/images/ppid_59c68470-image-177580253115450927.webp)

/images/ppid_59c68470-image-177556003669717195.webp)

What is the story about?

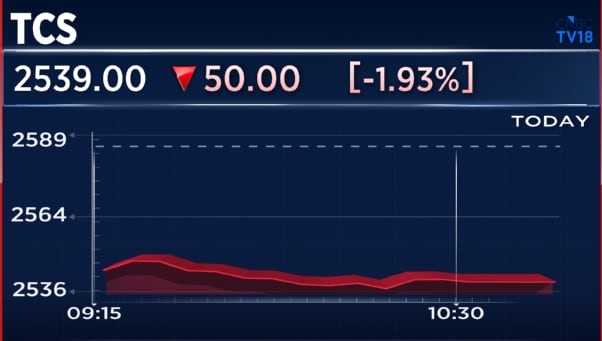

Shares of Tata Consultancy Services Ltd. (TCS) declined over 3% on Friday, April 10, as investors reacted to its fourth-quarter earnings. The stock had rallied 10% in April until yesterday.

TCS reported a 2.4% decline in constant currency revenue for FY26, underperforming peers and raising concerns over demand momentum.

2. Margin disappointment despite tailwinds

While EBIT margins expanded marginally by 10 basis points, this came despite a 110 basis points currency tailwind. The company continues to reinvest gains back into the business, with FY27 margin expansion expected to remain modest at around 20 basis points.

3. Market share

3. Market share

Brokerage firm CLSA said that TCS has been losing market share to Indian IT peers and sees limited evidence of a recovery in the near term, both in reported numbers and order book visibility.

Despite the near-term concerns, deal wins remained strong, and artificial intelligence-led revenues now contribute around 7.5% of total revenue.

4. Valuations

While valuations remain attractive, growth remains a concern. According to Kotak Institutional Equities, TCS trades at an 18.4% discount to HCL Technologies and a 3.6% discount to Infosys.

The brokerage believes the stock does not need to lead sector growth to perform, but a meaningful narrowing of the growth gap is crucial.

TCS currently trades at around 15.2 times forward earnings, with earnings per share expected to grow 14% in FY27 and 7% in FY28.

According to consensus estimates, 72% of the 51 analysts tracking the stock have a 'Buy' rating, while 18% recommend 'Hold' and 10% suggest 'Sell'.

So, what led to the fall?

1. Weak constant currency growthTCS reported a 2.4% decline in constant currency revenue for FY26, underperforming peers and raising concerns over demand momentum.

2. Margin disappointment despite tailwinds

While EBIT margins expanded marginally by 10 basis points, this came despite a 110 basis points currency tailwind. The company continues to reinvest gains back into the business, with FY27 margin expansion expected to remain modest at around 20 basis points.

3. Market share

Brokerage firm CLSA said that TCS has been losing market share to Indian IT peers and sees limited evidence of a recovery in the near term, both in reported numbers and order book visibility.

Despite the near-term concerns, deal wins remained strong, and artificial intelligence-led revenues now contribute around 7.5% of total revenue.

4. Valuations

While valuations remain attractive, growth remains a concern. According to Kotak Institutional Equities, TCS trades at an 18.4% discount to HCL Technologies and a 3.6% discount to Infosys.

The brokerage believes the stock does not need to lead sector growth to perform, but a meaningful narrowing of the growth gap is crucial.

TCS currently trades at around 15.2 times forward earnings, with earnings per share expected to grow 14% in FY27 and 7% in FY28.

According to consensus estimates, 72% of the 51 analysts tracking the stock have a 'Buy' rating, while 18% recommend 'Hold' and 10% suggest 'Sell'.

/images/ppid_59c68470-image-177579018858455502.webp)

/images/ppid_59c68470-image-177573271409585418.webp)

/images/ppid_59c68470-image-177571507904798940.webp)

/images/ppid_59c68470-image-17757201625882095.webp)

/images/ppid_59c68470-image-177564004198128321.webp)

/images/ppid_59c68470-image-177573761155911569.webp)

/images/ppid_59c68470-image-177579525782061891.webp)

/images/ppid_59c68470-image-177573256842927278.webp)

/images/ppid_59c68470-image-177578506941644426.webp)