/images/ppid_59c68470-image-17787500253337215.webp)

/images/ppid_59c68470-image-177875253597591549.webp)

/images/ppid_a911dc6a-image-177874586110252130.webp)

What is the story about?

Solar glass manufacturer Borosil Renewables is targeting a 60% increase in installed capacity by financial year 2027-28 (FY28), said Executive Chairman Pradeep Kumar Kheruka. "We expect installed capacity to be in production or started up within this year. I can speak for 2028 that the figure should be about 60% higher in terms of turnover, profitability, everything," he said.

For 2026-27 (FY27), Kheruka expects a marginal improvement in performance, with volume growth flat at around 8% supported by operational efficiences before the new capacity comes on stream.

The company's next major earnings step-change is tied to a ₹950 crore capacity expansion. Borosil's board has approved the installation of two new solar glass furnaces of 300 tonne per day (TPD), which would lift total capacity from the current 1,000 TPD to 1,600 TPD.

Borosil Renewables reported its January-March 2026 quarter earnings for the financial year 2025-26 (FY26) on May 12.

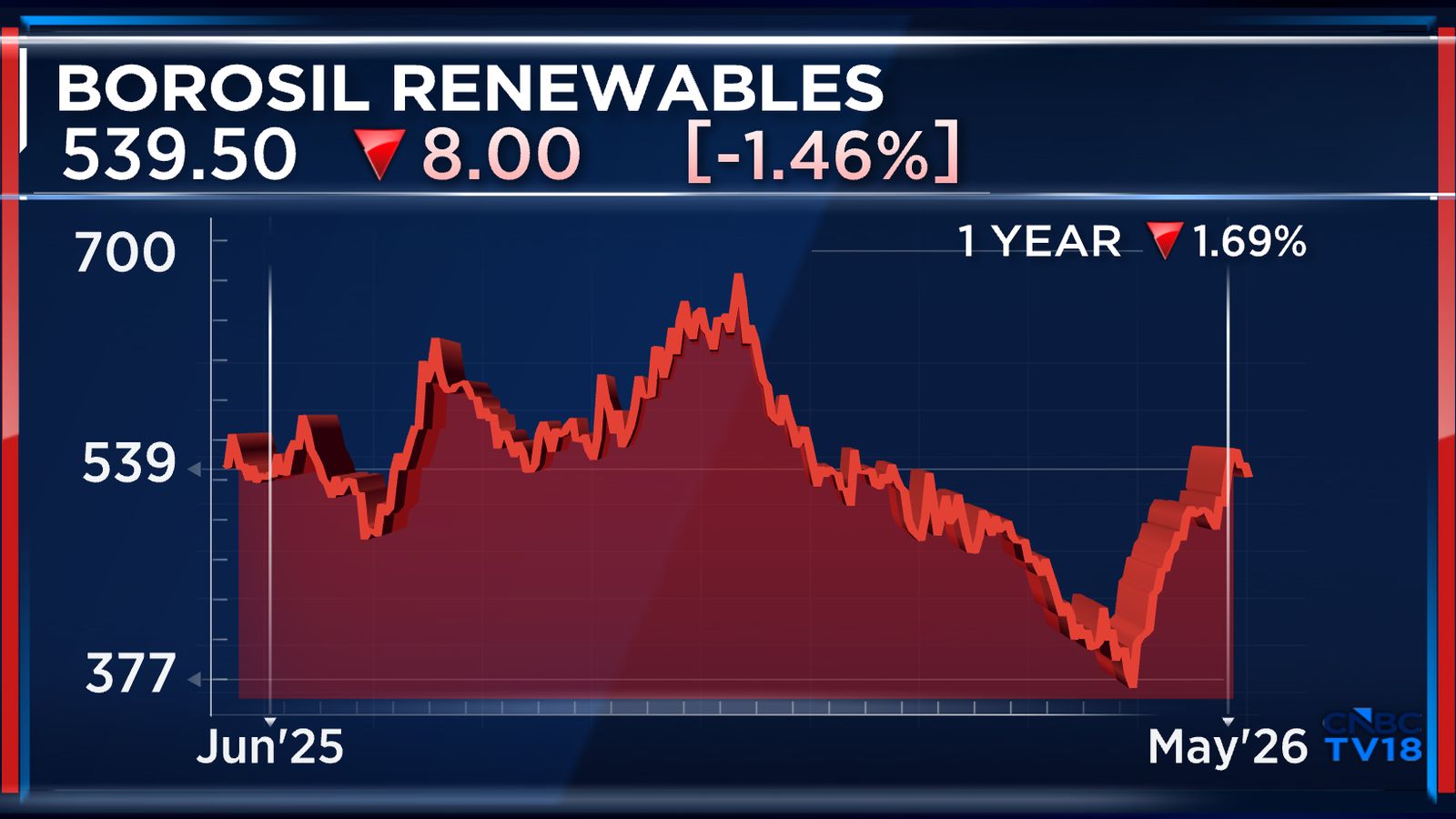

The company, which has a current market capitalisation of ₹7,420.20 crore, has seen its shares remain flat over the last year.

This is an edited transcript of the interview.Q: Put out the FY27 expectation, if you can on the top line, what are you expecting? And at an EBITDA level, what are you expecting? What kind of numbers?

A: The operational results for the year have shown is a reasonable margin of nearly ₹491 crore EBITDA, and the loss figure that you talked about is after setting off the loss that we had provided for last year from the German subsidiary. But operationally, we have done well.

Next year, we expect there to be a marginal improvement. Now, the way the expansion is coming up, we are online, to grow by about 60% this year, meaning we expect installed capacity to be in production or started up within this year. So, I can speak for 2028 that the figure should be about 60% higher in terms of turnover, profitability, everything.

This, of course, is subject to what we know, the uncertainties of everything, but everything seems to be going quite well in terms of demand, in terms of production, and there seems to be nothing on the horizon that should be interrupting us.

For the full interview, watch the accompanying videoQ: Some of the issues you've spoken about, which are the freight cost and now, of course, there is the power cost as well, right, with what's happening. Could you give us a sense of how that played out and what's playing out?

A: The power cost for us is not very bad because we are now significantly on renewable power, and with the renewable power that we now have, the prices are not subject to the power prices nationally otherwise. And the possibilities of natural gas going up do exist. But so far, we've had no curtailment in supply. We've had a marginal bump-up in the cost of natural gas, but we were able to pass on some of that to our customers, so we have not really suffered very much from power.

Going forward, I'm not sure. This is all very uncertain. On the one side, we see a lot of activity, which is geared towards solving the conflict. On the other side, of course, it's dragging on much longer than most of us would have expected. So other than that, I do not see any other major impediment on the horizon. Of course, some raw materials might go up, but that's a little uncertain. That could be because of freight rates and so on. I don't see any major roadblocks coming up.

Q: So, till your expansion comes on board, that's in December 2026, what would be the volume growth of the company for the first nine months of FY27? Last year, you were at 8%. Will it be similar? Will you do better? Can you push to double digits? And you said that the overall cost is manageable, so can you hold on to EBITDA margins of 30% that you clocked in during the quarter gone by?

A: Based on today's visibility, it seems that there should not be much change, and growth of about 8% is something that we could try to achieve within the year with further improvements in operational efficiencies and so on, and with the possibility of getting some extra production from at least one of the furnaces that we are planning to bring online. So, we expect that one furnace we might be able to light up in January, and the second furnace perhaps in March. So next year, of course, we can see 60% more glass coming out.

Q: You've also sought shareholder approval to raise ₹750 crore. Are you looking to raise that money? If yes, by when and what will it be used for?

A: At the moment, this is an enabling resolution. We are in a dynamic world. The solar business is taking off with even more energy than it was last year, and that's because of the uncertainty of oil supply and so on. People are shifting their focus to solar, and it's a matter of time before the nation moves away from LPG for cooking to induction heaters, which are more efficient. They are cheaper than LPG in terms of cost, and they are faster than LPG. So, induction cookers are the best way to go, and these use electricity.

Also Watch | Gas costs may spike, but Borosil Renewables expects to hold 30% margins

If you think of a billion people cooking on induction instead of LPG, that would add up to a sizeable demand. We're looking at data centres. So, at the moment, there seems to be no end to the demand for electric power. Everything associated with power is going to be on the rise.

Fortunately, we have negotiated the headwinds politically. We have sort of emerged unscathed, other than the cost of oil, to which there is no solution.

Q: Everything okay and set in terms of the duties? That's been a big mover for you.

A: And a very timely mover, I might say, because without it, you see, the government seems to have taken a consolidated, concerted decision to improve and to install a full-on manufacturing base in India for the entire solar value chain. And next year, we are seeing some further changes in terms of cells. We are seeing changes in cells coming in the next couple of months, when imported cells will no longer be allowed to be used. And after that, we will be looking at polysilicon, things like that. So, we are going to become a very strong renewable energy manufacturing power in India.

Catch all the latest updates from the stock market here

For 2026-27 (FY27), Kheruka expects a marginal improvement in performance, with volume growth flat at around 8% supported by operational efficiences before the new capacity comes on stream.

The company's next major earnings step-change is tied to a ₹950 crore capacity expansion. Borosil's board has approved the installation of two new solar glass furnaces of 300 tonne per day (TPD), which would lift total capacity from the current 1,000 TPD to 1,600 TPD.

Borosil Renewables reported its January-March 2026 quarter earnings for the financial year 2025-26 (FY26) on May 12.

The company, which has a current market capitalisation of ₹7,420.20 crore, has seen its shares remain flat over the last year.

This is an edited transcript of the interview.Q: Put out the FY27 expectation, if you can on the top line, what are you expecting? And at an EBITDA level, what are you expecting? What kind of numbers?

A: The operational results for the year have shown is a reasonable margin of nearly ₹491 crore EBITDA, and the loss figure that you talked about is after setting off the loss that we had provided for last year from the German subsidiary. But operationally, we have done well.

Next year, we expect there to be a marginal improvement. Now, the way the expansion is coming up, we are online, to grow by about 60% this year, meaning we expect installed capacity to be in production or started up within this year. So, I can speak for 2028 that the figure should be about 60% higher in terms of turnover, profitability, everything.

This, of course, is subject to what we know, the uncertainties of everything, but everything seems to be going quite well in terms of demand, in terms of production, and there seems to be nothing on the horizon that should be interrupting us.

For the full interview, watch the accompanying videoQ: Some of the issues you've spoken about, which are the freight cost and now, of course, there is the power cost as well, right, with what's happening. Could you give us a sense of how that played out and what's playing out?

A: The power cost for us is not very bad because we are now significantly on renewable power, and with the renewable power that we now have, the prices are not subject to the power prices nationally otherwise. And the possibilities of natural gas going up do exist. But so far, we've had no curtailment in supply. We've had a marginal bump-up in the cost of natural gas, but we were able to pass on some of that to our customers, so we have not really suffered very much from power.

Going forward, I'm not sure. This is all very uncertain. On the one side, we see a lot of activity, which is geared towards solving the conflict. On the other side, of course, it's dragging on much longer than most of us would have expected. So other than that, I do not see any other major impediment on the horizon. Of course, some raw materials might go up, but that's a little uncertain. That could be because of freight rates and so on. I don't see any major roadblocks coming up.

Q: So, till your expansion comes on board, that's in December 2026, what would be the volume growth of the company for the first nine months of FY27? Last year, you were at 8%. Will it be similar? Will you do better? Can you push to double digits? And you said that the overall cost is manageable, so can you hold on to EBITDA margins of 30% that you clocked in during the quarter gone by?

A: Based on today's visibility, it seems that there should not be much change, and growth of about 8% is something that we could try to achieve within the year with further improvements in operational efficiencies and so on, and with the possibility of getting some extra production from at least one of the furnaces that we are planning to bring online. So, we expect that one furnace we might be able to light up in January, and the second furnace perhaps in March. So next year, of course, we can see 60% more glass coming out.

Q: You've also sought shareholder approval to raise ₹750 crore. Are you looking to raise that money? If yes, by when and what will it be used for?

A: At the moment, this is an enabling resolution. We are in a dynamic world. The solar business is taking off with even more energy than it was last year, and that's because of the uncertainty of oil supply and so on. People are shifting their focus to solar, and it's a matter of time before the nation moves away from LPG for cooking to induction heaters, which are more efficient. They are cheaper than LPG in terms of cost, and they are faster than LPG. So, induction cookers are the best way to go, and these use electricity.

Also Watch | Gas costs may spike, but Borosil Renewables expects to hold 30% margins

If you think of a billion people cooking on induction instead of LPG, that would add up to a sizeable demand. We're looking at data centres. So, at the moment, there seems to be no end to the demand for electric power. Everything associated with power is going to be on the rise.

Fortunately, we have negotiated the headwinds politically. We have sort of emerged unscathed, other than the cost of oil, to which there is no solution.

Q: Everything okay and set in terms of the duties? That's been a big mover for you.

A: And a very timely mover, I might say, because without it, you see, the government seems to have taken a consolidated, concerted decision to improve and to install a full-on manufacturing base in India for the entire solar value chain. And next year, we are seeing some further changes in terms of cells. We are seeing changes in cells coming in the next couple of months, when imported cells will no longer be allowed to be used. And after that, we will be looking at polysilicon, things like that. So, we are going to become a very strong renewable energy manufacturing power in India.

Catch all the latest updates from the stock market here

/images/ppid_59c68470-image-177894503943539914.webp)

/images/ppid_59c68470-image-177881256761949868.webp)

/images/ppid_59c68470-image-177895252814252275.webp)