Draft Income Tax Rules 2026: The draft Income Tax Rules, 2026 propose significant changes to the way the taxable value of motor vehicles is calculated. Several revisions have been introduced in the valuation

of perquisites where an employer provides a car to an employee. If these changes are approved by Parliament, they will apply under both the old and new tax regimes, since they relate to the valuation of salary-related perks irrespective of the regime opted for.

In categories where the perquisite value has been increased, employees will end up paying higher income tax, as the revised value of the perk will be added to their salary income and taxed accordingly.

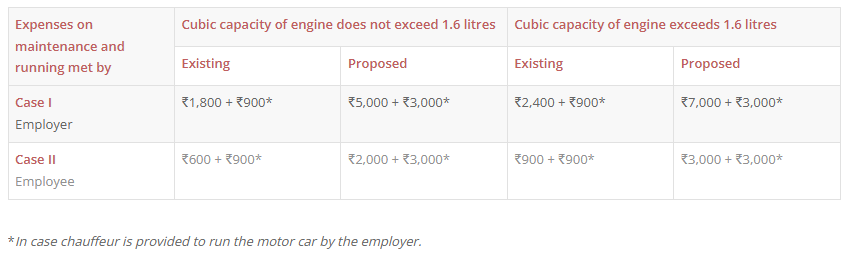

For instance, if an employer provides a car for both official and personal use and the employee bears the fuel and maintenance costs, the taxable perquisite value has been sharply revised. Earlier, for a car with an engine capacity of less than 1.6 litres, the taxable value was Rs 600 per month. Under the draft rules, this has been increased to Rs 2,000 per month.

For reference, the Hyundai Creta’s naturally aspirated MPi petrol engine has a capacity of 1.5 litres (1,497 cc). The Volkswagen Virtus comes with turbo petrol engine options of 1 litre (999 cc) and 1.5 litres (1,498 cc), depending on the variant.

What Has Changed Under Draft Income Tax Rules, 2026

Motor Car Perquisite

- Old Rule: Rule 3(2) of the Income-tax Rules, 1962

- New Rule: Rule 15(3) of the Draft Rules, 2026

Chartered Accountant Avinash Kumar Rao, Partner at Mohindra & Associates, told ET that the 1962 Rules traditionally classified motor car benefits based on:

- The purpose of use (official, personal or mixed),

- Who bears the running and maintenance expenses, and

- Whether a chauffeur is provided.

Rao explained that while the draft Income Tax Rules, 2026 retain this structural classification, they substantially revise the valuation amounts to reflect current economic realities. This revision has important implications for salary structuring and take-home pay, making it essential for both employers and employees to review arrangements in advance.

Proposed Changes and Impact

The Draft Rules prescribe a higher perquisite value for motor cars owned by employers and used partly for official duties and partly for personal purposes by employees or their household members. The proposed changes are expected to directly affect the cost structure of the CTC-based car leasing model.

From an employee’s perspective, the higher perquisite value will increase taxable income, thereby raising the tax outgo. The tax arbitrage that previously made the CTC car leasing model attractive — the difference between actual lease rentals and the lower notional perquisite value — is likely to narrow. Consequently, the net tax savings under this model will decline.

The likely impact can be illustrated through the following examples:

Example 1:

- Lease rental: Rs 25,000 per month

- Engine capacity: 1.7 litres

- Usage: Mixed (official and personal)

- Maintenance and running expenses borne/reimbursed by employer

- Tenure: 1 year

Example 2:

- Lease rental: Rs 25,000 per month

- Engine capacity: 1.5 litres

- Usage: Mixed (official and personal)

- Maintenance and running expenses borne/reimbursed by employee

- Tenure: 1 year

It is important to note that employers will not face any additional tax burden due to the proposed revisions, as the CTC paid to employees — including lease rentals — will continue to qualify as a deductible business expense.

Overall, the Draft Rules significantly increase the perquisite valuation of employer-provided cars, resulting in higher tax liability for employees opting for CTC-based car leasing. If notified, the revised valuation will apply even to existing leases from April 1, 2026. As a result, the tax efficiency of the CTC car leasing model will be materially reduced, affecting both its attractiveness and overall financial viability going forward.