/images/ppid_59c68470-image-178046253242552349.webp)

/images/ppid_59c68470-image-178063503354443298.webp)

What is the story about?

Gold has reclaimed a position many thought it had long lost. According to the European Central Bank's latest report on the international role of the euro, gold accounted for 27% of global official reserve assets at the end of 2025, surpassing US Treasuries at 22% and the euro at 15%.

The milestone marks a dramatic shift in the composition of global reserves and highlights the growing importance of gold in a world increasingly shaped by geopolitical tensions, sanctions risks and financial fragmentation.

Gold's return to the top

For decades, US government bonds served as the dominant reserve asset held by central banks around the world. Their size, liquidity and perceived safety made them the preferred destination for official reserves.

That hierarchy has now changed, at least on a market-value basis.

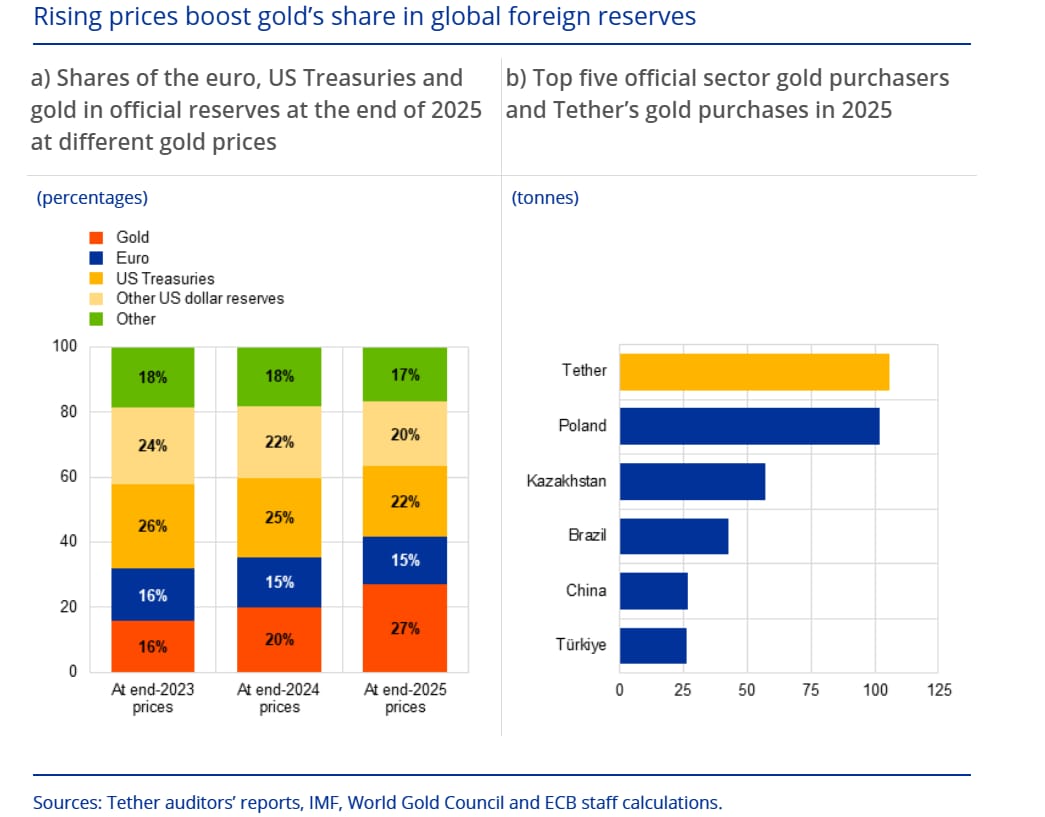

The ECB estimates that gold represented 27% of global official reserve assets by the end of 2025, compared with 22% for US Treasuries and 15% for the euro.

However, the central bank cautions that a significant portion of gold's rise reflects its extraordinary price appreciation.

Gold prices surged roughly 30% in 2024 and another 60% in 2025. As a result, the market value of existing gold holdings increased sharply, mechanically lifting gold's share in global reserves.

When the ECB adjusts for those valuation effects using gold prices from the end of 2023, the picture changes. Gold's share falls to around 16%, roughly in line with the euro's share, while US Treasuries remain the largest reserve asset at approximately 26%.

In other words, gold's rise is partly a story of higher prices. But it is also a story of sustained buying.

Central banks are buying gold at a record pace

The ECB notes that central banks have purchased more than 1,000 tonnes of gold annually for three consecutive years.

That pace is more than double the average annual purchases recorded during the decade preceding Russia's invasion of Ukraine in 2022.

According to the report, official-sector demand has become one of the most important drivers of the gold market.

Central bank purchases accounted for more than 20% of global gold demand in 2025, compared with roughly 10% during the 2010s.

The trend suggests reserve managers are actively reassessing the composition of their portfolios rather than merely benefiting from rising prices.

The geopolitical factor

One of the most striking findings in the ECB report is the growing connection between geopolitics and gold demand.

The shift accelerated after Western nations froze a significant portion of Russia's foreign exchange reserves following its invasion of Ukraine.

The episode highlighted a risk that many countries had previously viewed as theoretical: reserve assets held abroad could become inaccessible during periods of geopolitical conflict.

Unlike foreign government bonds or bank deposits, gold has no issuer and no counterparty.

It cannot be defaulted on, frozen by a foreign government, or rendered inaccessible through sanctions if it is held domestically.

The ECB's analysis finds that countries geopolitically closer to China and Russia have increased their gold purchases more aggressively since 2022 than other nations.

The findings suggest that reserve managers increasingly view gold not merely as a financial asset but as a strategic asset that provides protection against geopolitical shocks.

Tether buys more gold than sovereign nations

Another notable development highlighted by the ECB is that demand for gold is expanding beyond sovereign institutions.

One of the largest buyers of gold in 2025 was not a central bank at all.

It was Tether, the issuer of the world's largest stablecoin.

According to the report, Tether's gold purchases exceeded those of several sovereign nations, underscoring how gold is increasingly being used as a reserve asset across a broader range of financial institutions.

The trend reflects a growing convergence between traditional reserve management and parts of the digital asset ecosystem, where gold continues to be viewed as a trusted store of value.

What it means for India

The global shift comes at a time when the Reserve Bank of India has also been steadily increasing its gold holdings.

According to the RBI's FY26 Annual Report, India's gold reserves stood at 880.52 metric tonnes at the end of March 2026. Gold accounted for 16.7% of India's total foreign exchange reserves, up sharply from 9.3% in September 2024.

The RBI has also increased the proportion of gold stored domestically. Nearly 77% of India's gold stockpile is now held within the country, compared with 66% six months earlier.

India's experience mirrors a broader global trend in which central banks are placing greater emphasis on physical gold ownership and custody.

The bigger picture

The ECB's findings do not suggest that the dollar is losing its dominant position in the global financial system. The US dollar remains the world's leading reserve currency and continues to play a central role in global trade and finance.

But the report does point to an important shift in how reserve managers think about risk.

For much of the post-Cold War period, reserve management was primarily about returns, liquidity and diversification.

Today, geopolitical considerations are playing a much larger role.

As wars, sanctions and strategic rivalries reshape the global economy, central banks are increasingly turning to an asset that sits outside the traditional financial system.

Gold's resurgence is therefore also a reflection of a changing world order, one in which countries are placing a greater premium on assets they can hold, control and access regardless of geopolitical circumstances.

The milestone marks a dramatic shift in the composition of global reserves and highlights the growing importance of gold in a world increasingly shaped by geopolitical tensions, sanctions risks and financial fragmentation.

Gold's return to the top

For decades, US government bonds served as the dominant reserve asset held by central banks around the world. Their size, liquidity and perceived safety made them the preferred destination for official reserves.

That hierarchy has now changed, at least on a market-value basis.

The ECB estimates that gold represented 27% of global official reserve assets by the end of 2025, compared with 22% for US Treasuries and 15% for the euro.

However, the central bank cautions that a significant portion of gold's rise reflects its extraordinary price appreciation.

Gold prices surged roughly 30% in 2024 and another 60% in 2025. As a result, the market value of existing gold holdings increased sharply, mechanically lifting gold's share in global reserves.

When the ECB adjusts for those valuation effects using gold prices from the end of 2023, the picture changes. Gold's share falls to around 16%, roughly in line with the euro's share, while US Treasuries remain the largest reserve asset at approximately 26%.

In other words, gold's rise is partly a story of higher prices. But it is also a story of sustained buying.

Central banks are buying gold at a record pace

The ECB notes that central banks have purchased more than 1,000 tonnes of gold annually for three consecutive years.

That pace is more than double the average annual purchases recorded during the decade preceding Russia's invasion of Ukraine in 2022.

According to the report, official-sector demand has become one of the most important drivers of the gold market.

Central bank purchases accounted for more than 20% of global gold demand in 2025, compared with roughly 10% during the 2010s.

The trend suggests reserve managers are actively reassessing the composition of their portfolios rather than merely benefiting from rising prices.

The geopolitical factor

One of the most striking findings in the ECB report is the growing connection between geopolitics and gold demand.

The shift accelerated after Western nations froze a significant portion of Russia's foreign exchange reserves following its invasion of Ukraine.

The episode highlighted a risk that many countries had previously viewed as theoretical: reserve assets held abroad could become inaccessible during periods of geopolitical conflict.

Unlike foreign government bonds or bank deposits, gold has no issuer and no counterparty.

It cannot be defaulted on, frozen by a foreign government, or rendered inaccessible through sanctions if it is held domestically.

The ECB's analysis finds that countries geopolitically closer to China and Russia have increased their gold purchases more aggressively since 2022 than other nations.

The findings suggest that reserve managers increasingly view gold not merely as a financial asset but as a strategic asset that provides protection against geopolitical shocks.

Tether buys more gold than sovereign nations

Another notable development highlighted by the ECB is that demand for gold is expanding beyond sovereign institutions.

One of the largest buyers of gold in 2025 was not a central bank at all.

It was Tether, the issuer of the world's largest stablecoin.

According to the report, Tether's gold purchases exceeded those of several sovereign nations, underscoring how gold is increasingly being used as a reserve asset across a broader range of financial institutions.

The trend reflects a growing convergence between traditional reserve management and parts of the digital asset ecosystem, where gold continues to be viewed as a trusted store of value.

What it means for India

The global shift comes at a time when the Reserve Bank of India has also been steadily increasing its gold holdings.

According to the RBI's FY26 Annual Report, India's gold reserves stood at 880.52 metric tonnes at the end of March 2026. Gold accounted for 16.7% of India's total foreign exchange reserves, up sharply from 9.3% in September 2024.

The RBI has also increased the proportion of gold stored domestically. Nearly 77% of India's gold stockpile is now held within the country, compared with 66% six months earlier.

India's experience mirrors a broader global trend in which central banks are placing greater emphasis on physical gold ownership and custody.

The bigger picture

The ECB's findings do not suggest that the dollar is losing its dominant position in the global financial system. The US dollar remains the world's leading reserve currency and continues to play a central role in global trade and finance.

But the report does point to an important shift in how reserve managers think about risk.

For much of the post-Cold War period, reserve management was primarily about returns, liquidity and diversification.

Today, geopolitical considerations are playing a much larger role.

As wars, sanctions and strategic rivalries reshape the global economy, central banks are increasingly turning to an asset that sits outside the traditional financial system.

Gold's resurgence is therefore also a reflection of a changing world order, one in which countries are placing a greater premium on assets they can hold, control and access regardless of geopolitical circumstances.

/images/ppid_a911dc6a-image-178055284094579320.webp)

/images/ppid_59c68470-image-178062758540474775.webp)

/images/ppid_59c68470-image-178050266252837930.webp)

/images/ppid_59c68470-image-178059757658679460.webp)

/images/ppid_a911dc6a-image-178050083776054694.webp)