/images/ppid_59c68470-image-178038503070079270.webp)

/images/ppid_59c68470-image-178028780927943095.webp)

/images/ppid_59c68470-image-178027762133550163.webp)

What is the story about?

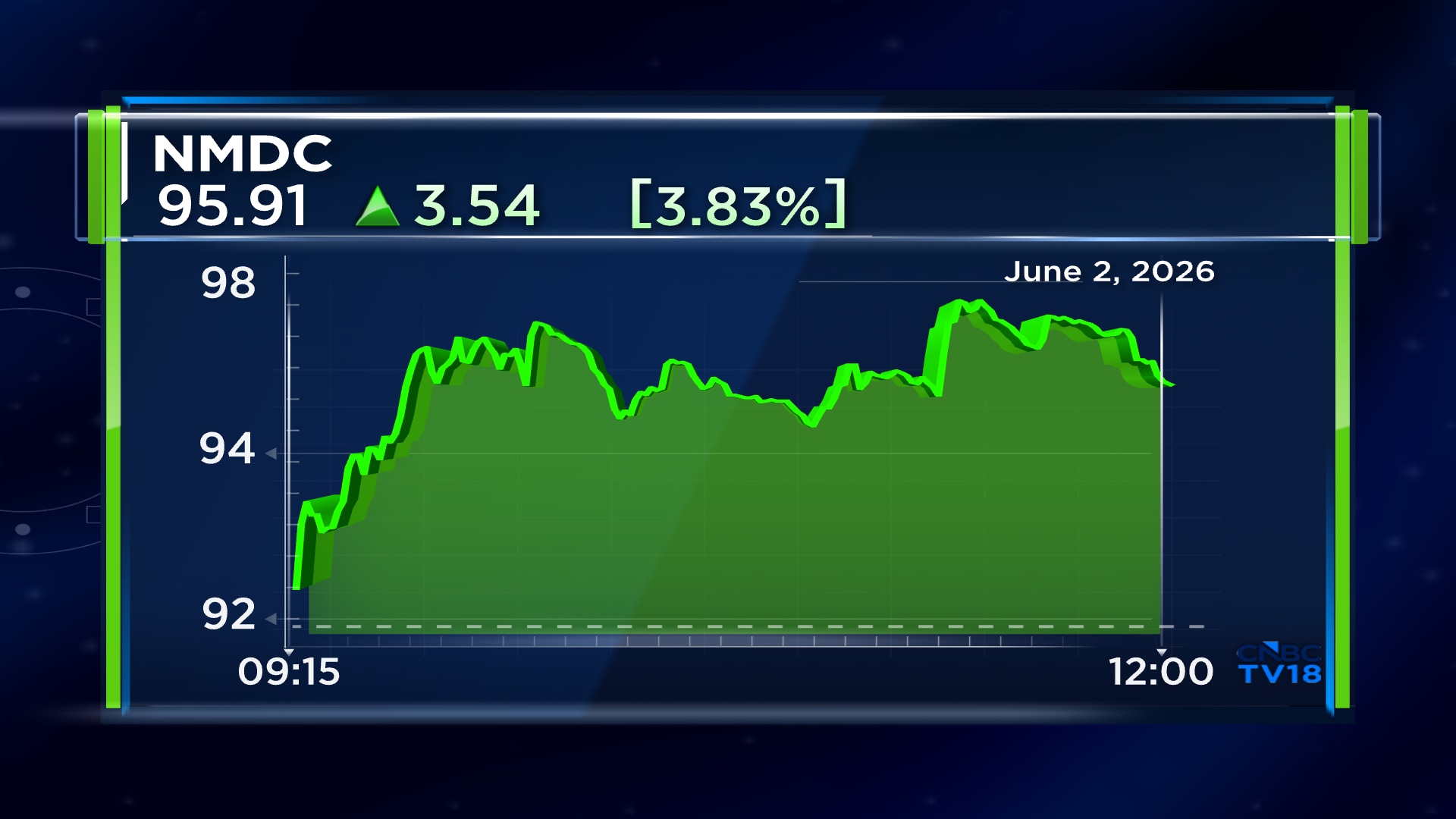

Shares of NMDC Ltd. gained 5% for the second day on Tuesday, June 2, as they continued to react to their recent earnings and production updates. The stock has now gained in five out of the last six trading sessions.

For the month of May, NMDC's production increased 20% to 5.31 MT from 4.43 MT in the year-ago period. Its offtake declined 7% to 4.04 MT from 4.34 MT in May last year. Its Karnataka offtake was at 0.7 MT compared to 1.34 MT in the previous year.

The state-run company's Earnings Before Interest, Taxes, Depreciation and amortisation (EBITDA) of ₹2,644 crore was below ICICI Securities' estimate of ₹3,090 crore.

Its pellet and other minerals business reported an EBIT loss of ₹102.4 crore compared to a loss of ₹10.8 crore in the previous quarter.

NMDC has taken a price hike of ₹500 to ₹600 per tonne in the first quarter of the financial year 2027. It is targeting 60 MT in FY27 and 100 MT by FY30 compared to 50.1 MT in FY26. Its capex for this fiscal is ₹6,000 crore.

Brokerages have mixed views on the stock, with Nuvama maintaining its "hold" rating but increasing its price target, Citi having a "sell" recommendation and Systematix having a "buy" rating.

The brokerage has maintained its "hold" rating on the stock but has increased its price target to ₹100 per share from the previous ₹85 apiece.

It has raised its EBITDA estimates for FY27 and FY28 by 13% and 16%, respectively. It said it is factoring in higher volume and iron ore prices.

The brokerage has a "sell" rating on NMDC with a price target of ₹85 apiece.

It expects domestic iron ore prices to be rangebound. Lloyds Metal and Energy has enhanced ore capacity from 10 MT to 25 MT, the brokerage said.

The brokerage has maintained its "buy" rating on the stock with a price target of ₹112 apiece.

It said NMDC reported strong execution in FY26 and that its future growth trajectory remains intact.

The company's management has guided for FY27 production to be 60 MT and it also expects the EBITDA margin to recover to between 35% - 40%.

Systematix has raised its EBITDA estimates for FY27 and FY28 by 10% and 8% and PAT estimates by 23% and 21%, respectively.

The brokerage said the revision is built on NMDC's strong execution track record.

Of the 23 analysts who have coverage on the stock, 10 have a "buy" rating, four have a "hold" rating and nine have a "sell" rating.

Shares of NMDC are trading 3.6% higher on Tuesday at ₹95.67. The stock is up 10% in the last one month and is also trading at a 52-week high.

Also Read: Coforge shares gain nearly 6% after Nexa Agentic AI Platform launch for insurance industry

For the month of May, NMDC's production increased 20% to 5.31 MT from 4.43 MT in the year-ago period. Its offtake declined 7% to 4.04 MT from 4.34 MT in May last year. Its Karnataka offtake was at 0.7 MT compared to 1.34 MT in the previous year.

NMDC in Q4

The state-run company's Earnings Before Interest, Taxes, Depreciation and amortisation (EBITDA) of ₹2,644 crore was below ICICI Securities' estimate of ₹3,090 crore.

Its pellet and other minerals business reported an EBIT loss of ₹102.4 crore compared to a loss of ₹10.8 crore in the previous quarter.

Looking Ahead

NMDC has taken a price hike of ₹500 to ₹600 per tonne in the first quarter of the financial year 2027. It is targeting 60 MT in FY27 and 100 MT by FY30 compared to 50.1 MT in FY26. Its capex for this fiscal is ₹6,000 crore.

Brokerages Divided

Brokerages have mixed views on the stock, with Nuvama maintaining its "hold" rating but increasing its price target, Citi having a "sell" recommendation and Systematix having a "buy" rating.

Nuvama

The brokerage has maintained its "hold" rating on the stock but has increased its price target to ₹100 per share from the previous ₹85 apiece.

It has raised its EBITDA estimates for FY27 and FY28 by 13% and 16%, respectively. It said it is factoring in higher volume and iron ore prices.

Citi

The brokerage has a "sell" rating on NMDC with a price target of ₹85 apiece.

It expects domestic iron ore prices to be rangebound. Lloyds Metal and Energy has enhanced ore capacity from 10 MT to 25 MT, the brokerage said.

Systematix

The brokerage has maintained its "buy" rating on the stock with a price target of ₹112 apiece.

It said NMDC reported strong execution in FY26 and that its future growth trajectory remains intact.

The company's management has guided for FY27 production to be 60 MT and it also expects the EBITDA margin to recover to between 35% - 40%.

Systematix has raised its EBITDA estimates for FY27 and FY28 by 10% and 8% and PAT estimates by 23% and 21%, respectively.

The brokerage said the revision is built on NMDC's strong execution track record.

Of the 23 analysts who have coverage on the stock, 10 have a "buy" rating, four have a "hold" rating and nine have a "sell" rating.

Shares of NMDC are trading 3.6% higher on Tuesday at ₹95.67. The stock is up 10% in the last one month and is also trading at a 52-week high.

Also Read: Coforge shares gain nearly 6% after Nexa Agentic AI Platform launch for insurance industry

/images/ppid_59c68470-image-178028256150629685.webp)

/images/ppid_59c68470-image-1780322531608273.webp)

/images/ppid_59c68470-image-178030003255353400.webp)

/images/ppid_59c68470-image-178028502994863121.webp)

/images/ppid_59c68470-image-178027503715352925.webp)

/images/ppid_59c68470-image-178029512343282637.webp)

/images/ppid_59c68470-image-178028787347845943.webp)