/images/ppid_59c68470-image-177909753618511871.webp)

/images/ppid_59c68470-image-177883009164753540.webp)

What is the story about?

Solar Industries India expects revenue to grow by over 40% in FY27, with its defence business expected to cross ₹4,500 crore and nearly 70% of that coming from international markets, Managing Director and Chief Executive Officer Manish Nuwal said. Consolidated revenue is expected to cross ₹14,000 crore in FY27.

“The international business should grow by around 35% and should cross the ₹5,000 crore revenue mark,” he said, adding that domestic business is also expected to grow at a similar pace. While the explosives business could grow around 35%, the defence segment is expected to grow by nearly 70% in the coming year.

Solar Industries expects trials for its Bhargavastra anti-drone system to be completed this year, with commercialisation likely over the next two years. Nuwal described the platform as a major opportunity for the company. “It will be bigger than Pinaka as we move forward,” he said, referring to the company’s existing Pinaka rocket programme.

The company currently generates around ₹500-550 crore annually from the Pinaka programme and expects additional orders for guided Pinaka rockets in the current financial year. Nuwal said this could add ₹700-800 crore in annual revenue from the next financial year.

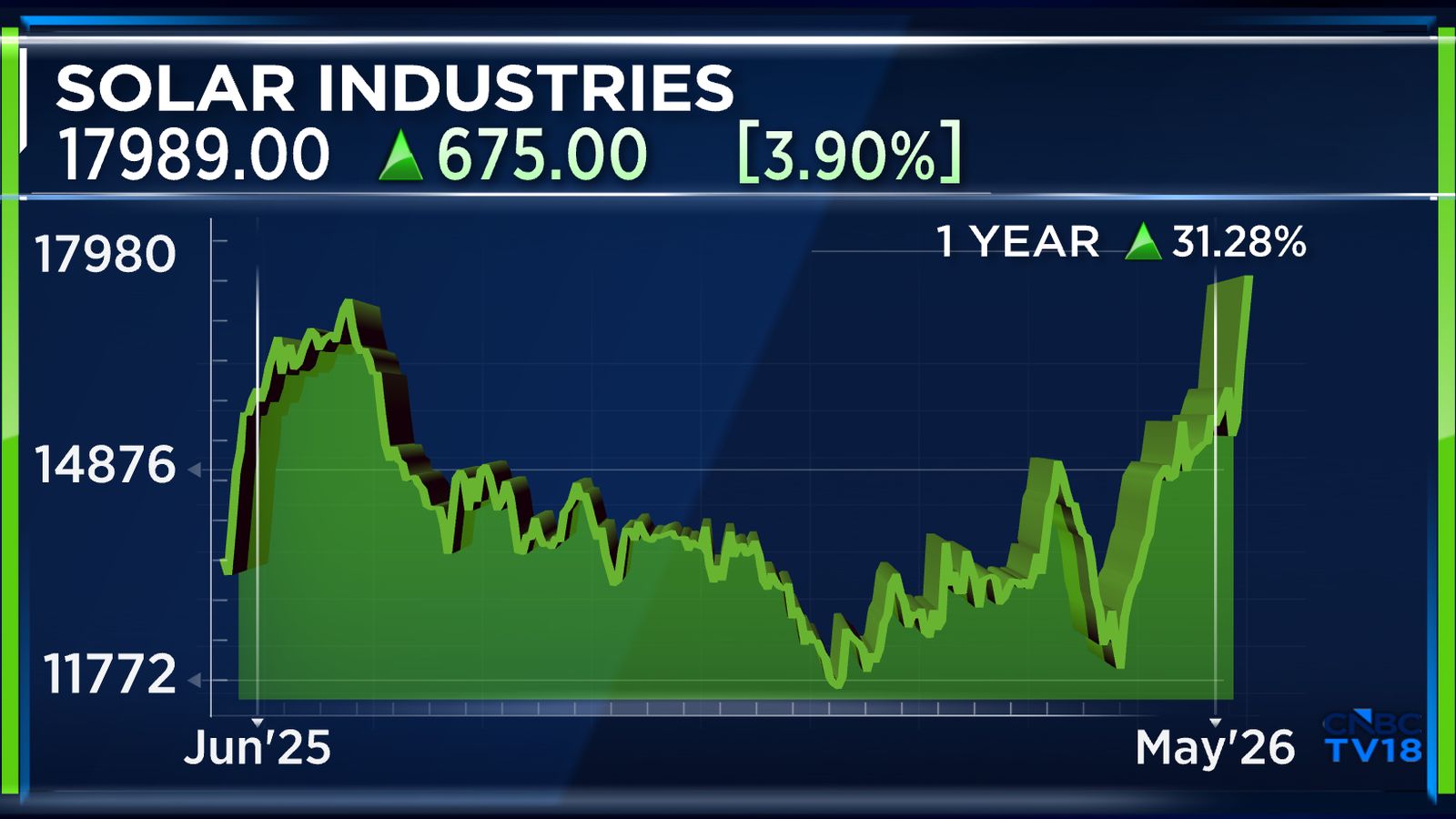

Solar Industries, which has a market capitalisation of ₹1,60,481.85 crore, has seen its shares rise more than 29% over the last year.

The company also reported its earnings for the January-March 2026 quarter of the financial year 2025-26 (FY26).

This is an edited transcript of the interview.Q: ₹14,000 crores of revenue guidance has been bifurcated for us. How much of that will be, you know, international defence, as well as domestic defence? If you could break that up for us, other businesses, as well as explosives, so just give us some colour on that front, because we have that ₹14,000 crore number for defence. On the whole, we have it as around ₹4,500 crores, but split it up for us between international and domestic.

A: Out of the total ₹14,000 crore, we are expecting that the international business should grow by around 35% and should cross the ₹5,000 crore revenue mark, and at the same time, the domestic business should also do better, and the growth rate will be around 35%. As far as defence is concerned, we have given guidance that this year we should cross revenues of around ₹4,500 crore, and out of that, around 70% will be for the international markets.

Q: Now, Coal India put out a release that ammonium nitrate prices have moved up, so the cost of production will move up as well. Will this impact your cost, because that will be an input for you and margins as well? Also, if you could help us out, what is the duration of the pass-through of these higher input costs for you? And how does it compare with the past?

A: A couple of years back, when the commodity cycle started moving up significantly, we suffered because of these price rises, but of late, because of the new changes in the contractual terms, the escalation is now on a monthly basis. So, whatever price increase will happen in ammonium nitrate, it will be passed on to the customers. So, by and large, most of the customers have those kinds of contractual terms.

Also Read | Muthoot Finance bets on higher-ticket gold loans, plans 300 new branches

Q: So, it's now monthly. Earlier, it was what, quarterly or half-yearly?

A: Earlier, it was on a quarterly basis. Now it is monthly, and in this special situation, we have requested, and the customers have agreed to pass on either the increase or decrease on a 15-day basis. So, we are not very much impacted at the moment.

Q: Just to confirm all that you earlier said, your margins at this 26-27% band continue?

A: Yes, last year we achieved around 27%, and in this financial year we just ended at around 28%. We expect that because of the improved defence business and international business as well, we expect these margins will continue even at these elevated numbers.

Q: So, 28% sustains, right?

A: Yes.

Q: And this 35% revenue growth that you've guided, nearly half of that comes in from volumes, and the other half comes in from prices.

A: We have given guidance that this year we should grow by 40%, which is around ₹14,000 crore, and mainly the growth is coming from defence. As far as the explosive market is concerned, around 20% to 22% should come from price rise, and around 15% should come from volume growth. So, it can vary by 2-3%. So, by and large, the explosive business should grow by 35%, and defence — we have already given guidance — should grow by 70% in the coming year.

Q: A large part of the defence business, obviously, will be supported by the Pinaka as well, but I just wanted to understand the Bhargavastra, which is currently under trials. Were that to come, how big an opportunity would this be for you? And by when do you expect this?

A: We have shared on various platforms that we are developing this product, and this can be a game changer for our company, and definitely will help in providing security solutions for our country. So, it's in the development stage. We are expecting that this year we should complete all the trials and development related to this product. As far as the opportunity is concerned, it is too early to speak on the number side, but definitely it will be a big boost for our company's performance.

Q: Would it be as big as Pinaka, bigger than Pinaka?

A: Whatever estimation we can do at this stage will definitely fall short, but it will definitely be bigger than Pinaka as we move forward.

Q: Will you complete this year?

A: We are expecting the trials to be completed this year, so the commercial run should start from either next financial year, maybe deferred by five or six months. So, in the defence programme development cycle, whatever we have achieved is quite fast, and in the next two years, we should reach the commercialisation stage.

Q: Any indication that you have?

A: It's too early to give any number, but as I said, it will be bigger than the Pinaka programme for us.

Also Read | Shadowfax eyes 30% revenue growth over next two years, expects higher profitability from expansion

Q: For those who don't know, the Bhargavastra essentially is like a multi-layer micro missile anti-drone system, right, so we are dependent on Russia for some of these systems, so this kind of is a replacement to that.

A: It is too early to speak on these sensitive issues on these platforms, but this product will provide a good defence mechanism, a defence product for our security solutions. So, let us wait for some more time. We will speak more on this as we move forward. So, our aim at this moment is to complete the trials, so that is what we are focusing on at this stage.

Q: What is the Pinaka size for you annually right now?

A: As of now, it's around ₹500 to ₹550 crore on an annual basis, and one of the products under the same family is the guided Pinaka rocket. We have participated in the RFP, and we expect orders in this financial year, so that will also help us to generate revenue of around ₹700 to ₹800 crores on an annual basis from the next financial year.

Q: You are saying this is going to be bigger than that, so that's the expectation?

A: It will be as big as Pinaka.

Q: You have generated a lot of wealth for investors as well, but the Street would like to know what the next course of action is. I recall when you all started this defence business; it was very small, and now you're talking about ₹4,500 crore. Is there a particular scale where you'll maybe want to list this entity separately, the defence vertical? Is that a thought that's come to your mind at some scale?

A: We have not given thought to this direction, but as we move forward, if it is required, and if it creates wealth for our stakeholders, definitely we will look towards that.

Q: Any scale you have in mind, ₹10,000 crore or something?

A: No, no scale at this moment.

Q: Premier Explosives, that's another small company. I believe that is in the market. I recall many years ago, I think one of the Nuwal family members had bought a small stake in the company, maybe more than 12 years ago, if I'm not mistaken. There are reports that suggest that Premier Explosives is on the block. Are you interested?

A: We have already migrated from a simple explosives company to an energetic materials company. Now we are developing platforms on our own, so our capital allocation strategy, whatever we have made, is focused on adopting new technologies and creating more platform-based products at this moment. So, we are very much focused on that.

Q: So, you're not interested in Premier Explosives as of now. Is that a clarification?

A: I can't say that, but our focus is towards creating platforms and new products on our own.

For the full interview, watch the accompanying videoQ: But you do have a ₹2,000 crore capex plan, and you've acquired a company in Northern India to strengthen your footprint also. So obviously, when all these things are happening, and you are growing, this would make sense, right? You have cash on the books, you obviously have capex plans, and you have growth ideas.

A: Let's see, we will come back on this later.

Q: Is the valuation a problem?

A: I can't comment on this.

Q: For last year, I think you've done around ₹1,800 crore of net profit. Various brokerages believe that by FY29, this profit number will more than double towards ₹3,900 to around ₹4,000 crore, going by the pipeline, going by the way you're evolving the business, do you think it's gettable that from around ₹1,800 crore of net profit, you move closer to ₹4,000 crore by FY29?

A: So there are a couple of things on this point. First, like we have already given guidance that in the coming year we should grow by over 40%, and margins will be at the same level. And if we maintain a growth of around 25% year-on-year, we are not far off from these numbers.

Catch all the latest updates from the stock market here

“The international business should grow by around 35% and should cross the ₹5,000 crore revenue mark,” he said, adding that domestic business is also expected to grow at a similar pace. While the explosives business could grow around 35%, the defence segment is expected to grow by nearly 70% in the coming year.

Solar Industries expects trials for its Bhargavastra anti-drone system to be completed this year, with commercialisation likely over the next two years. Nuwal described the platform as a major opportunity for the company. “It will be bigger than Pinaka as we move forward,” he said, referring to the company’s existing Pinaka rocket programme.

The company currently generates around ₹500-550 crore annually from the Pinaka programme and expects additional orders for guided Pinaka rockets in the current financial year. Nuwal said this could add ₹700-800 crore in annual revenue from the next financial year.

Solar Industries, which has a market capitalisation of ₹1,60,481.85 crore, has seen its shares rise more than 29% over the last year.

The company also reported its earnings for the January-March 2026 quarter of the financial year 2025-26 (FY26).

This is an edited transcript of the interview.Q: ₹14,000 crores of revenue guidance has been bifurcated for us. How much of that will be, you know, international defence, as well as domestic defence? If you could break that up for us, other businesses, as well as explosives, so just give us some colour on that front, because we have that ₹14,000 crore number for defence. On the whole, we have it as around ₹4,500 crores, but split it up for us between international and domestic.

A: Out of the total ₹14,000 crore, we are expecting that the international business should grow by around 35% and should cross the ₹5,000 crore revenue mark, and at the same time, the domestic business should also do better, and the growth rate will be around 35%. As far as defence is concerned, we have given guidance that this year we should cross revenues of around ₹4,500 crore, and out of that, around 70% will be for the international markets.

Q: Now, Coal India put out a release that ammonium nitrate prices have moved up, so the cost of production will move up as well. Will this impact your cost, because that will be an input for you and margins as well? Also, if you could help us out, what is the duration of the pass-through of these higher input costs for you? And how does it compare with the past?

A: A couple of years back, when the commodity cycle started moving up significantly, we suffered because of these price rises, but of late, because of the new changes in the contractual terms, the escalation is now on a monthly basis. So, whatever price increase will happen in ammonium nitrate, it will be passed on to the customers. So, by and large, most of the customers have those kinds of contractual terms.

Also Read | Muthoot Finance bets on higher-ticket gold loans, plans 300 new branches

Q: So, it's now monthly. Earlier, it was what, quarterly or half-yearly?

A: Earlier, it was on a quarterly basis. Now it is monthly, and in this special situation, we have requested, and the customers have agreed to pass on either the increase or decrease on a 15-day basis. So, we are not very much impacted at the moment.

Q: Just to confirm all that you earlier said, your margins at this 26-27% band continue?

A: Yes, last year we achieved around 27%, and in this financial year we just ended at around 28%. We expect that because of the improved defence business and international business as well, we expect these margins will continue even at these elevated numbers.

Q: So, 28% sustains, right?

A: Yes.

Q: And this 35% revenue growth that you've guided, nearly half of that comes in from volumes, and the other half comes in from prices.

A: We have given guidance that this year we should grow by 40%, which is around ₹14,000 crore, and mainly the growth is coming from defence. As far as the explosive market is concerned, around 20% to 22% should come from price rise, and around 15% should come from volume growth. So, it can vary by 2-3%. So, by and large, the explosive business should grow by 35%, and defence — we have already given guidance — should grow by 70% in the coming year.

Q: A large part of the defence business, obviously, will be supported by the Pinaka as well, but I just wanted to understand the Bhargavastra, which is currently under trials. Were that to come, how big an opportunity would this be for you? And by when do you expect this?

A: We have shared on various platforms that we are developing this product, and this can be a game changer for our company, and definitely will help in providing security solutions for our country. So, it's in the development stage. We are expecting that this year we should complete all the trials and development related to this product. As far as the opportunity is concerned, it is too early to speak on the number side, but definitely it will be a big boost for our company's performance.

Q: Would it be as big as Pinaka, bigger than Pinaka?

A: Whatever estimation we can do at this stage will definitely fall short, but it will definitely be bigger than Pinaka as we move forward.

Q: Will you complete this year?

A: We are expecting the trials to be completed this year, so the commercial run should start from either next financial year, maybe deferred by five or six months. So, in the defence programme development cycle, whatever we have achieved is quite fast, and in the next two years, we should reach the commercialisation stage.

Q: Any indication that you have?

A: It's too early to give any number, but as I said, it will be bigger than the Pinaka programme for us.

Also Read | Shadowfax eyes 30% revenue growth over next two years, expects higher profitability from expansion

Q: For those who don't know, the Bhargavastra essentially is like a multi-layer micro missile anti-drone system, right, so we are dependent on Russia for some of these systems, so this kind of is a replacement to that.

A: It is too early to speak on these sensitive issues on these platforms, but this product will provide a good defence mechanism, a defence product for our security solutions. So, let us wait for some more time. We will speak more on this as we move forward. So, our aim at this moment is to complete the trials, so that is what we are focusing on at this stage.

Q: What is the Pinaka size for you annually right now?

A: As of now, it's around ₹500 to ₹550 crore on an annual basis, and one of the products under the same family is the guided Pinaka rocket. We have participated in the RFP, and we expect orders in this financial year, so that will also help us to generate revenue of around ₹700 to ₹800 crores on an annual basis from the next financial year.

Q: You are saying this is going to be bigger than that, so that's the expectation?

A: It will be as big as Pinaka.

Q: You have generated a lot of wealth for investors as well, but the Street would like to know what the next course of action is. I recall when you all started this defence business; it was very small, and now you're talking about ₹4,500 crore. Is there a particular scale where you'll maybe want to list this entity separately, the defence vertical? Is that a thought that's come to your mind at some scale?

A: We have not given thought to this direction, but as we move forward, if it is required, and if it creates wealth for our stakeholders, definitely we will look towards that.

Q: Any scale you have in mind, ₹10,000 crore or something?

A: No, no scale at this moment.

Q: Premier Explosives, that's another small company. I believe that is in the market. I recall many years ago, I think one of the Nuwal family members had bought a small stake in the company, maybe more than 12 years ago, if I'm not mistaken. There are reports that suggest that Premier Explosives is on the block. Are you interested?

A: We have already migrated from a simple explosives company to an energetic materials company. Now we are developing platforms on our own, so our capital allocation strategy, whatever we have made, is focused on adopting new technologies and creating more platform-based products at this moment. So, we are very much focused on that.

Q: So, you're not interested in Premier Explosives as of now. Is that a clarification?

A: I can't say that, but our focus is towards creating platforms and new products on our own.

For the full interview, watch the accompanying videoQ: But you do have a ₹2,000 crore capex plan, and you've acquired a company in Northern India to strengthen your footprint also. So obviously, when all these things are happening, and you are growing, this would make sense, right? You have cash on the books, you obviously have capex plans, and you have growth ideas.

A: Let's see, we will come back on this later.

Q: Is the valuation a problem?

A: I can't comment on this.

Q: For last year, I think you've done around ₹1,800 crore of net profit. Various brokerages believe that by FY29, this profit number will more than double towards ₹3,900 to around ₹4,000 crore, going by the pipeline, going by the way you're evolving the business, do you think it's gettable that from around ₹1,800 crore of net profit, you move closer to ₹4,000 crore by FY29?

A: So there are a couple of things on this point. First, like we have already given guidance that in the coming year we should grow by over 40%, and margins will be at the same level. And if we maintain a growth of around 25% year-on-year, we are not far off from these numbers.

Catch all the latest updates from the stock market here

/images/ppid_a911dc6a-image-177908152831176407.webp)

/images/ppid_59c68470-image-177884003396999331.webp)

/images/ppid_59c68470-image-177884258300262709.webp)