the innovation and speciality side, where I think there are good prospects and strong dollar-earning opportunities.

Anthem Biosciences is another example. We have owned it since the initial public offering (IPO). It's a good business. They are looking at peptides and semaglutide-related opportunities. That's another area of growth, leaving aside what Chinese companies are doing and exporting in that space.

So, I do think there are opportunities there as well.

Q: You want to give us your take on SpaceX, and what kind of feedback have you got from where you're sitting?

A: It's a fascinating business. You have got to open the roadshow and even the prospectus. It's a brilliant business.

Also Read | Why RBI kept interest rates unchanged despite rising inflation risks

When you look at the three verticals, people get excited. Leave aside the launches, which are obviously the more glamorous part. Starlink itself is a significant opportunity with around 10 million subscribers and considerable room to scale.

Launches are going well. It's a good business.

You have also got the drag from the xAI side and the massive capex that goes into it.

It's attracted a lot of retail interest. It's a big deal. It's a fixed-price IPO at a $1.75 trillion valuation. There are probably a few others not far behind, looking to come to market.

Watch the full conversation here

We will have to see what market absorption looks like. We haven't seen IPOs of this scale before, but there is a fair amount of enthusiasm.

It's extremely unique. You are probably asking the wrong person to evaluate it, but people have made a lot of money from it.

Execution has been exceptional. If you look at the data centre buildout, they have put together this entire infrastructure in literally no time. So, overall, it's a great execution.

Catch all the latest updates from the stock market here

With AI spending still robust and hyperscaler capex yet to face meaningful scrutiny, he expects the earnings trajectory in those markets to remain strong for the next few quarters, continuing to attract global and retail flows.

Despite foreign investors reducing exposure to some Indian large-cap names, Saldanha sees selective opportunities in sectors benefiting from the AI infrastructure buildout, particularly power and related infrastructure. He is also constructive on long-term themes in infrastructure and speciality pharma, where innovation, strong demand and global revenue opportunities could support future growth.

This is an edited transcript of the interview.Q: The global sentiment, one day up, one day down on the AI stocks, though the macro trend is largely in their favour. Do you think that is one of the biggest factors because of which India is underperforming right now, and if yes, at what point does that come undone?

A: I think it's been going on for a while. When you look at earnings, they have been outstanding. Think of the US more broadly and the spillover impacts of that. You are seeing 25% growth for the US in terms of earnings. That's among the strongest it's been for a long period of time, so that's the first factor.

Second, when you look at markets like Korea and Taiwan, which are much more geared to the hardware, AI components and inputs, earnings growth has been extraordinary. In Korea, certain stocks could be seeing 150%-plus earnings growth. Memory names in particular, like Samsung or Hynix, are talking about 300% type earnings growth and still trading at six times earnings.

Now, I know these are cyclical stocks, so you have to worry about when you run into peak earnings. But AI spending is still strong. Until you see hyperscaler capex start to be questioned, that is when I think the slowdown happens, and multiples start to correct.

Short-term rates potentially going up could also cause some multiple compression. Arguably, there is evidence that it's overbought. It's probably in the 95th percentile in terms of buying interest and ownership in these stocks.

Also Read | InterGlobe Aviation

But the earnings trajectory is still very strong and is likely to continue for a few quarters. That is the headwind for India in essence. You have seen those flows, plus retail flows, gravitating toward AI, not just in the US, but also in Korea and Taiwan.

Q: What has been keeping you busy in India? Because there are pockets where stocks are doing very well, unaffected by the negative sentiment and external factors. These are largely, though not entirely, non-foreign institutional investor (FII) stocks.

A: I think you are right. Foreigners are pulling out, and maybe they were too long a handful of names, the mega-caps. So, you have seen the brunt of the selling pressure there.

Partly because emerging markets, to a certain degree, saw outflows until more recently, with the AI trend picking up and inflows finally coming back in.

By and large, the space that has done well, including some of what we own, is power. It's energy in a sense, but specifically power plays that feed into AI.

You don't have many direct AI infrastructure plays in India. We own NetWeb. It's been a phenomenal performer. Multiples can be questioned, and there is a scarcity value in the Indian context.

But broadly, infrastructure plays like power has done well, and I continue to see that as a global phenomenon.

I have met a few North Asian and US companies, and the roadmap continues to be very strong in terms of demand. Even transformer companies from Korea to China continue to see massive backlogs. Lead times remain extended.

All of those points point to good pricing, strong demand and healthy order books.

Q: What about India as an investment theme? You had trimmed your exposure to India from around 14-15% to roughly 10%. What are you doing right now? Is there a reason to increase allocation, or are you still cautious? Also, have there been any recent changes in stocks like Shriram Finance or GMR?

A: Not a whole bunch of changes. We are pretty static. We want to see the earnings inflexion. Last time, I mentioned we were starting to warm up to GMR Airports. I think that is a good business. What you are seeing with the infusion of capital from the Japanese is helping not only capital levels but also the cost of capital through credit rating improvements.

Now the question is whether oil prices and near-term concerns around vehicle financing make investors a little more cautious.

On Glenmark Pharmaceuticals, it's interesting because the management team is actually in New York this week. It's a good business. Obviously, you've seen pressure from developments in West Asia, some flight cancellations and potentially some charges being reduced to help alleviate industry pressure.

But it's a great business model and a strong infrastructure asset. It has massive operating leverage, and they run the three principal airports extremely well.

To me, that's a nice Indian consumer proxy backed by hard assets. It's a name we like over the long term. The question is valuation and entry price. You have to pick your points carefully, but it's a good business.

Beyond that, there hasn't been much change.

I would say I am looking again at the pharma space. I have spent a lot of time with Chinese companies and also met Indian companies.

Anthem Biosciences has done some innovative things. I am focusing much more on the innovation and speciality side, where I think there are good prospects and strong dollar-earning opportunities.

Anthem Biosciences is another example. We have owned it since the initial public offering (IPO). It's a good business. They are looking at peptides and semaglutide-related opportunities. That's another area of growth, leaving aside what Chinese companies are doing and exporting in that space.

So, I do think there are opportunities there as well.

Q: You want to give us your take on SpaceX, and what kind of feedback have you got from where you're sitting?

A: It's a fascinating business. You have got to open the roadshow and even the prospectus. It's a brilliant business.

Also Read | Why RBI kept interest rates unchanged despite rising inflation risks

When you look at the three verticals, people get excited. Leave aside the launches, which are obviously the more glamorous part. Starlink itself is a significant opportunity with around 10 million subscribers and considerable room to scale.

Launches are going well. It's a good business.

You have also got the drag from the xAI side and the massive capex that goes into it.

It's attracted a lot of retail interest. It's a big deal. It's a fixed-price IPO at a $1.75 trillion valuation. There are probably a few others not far behind, looking to come to market.

Watch the full conversation here

We will have to see what market absorption looks like. We haven't seen IPOs of this scale before, but there is a fair amount of enthusiasm.

It's extremely unique. You are probably asking the wrong person to evaluate it, but people have made a lot of money from it.

Execution has been exceptional. If you look at the data centre buildout, they have put together this entire infrastructure in literally no time. So, overall, it's a great execution.

Catch all the latest updates from the stock market here

/images/ppid_a911dc6a-image-178098208936431633.webp)

/images/ppid_a911dc6a-image-178098202621620144.webp)

/images/ppid_a911dc6a-image-178098205768116750.webp)

/images/ppid_a911dc6a-image-178098202820930360.webp)