/images/ppid_59c68470-image-178219002564420953.webp)

What is the story about?

Drew Pettit, Director-US Equity Strategy/ETF Analysis & Strategy Research at Citi, believes the recent technology sell-off is largely a "flash in the pan," with the artificial intelligence (AI) investment cycle remaining intact.

He says earnings resilience, continued spending and strong structural growth in AI, particularly semiconductors, should keep investors focused on the theme. Citi continues to favour AI-linked markets such as South Korea and Taiwan, while remaining underweight on India due to relatively weaker earnings revisions.

Pettit says Citi's decision to raise its S&P 500 target to 8,100 is driven entirely by stronger earnings expectations. The firm has increased its 2026 earnings estimate to $350 from $320, supported by broad-based positive earnings revisions. While valuations remain elevated and signs of risk exuberance are building, Pettit argues current market optimism is still supported by earnings growth and is not yet comparable to the excesses seen during the dot-com era.

This is an edited transcript of the interview.Q: Yesterday we saw a bit of a tech sell-off. Do you think it's a flash in the pan and the rally will resume after a dip? And as that happens, what is your call on emerging markets, including India, which do not have AI plays but have strong domestic structural growth stories?

This is an edited transcript of the interview.Q: Yesterday we saw a bit of a tech sell-off. Do you think it's a flash in the pan and the rally will resume after a dip? And as that happens, what is your call on emerging markets, including India, which do not have AI plays but have strong domestic structural growth stories?

A: We do think it is a little bit of a flash in the pan. Sentiment is really high and we understand investors taking profits in markets like this. But when you think about the large-cap growth story in the United States and the AI story globally, earnings resilience is there and spending is there. It has been good for the global economy and remains a strong theme.

We think investors will continue to gravitate toward these structural growth stories. The AI trade is real and continues, especially in semiconductors.

When we think about emerging markets broadly, our global team has moved the asset class to neutral. However, the areas we want to overweight are South Korea and Taiwan because of their ties to the AI trade. We also like South Africa, but that is more of an earnings revision story.

Markets like India, where we are underweight, have not seen earnings upgrades to the same extent, even though structural growth stories and Purchasing Managers' Index (PMI) remain reasonably healthy beneath the surface.

When you put it all together, there is really one consistent theme in markets today: buy earnings momentum. You are getting that primarily from AI, along with a few select pockets outside the theme.

Q: You have also raised your target on the S&P 500. The last time we spoke it was 7,700 and now you are pencilling in 8,100. What is driving the upside?

A: It's all our earnings expectations. The last time we spoke, our 2026 earnings estimate was $320. We have moved that to $350. We saw a lot of strength in the first quarter and we're seeing a broadening of positive earnings revisions.

About 75% of revisions last month for S&P 500 companies were to the upside.

At the same time, rates are a little higher, so we've actually trimmed our expected market multiple slightly. But what's driving the upside is entirely earnings.

It's earnings, earnings and more earnings.

Q: From an India market perspective, you are underweight India. We would like crude oil prices to cool off, and you seem to be building in further correction in crude prices given the de-escalation and the possibility of a deal. Also, do you think a more hawkish Fed could become a risk for global equity markets?

A: Let's start with oil. Lower oil prices are good for a market like India. They are also positive for the broadening trade in the United States and for Europe. However, we still think markets will narrow back toward the strongest earnings growth stories.

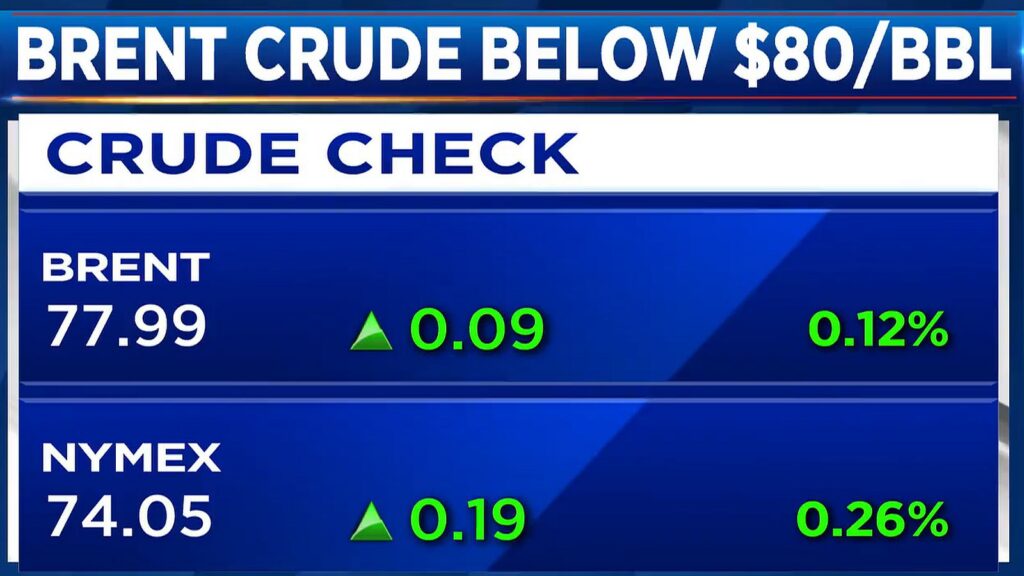

On Brent specifically, our commodities team expects around $75 per barrel this quarter, falling to $70 next quarter and moving toward the mid-$60s in 2027 because demand fundamentals are not particularly strong.

So, Brent is on a downward trend, which is positive.

On the other side, a more hawkish tone from the Fed could dampen the broadening trade. It's a bit of a balancing act, which is why we don't have strong conviction on that theme going forward.

Kevin Warsh was certainly more hawkish. From a rates perspective, our teams are more neutral in the near term. If we see some softening outside AI, rates could move lower over the longer term.

For now, the positives from lower oil prices and the negatives from higher rates largely offset each other, so we don't have a great deal of conviction either way.

Q: You have said global risk exuberance is building, but we are not yet at 1999 levels. What signals are you seeing?

A: Valuations are high. Everybody understands that.

When we look beneath the surface, we think the US market is already pricing in roughly 10% growth over the next five years. That's a high expectation, but we believe earnings growth can exceed that.

So, we are not yet at a point where markets are pricing in unrealistic growth relative to what companies can actually deliver.

We do see very elevated retail trading activity, which is pushing some of our sentiment indicators higher. Positioning and fund flows are also very strong and extended, with investors already heavily invested.

In addition, margin debt in the United States has risen significantly, which is another factor pushing sentiment indicators higher.

Compared with 1999, today's environment is certainly euphoric, but I would not describe it as irrationally exuberant to the same extent.

Q: On the AI trade itself, which part of the value chain still has more room to run? Many investors are beginning to question whether demand and revenues will justify the massive AI-related capex being undertaken by large technology companies.

A: That's a fair concern, and it's the key risk. What our AI teams are seeing is that cash return on investment for the hyperscalers—the Magnificent Seven and other large US technology companies—is beginning to stabilise.

These companies have substantial access to capital markets, and we have seen that through increased debt issuance. That continues to support the front end of the AI value chain.

Because of that stabilisation, we still like large-cap growth and exposure to indices such as the Nasdaq 100.

At the front end of the value chain, it's not just semiconductors. Several industrial and materials companies tied to AI are also benefiting. They have strong pricing power, improving margins and better asset efficiency.

Those trades are working alongside the technology components of the AI story. So, we are seeing a broadening within the AI trade that complements the hyperscalers, which remain the liquidity core of the theme.

Q: Here's a thought. Stocks in Korea and Taiwan, such as SK Hynix, TSMC and Samsung, benefited from the scarcity of AI plays. But as more AI-related companies get listed in the US, could money shift away from Korea and Taiwan toward these new opportunities? Is that a risk for emerging markets?

A: It's definitely a risk. Whenever equity supply increases, investors need to find capital to fund those investments. They can't create it out of thin air.

Cash levels remain relatively high and leverage is already extended, but there is still room for that to grow.

The other point is that if investors lack conviction in growth, they are unlikely to buy those stocks. When we look across the market, areas such as software and many traditional cyclicals that have not delivered earnings momentum continue to be sold.

Watch the full conversation here

What tends to happen when new equity supply comes to market is that investors narrow their focus toward the highest-conviction themes, which today are AI and quality earnings growth.

As a result, earnings momentum remains relatively insulated compared with other parts of the market that investors have largely avoided and continue to sell.

Catch all the latest updates from the stock market here

He says earnings resilience, continued spending and strong structural growth in AI, particularly semiconductors, should keep investors focused on the theme. Citi continues to favour AI-linked markets such as South Korea and Taiwan, while remaining underweight on India due to relatively weaker earnings revisions.

Pettit says Citi's decision to raise its S&P 500 target to 8,100 is driven entirely by stronger earnings expectations. The firm has increased its 2026 earnings estimate to $350 from $320, supported by broad-based positive earnings revisions. While valuations remain elevated and signs of risk exuberance are building, Pettit argues current market optimism is still supported by earnings growth and is not yet comparable to the excesses seen during the dot-com era.

This is an edited transcript of the interview.Q: Yesterday we saw a bit of a tech sell-off. Do you think it's a flash in the pan and the rally will resume after a dip? And as that happens, what is your call on emerging markets, including India, which do not have AI plays but have strong domestic structural growth stories?

A: We do think it is a little bit of a flash in the pan. Sentiment is really high and we understand investors taking profits in markets like this. But when you think about the large-cap growth story in the United States and the AI story globally, earnings resilience is there and spending is there. It has been good for the global economy and remains a strong theme.

We think investors will continue to gravitate toward these structural growth stories. The AI trade is real and continues, especially in semiconductors.

When we think about emerging markets broadly, our global team has moved the asset class to neutral. However, the areas we want to overweight are South Korea and Taiwan because of their ties to the AI trade. We also like South Africa, but that is more of an earnings revision story.

Markets like India, where we are underweight, have not seen earnings upgrades to the same extent, even though structural growth stories and Purchasing Managers' Index (PMI) remain reasonably healthy beneath the surface.

When you put it all together, there is really one consistent theme in markets today: buy earnings momentum. You are getting that primarily from AI, along with a few select pockets outside the theme.

Q: You have also raised your target on the S&P 500. The last time we spoke it was 7,700 and now you are pencilling in 8,100. What is driving the upside?

A: It's all our earnings expectations. The last time we spoke, our 2026 earnings estimate was $320. We have moved that to $350. We saw a lot of strength in the first quarter and we're seeing a broadening of positive earnings revisions.

About 75% of revisions last month for S&P 500 companies were to the upside.

At the same time, rates are a little higher, so we've actually trimmed our expected market multiple slightly. But what's driving the upside is entirely earnings.

It's earnings, earnings and more earnings.

Q: From an India market perspective, you are underweight India. We would like crude oil prices to cool off, and you seem to be building in further correction in crude prices given the de-escalation and the possibility of a deal. Also, do you think a more hawkish Fed could become a risk for global equity markets?

A: Let's start with oil. Lower oil prices are good for a market like India. They are also positive for the broadening trade in the United States and for Europe. However, we still think markets will narrow back toward the strongest earnings growth stories.

On Brent specifically, our commodities team expects around $75 per barrel this quarter, falling to $70 next quarter and moving toward the mid-$60s in 2027 because demand fundamentals are not particularly strong.

So, Brent is on a downward trend, which is positive.

On the other side, a more hawkish tone from the Fed could dampen the broadening trade. It's a bit of a balancing act, which is why we don't have strong conviction on that theme going forward.

Kevin Warsh was certainly more hawkish. From a rates perspective, our teams are more neutral in the near term. If we see some softening outside AI, rates could move lower over the longer term.

For now, the positives from lower oil prices and the negatives from higher rates largely offset each other, so we don't have a great deal of conviction either way.

Q: You have said global risk exuberance is building, but we are not yet at 1999 levels. What signals are you seeing?

A: Valuations are high. Everybody understands that.

When we look beneath the surface, we think the US market is already pricing in roughly 10% growth over the next five years. That's a high expectation, but we believe earnings growth can exceed that.

So, we are not yet at a point where markets are pricing in unrealistic growth relative to what companies can actually deliver.

We do see very elevated retail trading activity, which is pushing some of our sentiment indicators higher. Positioning and fund flows are also very strong and extended, with investors already heavily invested.

In addition, margin debt in the United States has risen significantly, which is another factor pushing sentiment indicators higher.

Compared with 1999, today's environment is certainly euphoric, but I would not describe it as irrationally exuberant to the same extent.

Q: On the AI trade itself, which part of the value chain still has more room to run? Many investors are beginning to question whether demand and revenues will justify the massive AI-related capex being undertaken by large technology companies.

A: That's a fair concern, and it's the key risk. What our AI teams are seeing is that cash return on investment for the hyperscalers—the Magnificent Seven and other large US technology companies—is beginning to stabilise.

These companies have substantial access to capital markets, and we have seen that through increased debt issuance. That continues to support the front end of the AI value chain.

Because of that stabilisation, we still like large-cap growth and exposure to indices such as the Nasdaq 100.

At the front end of the value chain, it's not just semiconductors. Several industrial and materials companies tied to AI are also benefiting. They have strong pricing power, improving margins and better asset efficiency.

Those trades are working alongside the technology components of the AI story. So, we are seeing a broadening within the AI trade that complements the hyperscalers, which remain the liquidity core of the theme.

Q: Here's a thought. Stocks in Korea and Taiwan, such as SK Hynix, TSMC and Samsung, benefited from the scarcity of AI plays. But as more AI-related companies get listed in the US, could money shift away from Korea and Taiwan toward these new opportunities? Is that a risk for emerging markets?

A: It's definitely a risk. Whenever equity supply increases, investors need to find capital to fund those investments. They can't create it out of thin air.

Cash levels remain relatively high and leverage is already extended, but there is still room for that to grow.

The other point is that if investors lack conviction in growth, they are unlikely to buy those stocks. When we look across the market, areas such as software and many traditional cyclicals that have not delivered earnings momentum continue to be sold.

Watch the full conversation here

What tends to happen when new equity supply comes to market is that investors narrow their focus toward the highest-conviction themes, which today are AI and quality earnings growth.

As a result, earnings momentum remains relatively insulated compared with other parts of the market that investors have largely avoided and continue to sell.

Catch all the latest updates from the stock market here

/images/ppid_a911dc6a-image-178191522336153101.webp)