What's Happening?

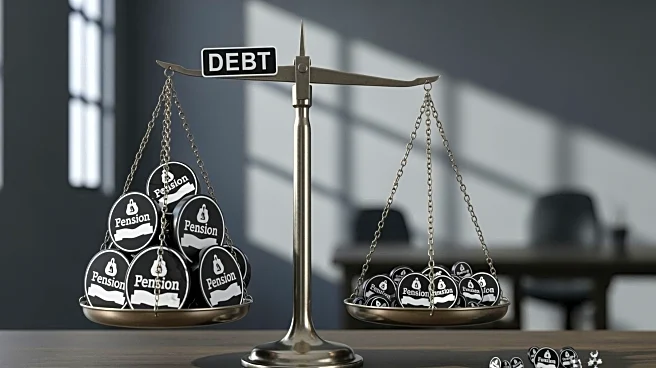

Illinois lawmakers are reviewing Senate Bill 1937, which proposes significant increases in retirement benefits for Tier 2 employees hired after 2010. The bill aims to reduce retirement ages, remove early retirement penalties, and enhance cost-of-living

adjustments, among other changes. To fund these benefits, the state would need to contribute an estimated $13.9 billion immediately, with long-term costs exceeding $52.7 billion. This approach continues the state's 'pay-later' pension funding strategy, which has led to substantial unfunded liabilities.

Why It's Important?

The proposed legislation could exacerbate Illinois' pension debt, placing a financial burden on future generations. The state's current pension funding schedule, known as the 'Edgar Ramp,' has been criticized for deferring costs and increasing liabilities over time. The bill's passage could lead to higher taxes and reduced funding for essential services, impacting the state's economic stability. The situation highlights the need for sustainable pension reform and fiscal responsibility to ensure long-term financial health.

What's Next?

If Senate Bill 1937 is enacted, Illinois may face increased pension liabilities, prompting discussions about alternative funding strategies. Lawmakers may consider measures to outlaw gradual amortization of benefits and require voter approval for changes that increase liabilities. The debate over pension reform is likely to continue, with stakeholders advocating for solutions that balance the needs of government employees and taxpayers.

Beyond the Headlines

The ongoing pension challenges in Illinois may serve as a cautionary tale for other states facing similar issues. The situation underscores the importance of transparent fiscal policies and the ethical implications of deferring financial obligations to future generations. The debate may influence broader discussions about public sector pension reform and the need for equitable solutions that protect both retirees and taxpayers.