What is the story about?

What's Happening?

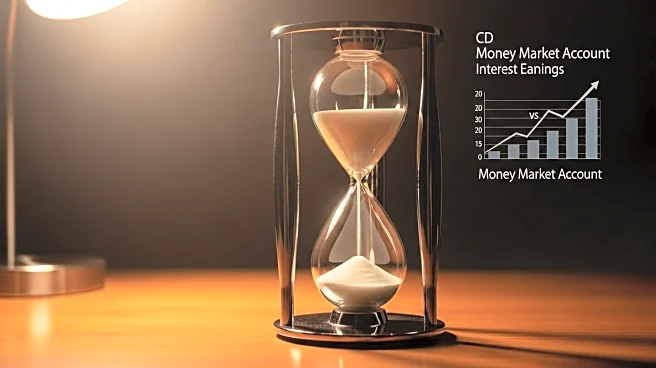

Recent analysis compares the interest earnings of a $40,000 deposit in a certificate of deposit (CD) versus a money market account. With fluctuating interest rates due to Federal Reserve cuts, savers are evaluating which option offers better returns. A CD provides a fixed interest rate, ensuring predictable earnings, while a money market account offers variable rates that can change with market conditions. Current calculations show that over a six-month period, a CD at 4.45% earns $880.31, slightly more than a money market account at 4.40%, which earns $870.53. However, over nine months, the money market account outperforms the CD, earning $1,312.87 compared to $1,283.19. Over a year, both account types yield identical returns of $1,760.00. The choice between these accounts depends on the saver's preference for guaranteed returns versus potential higher earnings with variable rates.

Why It's Important?

The decision between a CD and a money market account is crucial for savers looking to maximize interest earnings on large deposits. CDs offer security with fixed rates, appealing to those who prioritize guaranteed returns. Conversely, money market accounts may offer higher returns if rates remain favorable, but they carry the risk of rate fluctuations. This analysis is particularly relevant as the Federal Reserve's rate cuts impact savings account yields, influencing savers' strategies. Understanding these dynamics helps individuals make informed decisions about where to allocate their funds, balancing risk and reward in a changing economic environment.

What's Next?

As the Federal Reserve is expected to implement further rate cuts, savers should anticipate potential declines in money market account rates. This may lead to increased interest in CDs for those seeking stable returns. Financial advisors and institutions may offer guidance on optimizing savings strategies in light of these changes. Savers should monitor rate trends and consider their financial goals and risk tolerance when choosing between these account types.

Beyond the Headlines

The broader implications of this financial decision extend to the overall savings behavior in the U.S. As interest rates fluctuate, savers may shift their preferences, impacting the demand for different financial products. This could influence banks' offerings and strategies, potentially leading to innovations in savings account features. Additionally, the choice between fixed and variable rates reflects broader economic sentiments and risk management approaches among consumers.