/images/ppid_59c68470-image-178358002366772572.webp)

/images/ppid_59c68470-image-178331255431569511.webp)

/images/ppid_59c68470-image-178338765293022446.webp)

/images/ppid_59c68470-image-178339514221412632.webp)

What is the story about?

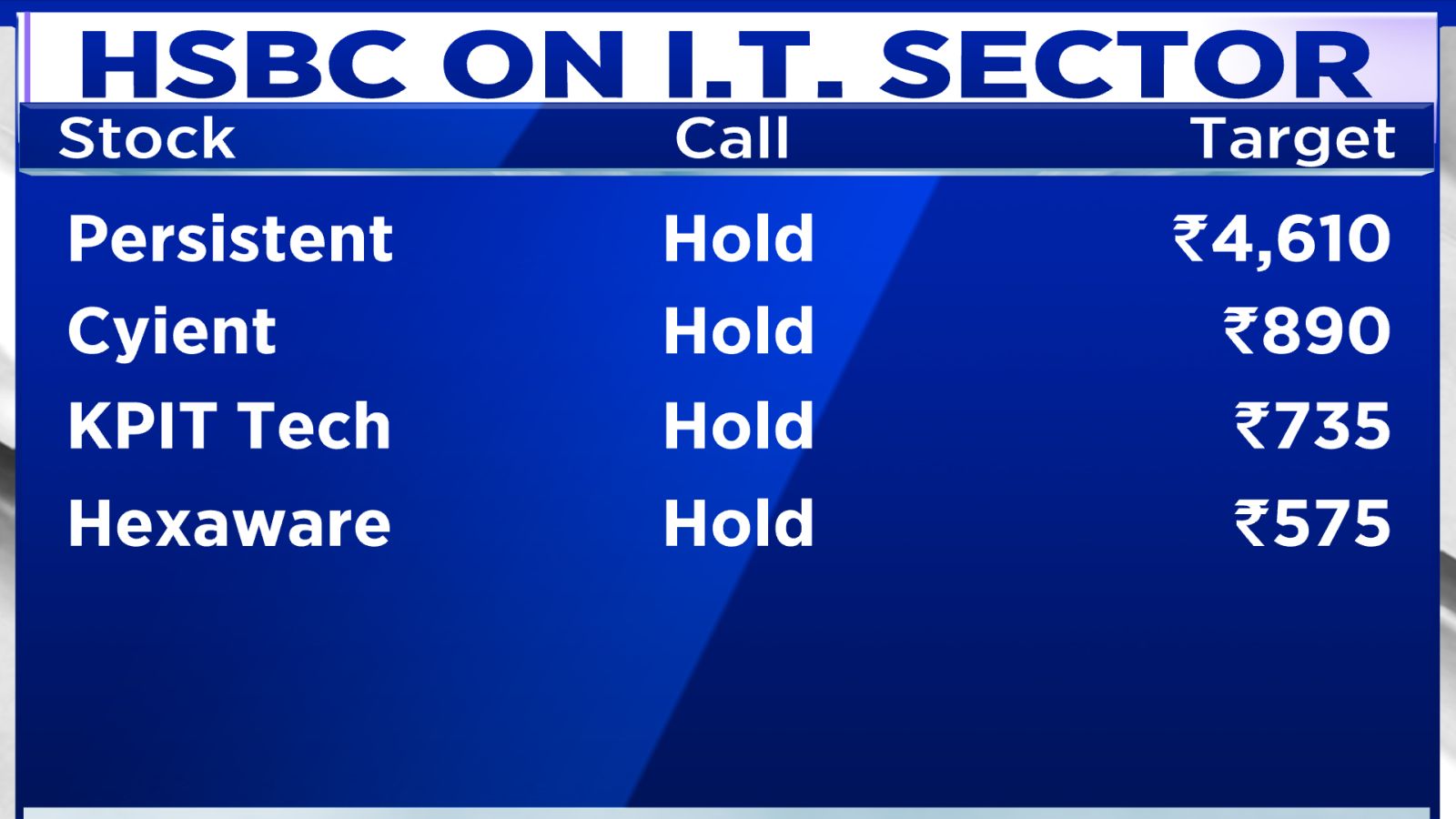

HSBC India expects the Indian IT sector to remain under pressure in FY27 as artificial intelligence-led pricing pressure weighs on earnings, but believes valuations have already factored in much of the weakness, limiting the downside for stocks.

According to Yogesh Aggarwal, Head of Research at HSBC India said, “FY27 is likely to be the worst year in terms of the negative AI impact, and things will start to improve in FY28 and maybe go back to normal in FY29. Therefore, when you factor that in in the long-term valuations, the 12-13 times forward PE, which the

stocks are trading today, is probably the bottom.”

He believes the downside for IT stocks is limited from current levels, although a sharp recovery is also unlikely in the near term. With FY27 expected to remain a weak year due to AI-led pricing pressure, he sees little urgency for investors to increase exposure to the sector.

He expects the industry to remain largely range-bound over the next year, while consensus earnings estimates for the current quarter could see modest downgrades as business conditions are likely to be slightly weaker than anticipated a few months ago.

He expects FY27 revenue growth for the sector to remain broadly flat, in the range of 0-2%, followed by another year of low single-digit growth in FY28 before returning to mid-single-digit growth in FY29.

On the automobile sector, Aggarwal said demand has remained stronger than expected despite recent vehicle price increases and higher fuel prices.

He noted that passenger vehicle demand has held up well after the GST rate reduction last year, with subsequent price hikes of 3-5% having little impact on consumer buying trends. However, he cautioned that a higher base in the second half of the year could moderate growth from October onwards.

On electric vehicles, Aggarwal said adoption is improving, with penetration reaching around 7-8% in passenger vehicles and nearly 10% in two-wheelers.

However, he expects the pace of adoption to moderate over the longer term as government incentives are gradually withdrawn and tax policies evolve.

Watch accompanying video for more Follow our live blog for more stock market updates

According to Yogesh Aggarwal, Head of Research at HSBC India said, “FY27 is likely to be the worst year in terms of the negative AI impact, and things will start to improve in FY28 and maybe go back to normal in FY29. Therefore, when you factor that in in the long-term valuations, the 12-13 times forward PE, which the

He believes the downside for IT stocks is limited from current levels, although a sharp recovery is also unlikely in the near term. With FY27 expected to remain a weak year due to AI-led pricing pressure, he sees little urgency for investors to increase exposure to the sector.

He expects the industry to remain largely range-bound over the next year, while consensus earnings estimates for the current quarter could see modest downgrades as business conditions are likely to be slightly weaker than anticipated a few months ago.

He expects FY27 revenue growth for the sector to remain broadly flat, in the range of 0-2%, followed by another year of low single-digit growth in FY28 before returning to mid-single-digit growth in FY29.

On the automobile sector, Aggarwal said demand has remained stronger than expected despite recent vehicle price increases and higher fuel prices.

He noted that passenger vehicle demand has held up well after the GST rate reduction last year, with subsequent price hikes of 3-5% having little impact on consumer buying trends. However, he cautioned that a higher base in the second half of the year could moderate growth from October onwards.

On electric vehicles, Aggarwal said adoption is improving, with penetration reaching around 7-8% in passenger vehicles and nearly 10% in two-wheelers.

However, he expects the pace of adoption to moderate over the longer term as government incentives are gradually withdrawn and tax policies evolve.

Watch accompanying video for more Follow our live blog for more stock market updates

/images/ppid_59c68470-image-178357252488036660.webp)

/images/ppid_59c68470-image-178358004906819822.webp)

/images/ppid_59c68470-image-178348503083162804.webp)

/images/ppid_59c68470-image-178349256126863012.webp)

/images/ppid_59c68470-image-178357011720533876.webp)

/images/ppid_59c68470-image-178333756360531474.webp)

/images/ppid_59c68470-image-178339009114876534.webp)

/images/ppid_59c68470-image-178332502875185886.webp)