/images/ppid_59c68470-image-177917259649669823.webp)

/images/ppid_a911dc6a-image-177939303354854007.webp)

What is the story about?

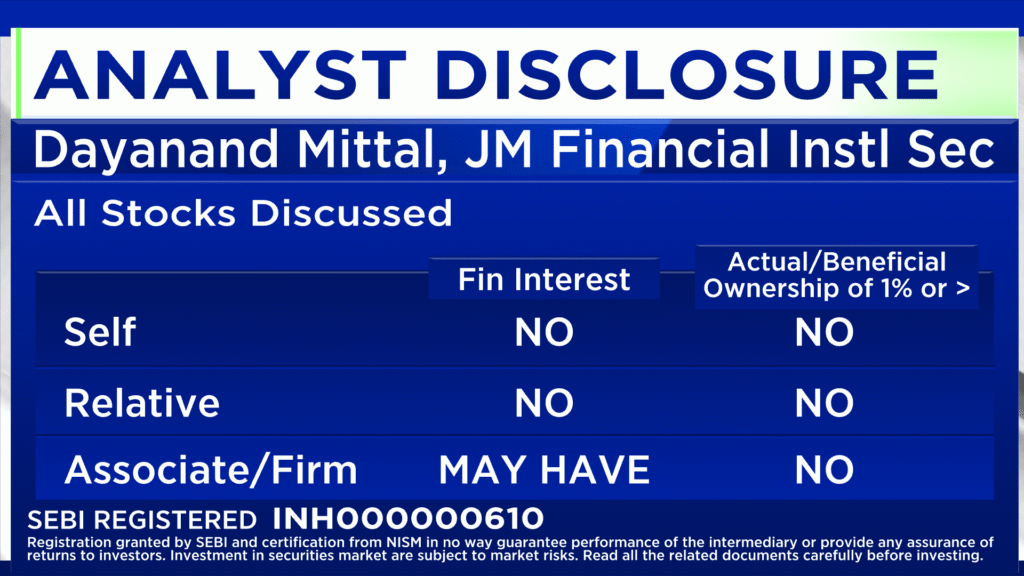

Petrol and diesel prices have been raised twice this week, putting the spotlight back on the oil sector. Dayanand Mittal, Oil & Gas and Telecom Research Analyst at JM Financial Institutional Securities, believes this could create an opportunity for upstream producers such as Oil and Natural Gas Corporation (ONGC), which stand to benefit from elevated crude prices.

Mittal said ONGC still offers around 15% upside despite the recent rally., as concerns around windfall taxes appear limited and crude prices are expected to remain relatively high over the next year.

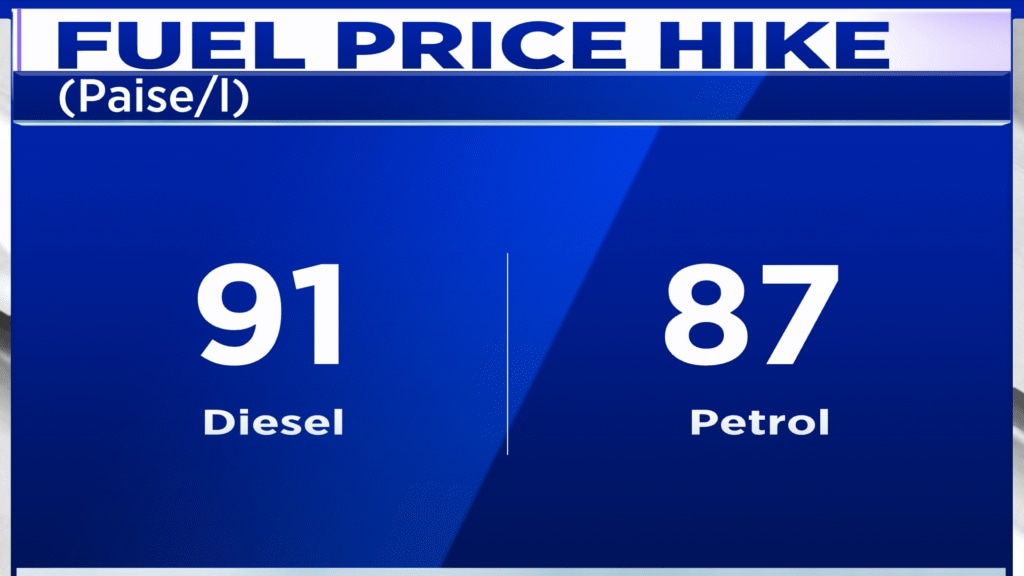

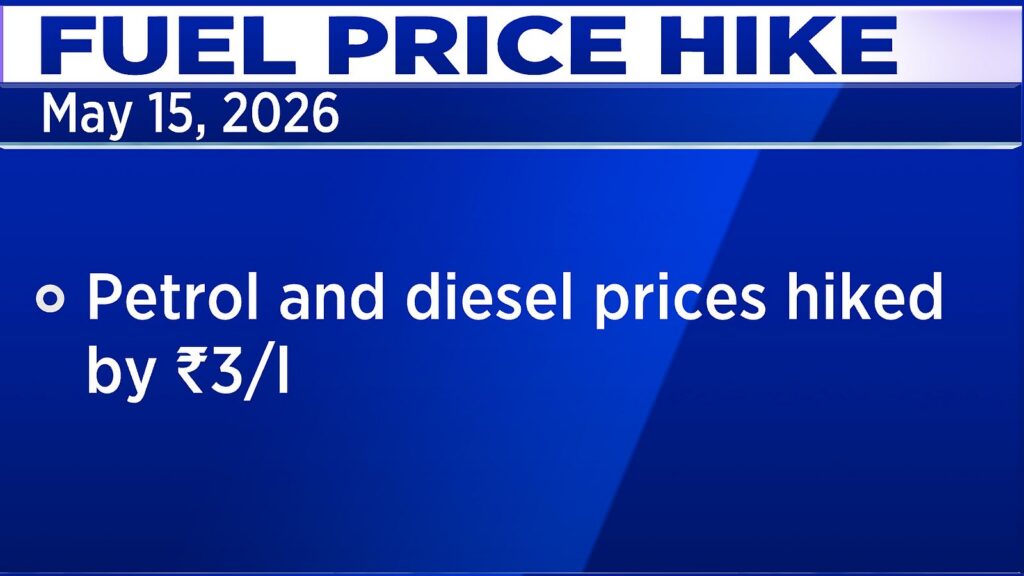

At the same time, he expects fuel retailers to remain under pressure, as India buys over 85% of its crude from abroad. When global oil prices rise, import costs go up. But pump prices have not kept pace. As a result, Indian Oil, BPCL, and HPCLare losing ₹15 to ₹17 on every litre sold.

"Original expectation when this fuel price hike rumour was going on... given OMCs are losing somewhere in the range of ₹15 to 17 per litre to get back to normalised earnings, there would be at least ₹5 hike," Mittal said. The two hikes this week add up to just ₹3.90 — barely a third of what's needed.

Also Read | Oil price pressure priced in, India offers selective opportunities: Raymond James strategist

More hikes will come, but slowly. Mittal expects another ₹2–3 in the coming weeks. A large one-time jump of ₹10 or more is off the table — it would push up the cost of everything that moves by truck and hit consumers hard. "If let's say crude stays upwards of $110 per barrel, consumers will take about one-third, maybe 40–50% of the hit. OMCs will have to absorb ₹5-7-10," he said.

Can the oil companies absorb that? For now, yes. Two good years before this crisis helped them pay down debt significantly. They have roughly two to three quarters of breathing room before things get truly uncomfortable.

Also Watch | WPI may stay elevated for months amid oil price surge: ICRA’s Aditi Nayar

Some argue oil companies should take all the pain — they made good money when oil was cheap. Mittal says that's only partly fair. Most of those profits went toward recovering from the massive losses of 2023, when crude last spiked above $100 after the war in Ukraine. "They can absorb almost like ₹2 lakh crore debt in case the worst were to be factored in," he said.

Watch the full conversation here

That is why he prefers ONGC. Unlike fuel retailers, ONGC sells oil at global market prices — it benefits when crude is high, rather than bleeding on it. The main investor worry has been a windfall tax on its profits. Mittal doesn't see that happening this time.

With the stock still priced as though oil will fall to $70 — against his forecast of $85 — he sees a gap the market hasn't closed yet. In a high-oil world, ONGC is one of the few Indian energy names built to gain, not just survive.

Catch all the latest updates from the stock market here

Mittal said ONGC still offers around 15% upside despite the recent rally., as concerns around windfall taxes appear limited and crude prices are expected to remain relatively high over the next year.

At the same time, he expects fuel retailers to remain under pressure, as India buys over 85% of its crude from abroad. When global oil prices rise, import costs go up. But pump prices have not kept pace. As a result, Indian Oil, BPCL, and HPCLare losing ₹15 to ₹17 on every litre sold.

"Original expectation when this fuel price hike rumour was going on... given OMCs are losing somewhere in the range of ₹15 to 17 per litre to get back to normalised earnings, there would be at least ₹5 hike," Mittal said. The two hikes this week add up to just ₹3.90 — barely a third of what's needed.

Also Read | Oil price pressure priced in, India offers selective opportunities: Raymond James strategist

More hikes will come, but slowly. Mittal expects another ₹2–3 in the coming weeks. A large one-time jump of ₹10 or more is off the table — it would push up the cost of everything that moves by truck and hit consumers hard. "If let's say crude stays upwards of $110 per barrel, consumers will take about one-third, maybe 40–50% of the hit. OMCs will have to absorb ₹5-7-10," he said.

Can the oil companies absorb that? For now, yes. Two good years before this crisis helped them pay down debt significantly. They have roughly two to three quarters of breathing room before things get truly uncomfortable.

Also Watch | WPI may stay elevated for months amid oil price surge: ICRA’s Aditi Nayar

Some argue oil companies should take all the pain — they made good money when oil was cheap. Mittal says that's only partly fair. Most of those profits went toward recovering from the massive losses of 2023, when crude last spiked above $100 after the war in Ukraine. "They can absorb almost like ₹2 lakh crore debt in case the worst were to be factored in," he said.

Watch the full conversation here

That is why he prefers ONGC. Unlike fuel retailers, ONGC sells oil at global market prices — it benefits when crude is high, rather than bleeding on it. The main investor worry has been a windfall tax on its profits. Mittal doesn't see that happening this time.

With the stock still priced as though oil will fall to $70 — against his forecast of $85 — he sees a gap the market hasn't closed yet. In a high-oil world, ONGC is one of the few Indian energy names built to gain, not just survive.

Catch all the latest updates from the stock market here

/images/ppid_a911dc6a-image-177939652584428477.webp)