What's Happening?

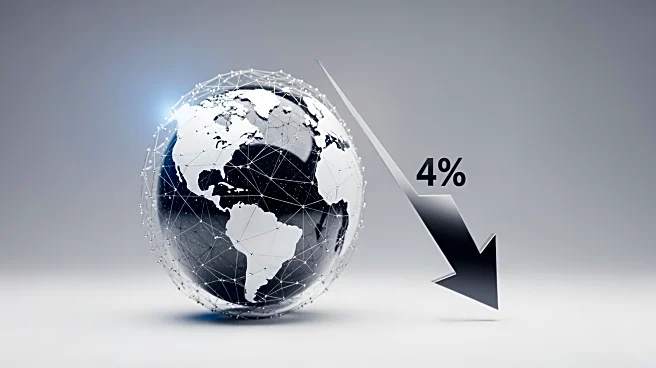

Global commercial insurance rates have decreased by 4% in the third quarter of 2025, marking the fifth consecutive quarterly decline. This trend follows seven years of consistent rate increases and is driven

by heightened competition among insurers and favorable reinsurance pricing. The Global Insurance Market Index by Marsh indicates that all global regions experienced rate decreases, with the Pacific region seeing the largest drop at 11%. In the U.S., the composite rate declined by 1%, contrasting with a flat rate in the previous quarter. Rates for property, cyber, and financial and professional insurance have declined across all regions, while casualty rates increased by 3% globally, largely due to significant jury awards in the U.S.

Why It's Important?

The decline in insurance rates is significant for businesses and industries across the U.S., as it presents opportunities for negotiating better terms and broader coverage. Lower rates can reduce operational costs for companies, potentially leading to increased investment and growth. However, the increase in casualty rates, driven by large jury awards, poses challenges for insurers and businesses facing liability claims. The competitive insurance market, characterized by ample capacity, suggests that these trends may continue, offering benefits to clients seeking cost-effective insurance solutions.

What's Next?

As the insurance market remains competitive, businesses are likely to continue benefiting from lower rates and improved coverage options. Marsh anticipates these trends to persist, barring unforeseen changes in market conditions. Companies may leverage this environment to optimize their insurance portfolios, while insurers might focus on managing the risks associated with rising casualty claims. Stakeholders will be closely monitoring any shifts in market dynamics that could impact future rate trends.

Beyond the Headlines

The ongoing decline in insurance rates could have broader implications for the industry, including potential pressure on insurers' profitability and the need for strategic adjustments. The trend may also influence regulatory discussions around insurance practices and consumer protection, as stakeholders seek to balance competitive pricing with sustainable business models.