/images/ppid_59c68470-image-178229009023738865.webp)

/images/ppid_59c68470-image-178221503599875243.webp)

/images/ppid_59c68470-image-17820925801628154.webp)

What is the story about?

The recent sell-off in US technology stocks should be viewed as a pause rather than the start of a broader market reversal, according to John Stoltzfus, Managing Director and Chief Investment Strategist at Oppenheimer Asset Management. He believes the long-term technology upgrade cycle remains intact, supported by strong corporate earnings, ongoing innovation and a Federal Reserve that is unlikely to raise interest rates this year.

Stoltzfus is also constructive on emerging markets (EMs), with India among his preferred long-term opportunities. As companies diversify supply chains beyond China and the artificial intelligence (AI) investment cycle expands globally, he says India is well positioned to benefit from re-globalisation through its growing strengths in technology, healthcare and manufacturing, although investors may need patience before returns fully reflect these fundamentals.

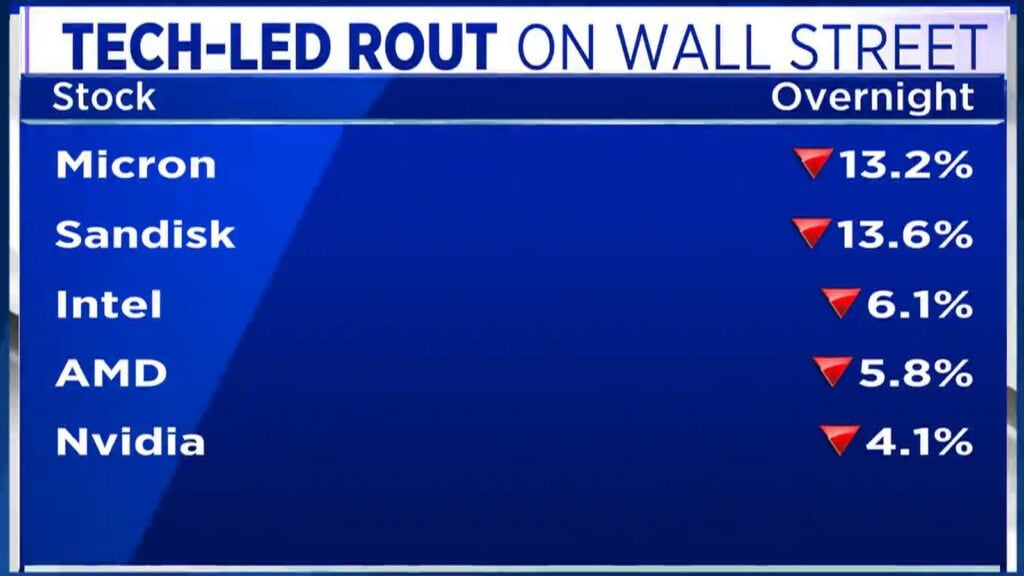

This is an edited transcript of the interview.Q: Every time there is a large tech sell-off, we ask whether it is routine profit-booking or the start of something bigger. Even after yesterday's sharp fall in individual names, many stocks are perhaps where they were a week ago. What is your assessment of the tech trade?

This is an edited transcript of the interview.Q: Every time there is a large tech sell-off, we ask whether it is routine profit-booking or the start of something bigger. Even after yesterday's sharp fall in individual names, many stocks are perhaps where they were a week ago. What is your assessment of the tech trade?

A: The first point we would make is that we are all on the upgrade cycle, whether we like it or not. There is a transformational change happening in technology. There is an argument over how much investment is too much investment, what will work and what won't. It creates a great opportunity for traders to play volatility, and it has been recurring.

If you look over the last few quarters, every time the S&P 500 earnings season has surprised to the upside. The most recent quarter delivered earnings growth of 27%. Going into the reporting season, consensus expectations were around 12-13% growth.

Once earnings season ends and investors wait for the next one to begin — with second-quarter reporting effectively starting on July 14 when the major banks report — markets tend to focus on other issues. In the meantime, attention will be on developments around the Strait of Hormuz, negotiations with Iran, and questions around which companies emerge as power players through this period.

At the same time, we have a rotational market that can shift from risk-on to risk-off on a day-to-day basis. That is advantageous for traders who position themselves well and move quickly. It is also beneficial for intermediate- and long-term investors who can pick up quality stocks that get unfairly sold off during pullbacks.

The S&P 500 is down only a little more than 3% since its June 2 peak. Technology is down around 8%, nearing correction territory. However, technology remains up 16.58% year-to-date and nearly 34% from its March low.

This looks more like a trim than a major turnaround. Some stocks have pulled back sharply, but when you consider how much they have risen from the start of the year or from the March lows, I don't think it's anything to worry about. If anything, it tests investors' patience and creates opportunities for traders.

Q: There are fears that a rate hike could come earlier than expected this year. If that happens, could it affect stocks in general and the technology rally?

A: We don't think the Federal Reserve is going to hike rates this year.

The market may speculate about it, but we have seen similar situations over the last two years when markets expected more hikes than the Fed was prepared to deliver.

The Federal Reserve remains very sensitive to its dual mandate. Its objective is to provide an interest-rate regime that supports sustainable economic growth while avoiding excessive inflation. At the same time, it seeks to maintain unemployment within a range that is broadly consistent with full employment.

Q: You believe US markets are merely pausing, earnings remain strong and the Fed is unlikely to hike rates. How would you position between developed and emerging markets? Where does India fit into this picture?

A: We entered this year at a time when many firms expected the US market to underperform after a long period of leadership. We took a different view because of the innovation taking place within technology.

We remain overweight the US while maintaining meaningful exposure to both emerging markets and developed international markets. Within our international allocation, we have a greater weighting towards emerging markets than developed markets.

Developed markets, particularly Europe and the UK, continue to face economic challenges. Government spending obligations are weighing on economic growth.

We like emerging markets and, in fact, they have been among the better-performing areas. After that, we would highlight US small- and mid-cap stocks, particularly small-caps.

As for India, it is sitting in the driver's seat. The world is diversifying away from dependence on China in global supply chains. That does not mean countries will stop doing business with China, but they need additional large-scale partners.

India has demonstrated increasing sophistication in healthcare, technology and manufacturing. There is still a need for infrastructure investment to improve efficiency, but from an intermediate- to long-term perspective, India is very well positioned.

Along with Mexico and Brazil among emerging markets, and Korea and Japan among developed markets, India stands to benefit from the re-globalisation process that has been underway for several years and is now accelerating.

Q: The re-globalisation trend may be accelerating, but it hasn't yet translated into Indian equity returns. Indian markets have underperformed for roughly 18 months, perhaps because they lack a strong AI trade. What are your expectations for India over the next 12 to 18 months?

A: We are very aware of India's recent underperformance. Whether viewed in local currency terms or in US dollars, Indian markets have been weak and have posted negative returns.

However, we believe the fundamentals tied to the AI trade, increased participation in global trade and the broader re-globalisation trend will eventually reward investors.

We think that point is getting closer. It could happen within the next six to twelve months, although patience may be required.

Watch the full conversation here

Remember that some of the greatest investors, including Warren Buffett, often buy when others are unwilling to do so. They invest in strong long-term stories before the market fully recognises them rather than chasing momentum later.

We believe there is reason for investors to remain constructive on India. At the same time, diversification remains critical — across geographies, sectors, market capitalisations and investment styles such as growth and value.

We see this as the return of diversification. Investors should avoid excessive concentration and focus on building balanced portfolios that can participate in long-term opportunities while limiting unnecessary near-term risk.

Catch all the latest updates from the stock market here

Stoltzfus is also constructive on emerging markets (EMs), with India among his preferred long-term opportunities. As companies diversify supply chains beyond China and the artificial intelligence (AI) investment cycle expands globally, he says India is well positioned to benefit from re-globalisation through its growing strengths in technology, healthcare and manufacturing, although investors may need patience before returns fully reflect these fundamentals.

This is an edited transcript of the interview.Q: Every time there is a large tech sell-off, we ask whether it is routine profit-booking or the start of something bigger. Even after yesterday's sharp fall in individual names, many stocks are perhaps where they were a week ago. What is your assessment of the tech trade?

A: The first point we would make is that we are all on the upgrade cycle, whether we like it or not. There is a transformational change happening in technology. There is an argument over how much investment is too much investment, what will work and what won't. It creates a great opportunity for traders to play volatility, and it has been recurring.

If you look over the last few quarters, every time the S&P 500 earnings season has surprised to the upside. The most recent quarter delivered earnings growth of 27%. Going into the reporting season, consensus expectations were around 12-13% growth.

Once earnings season ends and investors wait for the next one to begin — with second-quarter reporting effectively starting on July 14 when the major banks report — markets tend to focus on other issues. In the meantime, attention will be on developments around the Strait of Hormuz, negotiations with Iran, and questions around which companies emerge as power players through this period.

At the same time, we have a rotational market that can shift from risk-on to risk-off on a day-to-day basis. That is advantageous for traders who position themselves well and move quickly. It is also beneficial for intermediate- and long-term investors who can pick up quality stocks that get unfairly sold off during pullbacks.

The S&P 500 is down only a little more than 3% since its June 2 peak. Technology is down around 8%, nearing correction territory. However, technology remains up 16.58% year-to-date and nearly 34% from its March low.

This looks more like a trim than a major turnaround. Some stocks have pulled back sharply, but when you consider how much they have risen from the start of the year or from the March lows, I don't think it's anything to worry about. If anything, it tests investors' patience and creates opportunities for traders.

Q: There are fears that a rate hike could come earlier than expected this year. If that happens, could it affect stocks in general and the technology rally?

A: We don't think the Federal Reserve is going to hike rates this year.

The market may speculate about it, but we have seen similar situations over the last two years when markets expected more hikes than the Fed was prepared to deliver.

The Federal Reserve remains very sensitive to its dual mandate. Its objective is to provide an interest-rate regime that supports sustainable economic growth while avoiding excessive inflation. At the same time, it seeks to maintain unemployment within a range that is broadly consistent with full employment.

Q: You believe US markets are merely pausing, earnings remain strong and the Fed is unlikely to hike rates. How would you position between developed and emerging markets? Where does India fit into this picture?

A: We entered this year at a time when many firms expected the US market to underperform after a long period of leadership. We took a different view because of the innovation taking place within technology.

We remain overweight the US while maintaining meaningful exposure to both emerging markets and developed international markets. Within our international allocation, we have a greater weighting towards emerging markets than developed markets.

Developed markets, particularly Europe and the UK, continue to face economic challenges. Government spending obligations are weighing on economic growth.

We like emerging markets and, in fact, they have been among the better-performing areas. After that, we would highlight US small- and mid-cap stocks, particularly small-caps.

As for India, it is sitting in the driver's seat. The world is diversifying away from dependence on China in global supply chains. That does not mean countries will stop doing business with China, but they need additional large-scale partners.

India has demonstrated increasing sophistication in healthcare, technology and manufacturing. There is still a need for infrastructure investment to improve efficiency, but from an intermediate- to long-term perspective, India is very well positioned.

Along with Mexico and Brazil among emerging markets, and Korea and Japan among developed markets, India stands to benefit from the re-globalisation process that has been underway for several years and is now accelerating.

Q: The re-globalisation trend may be accelerating, but it hasn't yet translated into Indian equity returns. Indian markets have underperformed for roughly 18 months, perhaps because they lack a strong AI trade. What are your expectations for India over the next 12 to 18 months?

A: We are very aware of India's recent underperformance. Whether viewed in local currency terms or in US dollars, Indian markets have been weak and have posted negative returns.

However, we believe the fundamentals tied to the AI trade, increased participation in global trade and the broader re-globalisation trend will eventually reward investors.

We think that point is getting closer. It could happen within the next six to twelve months, although patience may be required.

Watch the full conversation here

Remember that some of the greatest investors, including Warren Buffett, often buy when others are unwilling to do so. They invest in strong long-term stories before the market fully recognises them rather than chasing momentum later.

We believe there is reason for investors to remain constructive on India. At the same time, diversification remains critical — across geographies, sectors, market capitalisations and investment styles such as growth and value.

We see this as the return of diversification. Investors should avoid excessive concentration and focus on building balanced portfolios that can participate in long-term opportunities while limiting unnecessary near-term risk.

Catch all the latest updates from the stock market here

/images/ppid_59c68470-image-17821076159803596.webp)

/images/ppid_59c68470-image-178219002564420953.webp)

/images/ppid_59c68470-image-178218263948454985.webp)

/images/ppid_59c68470-image-178217755652155016.webp)

/images/ppid_59c68470-image-178210752301867473.webp)