/images/ppid_59c68470-image-177572262814838050.webp)

What is the story about?

Jammu and Kashmir Bank was preparing to raise ₹750 crore from the market, via qualified institutional placement (QIP), by March 2026. However, the plan was beset by the war in West Asia, which has rattled risk appetite.

A QIP allows listed companies to raise capital by selling shares exclusively to qualified institutional buyers like banks and mutual funds, bypassing the need for costly, time-consuming public filings.

However, the CEO assured investors that the plan was still on. "Fortunately, our capital position is quite good. We will definitely, sometime in this quarter or next quarter, try to take it up," managing director and CEO Amitava Chatterjee told CNBC-TV18 on Thursday (April 9).

He also projected a 14–15% loan growth in the financial year ending March 2027, compared to the earlier guidance for a 12-15% growth, which could rise to 18% in the best-case scenario.

However, like many of its peers, the bank's primary concern has been the slow pace of deposit growth. Low-cost deposits have shrunk to 45.6% at the end of March 2026, down from 50.5% two years earlier.

A shrinking base of low-cost deposits tends to squeeze lenders' profit margins. CEO Chaudhary reassured investors that the figure would soon reach the company's internal target of 48%.

J&K Bank's credit-to-deposit ratio is 72%, much lower than larger peers like HDFC Bank and Axis Bank, where the ratio is in excess of 90%, and IDFC First Bank, at 102%.

The data shows that J&K Bank has relatively more headroom to push for loan growth without straining profitability.

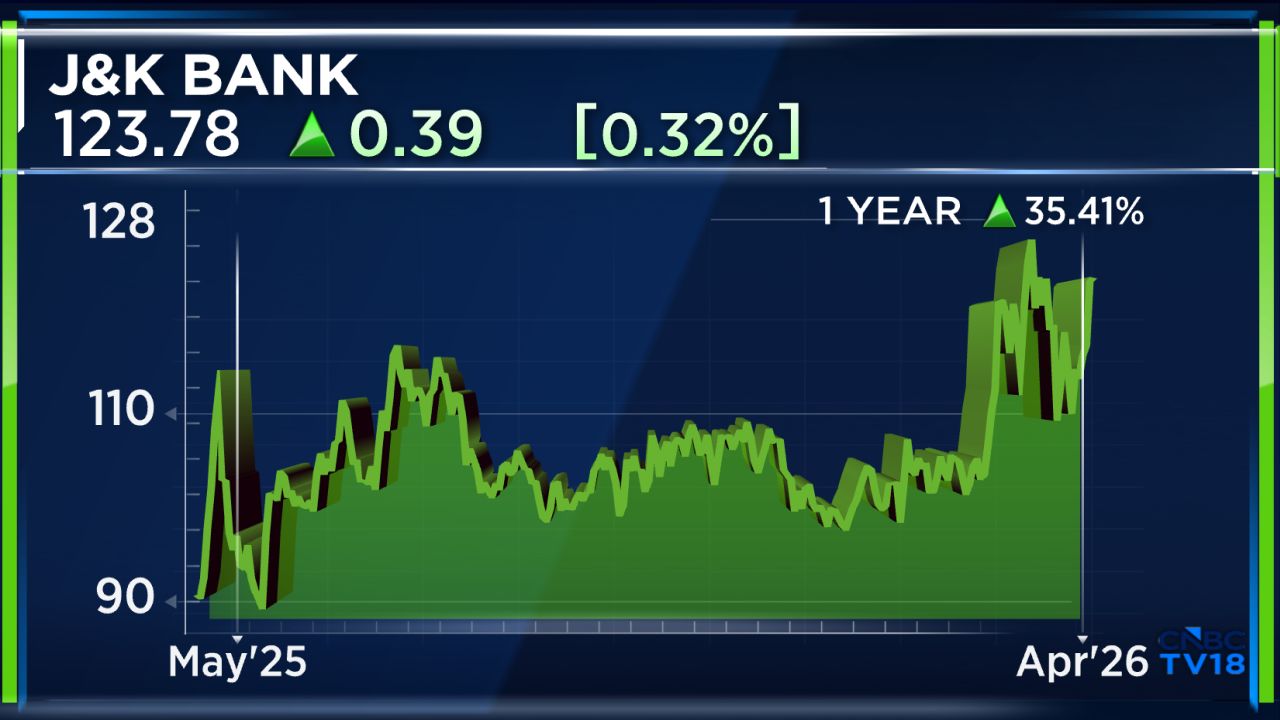

The company has seen its shares gain more than 35% over the last year, underperforming many of its peers. However, it ranks sixth among all banking stocks in terms of returns over the last five years.

For the full interview, watch the accompanying video

A QIP allows listed companies to raise capital by selling shares exclusively to qualified institutional buyers like banks and mutual funds, bypassing the need for costly, time-consuming public filings.

However, the CEO assured investors that the plan was still on. "Fortunately, our capital position is quite good. We will definitely, sometime in this quarter or next quarter, try to take it up," managing director and CEO Amitava Chatterjee told CNBC-TV18 on Thursday (April 9).

He also projected a 14–15% loan growth in the financial year ending March 2027, compared to the earlier guidance for a 12-15% growth, which could rise to 18% in the best-case scenario.

However, like many of its peers, the bank's primary concern has been the slow pace of deposit growth. Low-cost deposits have shrunk to 45.6% at the end of March 2026, down from 50.5% two years earlier.

A shrinking base of low-cost deposits tends to squeeze lenders' profit margins. CEO Chaudhary reassured investors that the figure would soon reach the company's internal target of 48%.

J&K Bank's credit-to-deposit ratio is 72%, much lower than larger peers like HDFC Bank and Axis Bank, where the ratio is in excess of 90%, and IDFC First Bank, at 102%.

The data shows that J&K Bank has relatively more headroom to push for loan growth without straining profitability.

The company has seen its shares gain more than 35% over the last year, underperforming many of its peers. However, it ranks sixth among all banking stocks in terms of returns over the last five years.

| Stock | Last five years returns |

| Karur Vysya Bank | 490% |

| Union Bank of India | 410.5% |

| South Indian Bank | 396.2% |

| Canara Bank | 373.2% |

| J&K Bank | 370.6% |

| Karnataka Bank | 290% |

| Bank of Baroda | 276.6% |

| Federal Bank | 266% |

| Bank of Maharashtra | 233.7% |

| Punjab National Bank | 196.5% |

For the full interview, watch the accompanying video

/images/ppid_a911dc6a-image-177572223080167316.webp)

/images/ppid_a911dc6a-image-177572225959642827.webp)

/images/ppid_a911dc6a-image-177572202907971180.webp)

/images/ppid_a911dc6a-image-17757215607332159.webp)

/images/ppid_a911dc6a-image-177572152946925398.webp)